Washington contractor insurance costs vary dramatically based on your specific work and business profile. At FirstMark Insurance Group, we’ve helped countless contractors navigate these pricing differences to find rates that actually reflect their risk level.

The gap between what you might pay and what you should pay often comes down to understanding what insurers are really evaluating. This guide walks you through the factors that matter most, how to compare quotes effectively, and the mistakes that end up costing contractors thousands in unnecessary premiums.

What Determines Your Washington Contractor Insurance Rate

Trade Type and Risk Profile

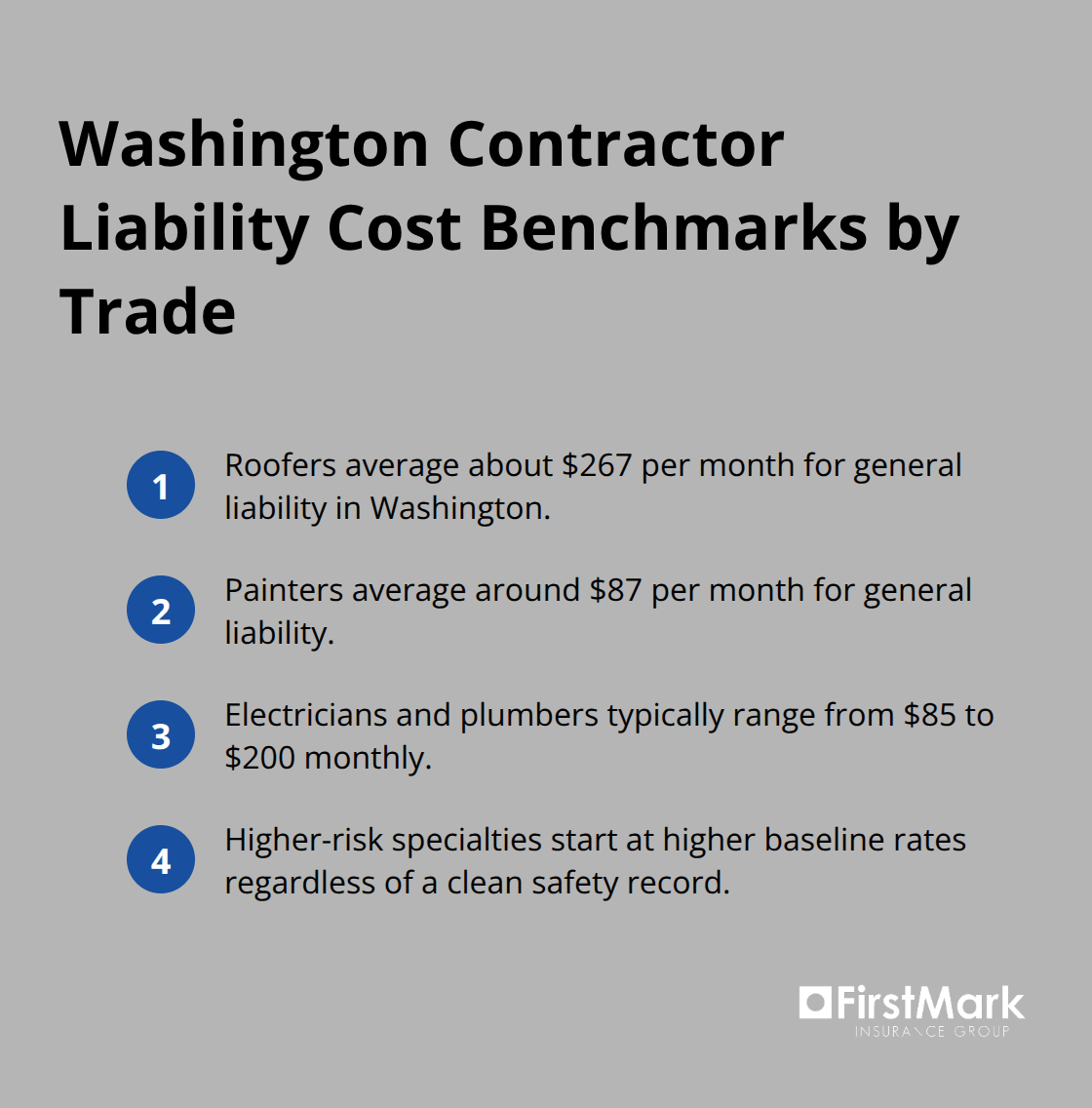

