A single liability claim can devastate a business that lacks proper coverage. General liability protection in Seattle isn’t optional-it’s the foundation that keeps your operation standing when accidents happen.

At FirstMark Insurance Group, we’ve seen how the right policy transforms risk from a business-ending threat into a manageable expense. Whether you run a retail shop, service business, or contractor operation, understanding what this coverage actually protects is the first step toward real peace of mind.

What Your General Liability Policy Actually Covers

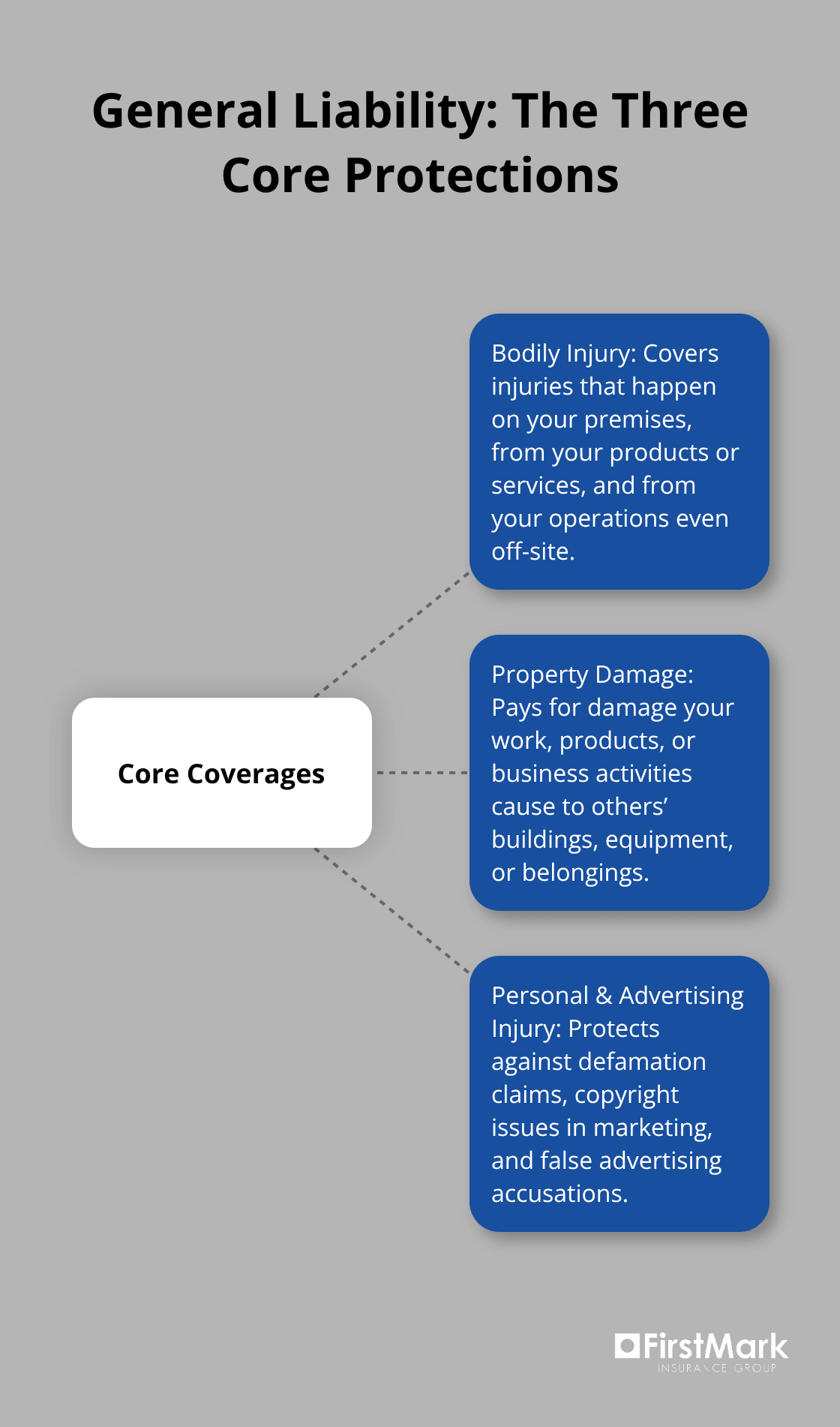

The Three Core Protections Your Policy Provides

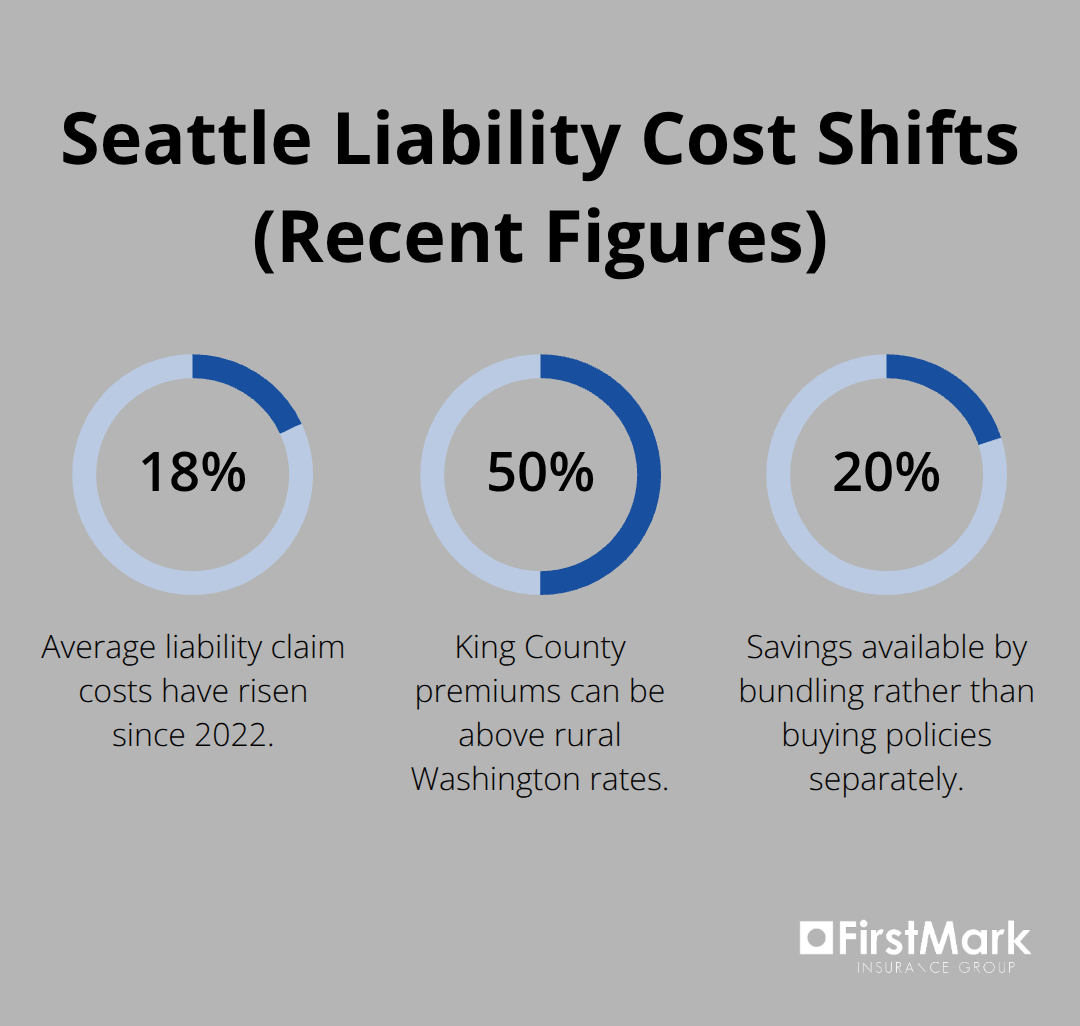

General liability insurance protects your Seattle business from three core exposures that appear repeatedly in claims we handle. When a customer slips on your floor and breaks their wrist, when your work crew damages a client’s property, or when your advertisement inadvertently harms someone’s reputation, general liability steps in to cover medical bills, repair costs, legal defense, and settlements. Average liability claims now reach $97,200, up 18 percent since 2022, which means outdated coverage limits leave most Seattle businesses dangerously exposed.

Bodily Injury Claims Drive the Largest Payouts

Bodily injury claims represent the largest category of payouts, driven by rising medical expenses and court awards that reflect today’s healthcare costs and litigation realities. Your policy covers injuries that occur on your business premises, injuries caused by your products or services, and injuries caused by your operations even if they happen off-site. Washington’s pure comparative negligence framework means injured parties can recover damages even if they’re partially at fault, which increases settlement costs and renewal premiums across the state.

Property Damage and Personal Injury Protection

Property damage liability protects you when your work, your products, or your business activities damage someone else’s building, equipment, or belongings. A painter who spills paint on a client’s flooring, an electrician whose installation causes a fire, or a delivery service that damages warehouse inventory-these situations drain your cash reserves without proper coverage. Personal and advertising injury rounds out protection by covering defamation claims, copyright infringement in your marketing materials, and false advertising accusations.

Coverage Limits Must Match Today’s Claim Reality

Most Seattle businesses operate with minimum coverage limits that haven’t been updated in years, creating a false sense of security. A single serious claim exceeding your policy limit becomes your personal liability, paid directly from business assets or personal accounts. King County procurement rules require vendors to carry $1,000,000 per occurrence and $2,000,000 aggregate limits for county work, while state licensing thresholds mandate at least $200,000 public liability for most trades.

If your