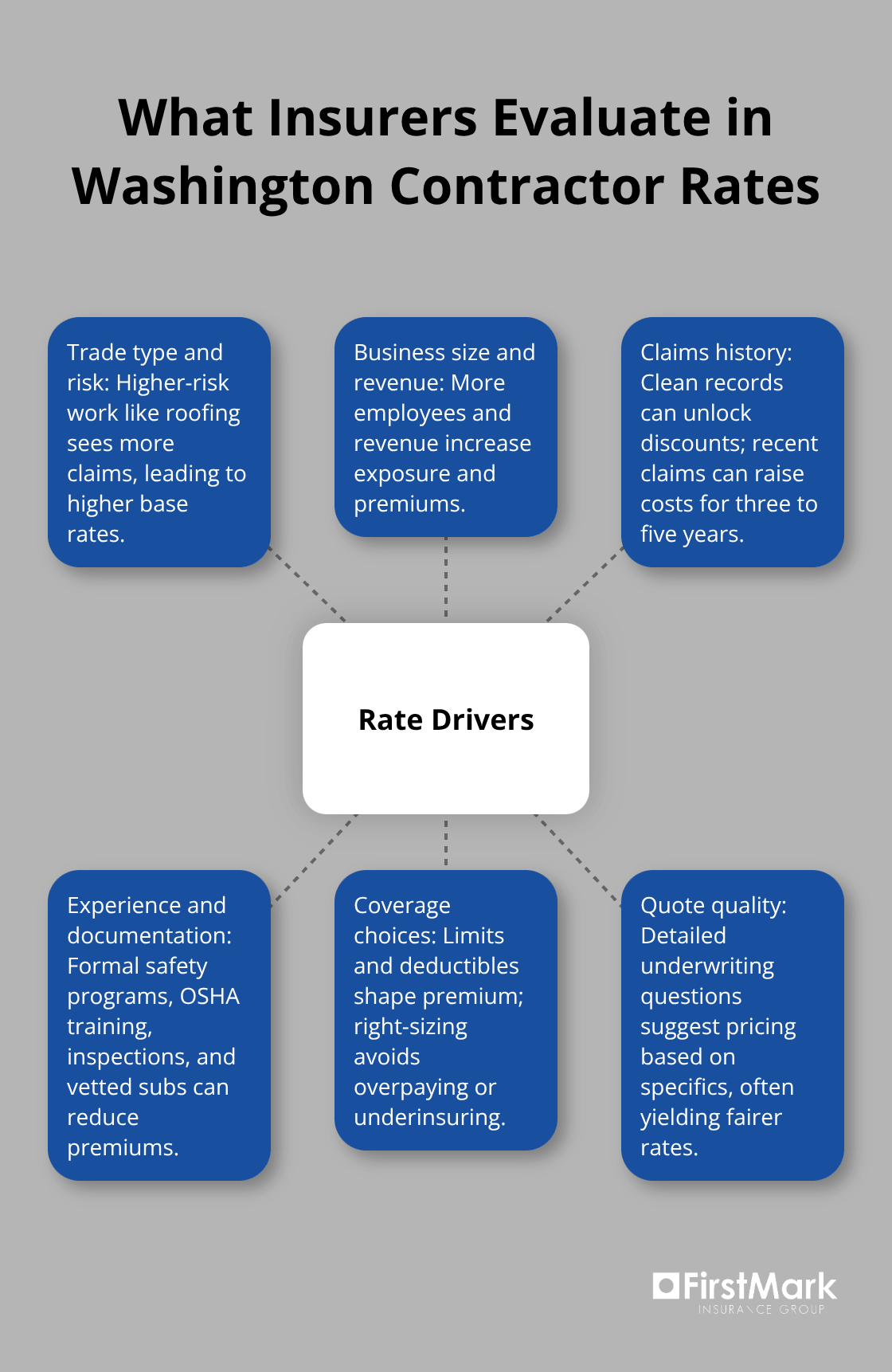

Your insurance premium reflects a calculation that goes far beyond a simple lookup table. Insurers assess multiple dimensions of your operation to predict claim likelihood, and understanding these factors gives you real leverage when shopping for rates. The trade you perform matters enormously. Roofers in Washington pay roughly $267 per month for general liability, while painters average around $87 monthly according to recent market data. This $180 spread exists because roofing generates more slip-and-fall claims, weather-related disputes, and structural damage allegations than interior finishing work. Electricians and plumbers sit in the middle, typically ranging from $85 to $200 monthly.

The difference isn’t arbitrary-it reflects actual loss experience across thousands of policies. If you perform higher-risk work like roofing or structural demolition, your baseline rate starts higher regardless of your perfect safety record. This is why some contractors deliberately narrow their service offerings to lower-risk specialties; the insurance savings alone can justify the business model change.

Business Size and Revenue Impact

Your annual revenue and payroll directly influence your exposure calculation and premium structure. A solo operation averages about $76 per month for general liability, while adding your first employee more than doubles that to roughly $150 monthly. A firm with 20 to 49 employees pays around $3,059 monthly on average. This dramatic escalation reflects the reality that larger operations generate higher claim exposure simply through volume. The jump from solo to your first hire represents the steepest premium increase you’ll experience, so understanding this threshold helps you plan expansion costs accurately.

Claims History as Your Strongest Asset

Your claims history acts as the strongest negotiating tool you possess. A single significant claim can raise your premiums for three to five years afterward, making loss prevention genuinely financial strategy rather than just safety philosophy. Conversely, contractors who maintain clean records for five or more years often qualify for loyalty discounts that insurers rarely advertise. This reality means that every job-site decision-from equipment maintenance to worker supervision-carries direct financial consequences beyond immediate safety concerns.

Experience and Documentation

Years in business matter, though perhaps less than you’d expect. An electrician with 15 years of experience doesn’t automatically pay less than one with three years if the newer contractor has zero claims and strong safety protocols. What really moves the needle is documented evidence of professional practices-formal safety programs, OSHA training completion, regular job-site inspections, and proper subcontractor vetting. Insurers now reward this documentation with measurable premium reductions, sometimes 10 to 15 percent depending on the program’s rigor. These concrete practices signal to underwriters that you manage risk actively rather than hoping nothing goes wrong. Understanding how insurers weight these factors positions you to negotiate effectively when you receive quotes, and it also reveals which operational improvements deliver the fastest premium relief.

Getting Real Quotes That Reflect Your Actual Risk

Gather Quotes from Multiple Carriers

Shopping for contractor insurance without comparing multiple quotes is like accepting the first bid on a job without understanding the scope. Rates vary significantly across carriers because underwriting standards differ, and what one insurer views as high-risk another may rate as moderate. General liability premiums for the same roofing contractor can range from $200 to $350 monthly depending on the carrier’s appetite for that trade and their loss experience in Washington. Contact at least three to five providers and provide identical information to each: your trade classification, annual revenue, number of employees, years in business, and claims history. This consistency matters because vague details lead to lowball quotes that change dramatically during underwriting, wasting weeks of your time.

Evaluate What Each Quote Actually Reveals

When you receive quotes, the document itself tells you what the carrier actually evaluated. A quote that omits questions about your safety protocols or subcontractor vetting practices signals that carrier uses a lighter underwriting touch, which often means their rates don’t reflect your actual exposure. Conversely, detailed underwriting questions indicate the carrier prices based on specifics rather than industry averages. This matters because specific pricing usually means lower rates for contractors who manage risk actively. The questions carriers ask reveal their underwriting philosophy and, by extension, whether their rates account for your actual operational practices.

Choose Coverage Limits That Match Your Work

Coverage limits and deductibles directly control your monthly premium, and most contractors make poor choices here because they don’t understand the downstream cost of being wrong. Washington requires minimum general liability of $200,000 in public liability and $50,000 property damage, or a combined single limit of $250,000. Many commercial clients and developers demand 1 million per occurrence and 2 million aggregate, which raises your premium roughly 20 to 40 percent depending on your trade and claims history. The mistake contractors make is purchasing 1M/2M limits across all jobs when some projects legitimately need only the state minimum, and others require 2M/5M or higher. Request quotes at three different limit levels: state minimum, 1M/2M, and 2M/5M so you see the actual cost of each tier.

Optimize Deductibles and Bundle Coverage

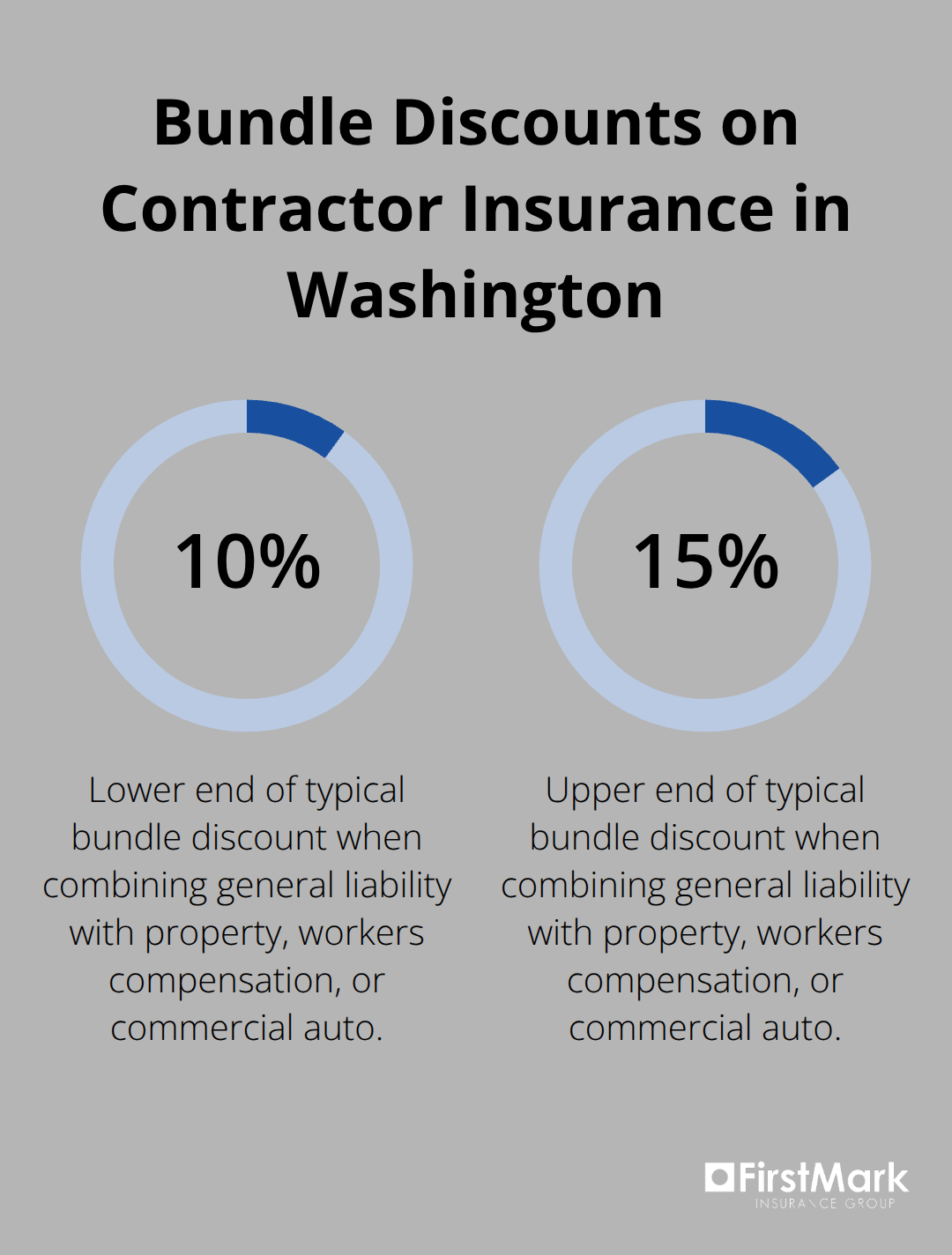

Deductibles work the same way as coverage limits. A $1,000 deductible costs significantly less than $500, but only if you can actually absorb that $1,000 without affecting cash flow when a claim occurs. Ask providers specifically about bundle discounts when combining general liability with commercial property, workers compensation, or commercial auto. These bundled policies often cost 10 to 15 percent less than purchasing each separately, and they simplify renewal management. Bundling transforms your insurance structure from a collection of separate policies into a coordinated protection strategy that carriers reward with measurable savings.

Move Forward with Confidence

Before finalizing any quote, confirm that you’re comparing genuine alternatives rather than variations from a single underwriter. The quotes you’ve gathered now provide the foundation for understanding what fair rates actually look like in your market. With this information in hand, you’re positioned to recognize which carriers understand your specific risk profile and which ones rely on generic pricing formulas. The next step involves understanding the common mistakes that contractors make during the buying process-mistakes that often cost thousands in unnecessary premiums or inadequate coverage.

Where Contractors Lose Thousands on Insurance

The gap between what you pay and what you should pay often widens during the buying process itself, not just in the quotes you receive. Most contractors make one or two critical mistakes that either leave them dangerously underinsured or paying premiums that don’t match their actual risk profile.

Purchasing Coverage Limits Based on Comfort Rather Than Demand

The first mistake is selecting coverage limits based on what feels comfortable rather than what your actual work demands. A general contractor taking on a commercial renovation project worth $500,000 cannot rely on the state minimum $250,000 combined single limit. Commercial clients routinely require $1,000,000 per occurrence and $2,000,000 aggregate, and if you don’t have it, you won’t get the job. More problematically, if you do get the job without proper limits and a claim occurs, your personal assets face exposure beyond what insurance covers.

The opposite mistake-purchasing excessive limits you’ll never need-wastes money month after month. A painter doing residential interior work rarely needs more than the state minimum, yet some painters carry higher limits across all jobs simply because they did once for a single large project. Request quotes specifically for the limits your work actually requires, then purchase accordingly rather than defaulting to one coverage tier for everything.

Omitting Details During the Quoting Process

Incomplete disclosure during the quoting process creates quotes that evaporate during underwriting. Contractors who omit details about subcontractors they regularly hire, specific equipment they use, or past claims they consider minor receive quotes that don’t reflect reality. An electrician who hires subcontractors but fails to mention this gets a quote assuming they work solo, then watches their premium jump 30 to 40 percent when underwriting discovers the truth. Similarly, a roofing contractor who mentions a claim from eight years ago but not one from three years ago receives a quote that doesn’t reflect their actual loss history.

Neglecting Annual Policy Reviews

Annual policy reviews represent another overlooked opportunity where contractors leave money on the table. Your premium should decrease as your claims history ages beyond the five-year lookback period, yet many contractors never ask about this reduction. If you had a claim four years ago and your policy renews this year, you should specifically request a quote reflecting that your loss history now extends beyond the standard underwriting window. Some carriers automatically apply this benefit; others require you to request it explicitly.

Comparing Price Without Understanding Coverage

The final mistake is selecting purely on price without understanding what coverage you actually receive. A quote at $89 per month might exclude certain job types your business performs, include a $5,000 deductible instead of $1,000, or provide lower aggregate limits than a $125 per month alternative. Comparing price alone without reading the policy details means you’re not really comparing coverage-you’re comparing misleading numbers. Spend 30 minutes reviewing what each quote actually includes, and you’ll often find that the second-cheapest option provides substantially better protection for only slightly more premium.

Final Thoughts

Finding fair Washington contractor insurance costs requires moving beyond price comparison into genuine risk assessment. The factors that determine your premium-your trade, business size, claims history, and documented safety practices-are all within your control to some degree. Contractors who understand these drivers negotiate from a position of strength, recognizing which rate increases reflect legitimate risk and which ones signal an insurer’s poor fit for their operation.

The mistakes outlined earlier cost contractors thousands annually because they occur during the buying process itself, not just in the quotes received. Purchasing coverage limits based on comfort rather than actual job requirements leaves you either dangerously exposed or overpaying for protection you don’t need. Omitting business details during quoting creates false quotes that collapse during underwriting, and skipping annual reviews means you miss premium reductions as your claims history ages.

Working with an insurance professional transforms this process from a frustrating administrative task into a strategic business decision. A broker with deep Washington contractor experience understands how different carriers underwrite your specific trade, which questions signal thorough evaluation versus generic pricing, and where bundle discounts actually exist. Connect with FirstMark Insurance Group to translate your quotes into a coherent strategy and access fair rates for your specific risk profile.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation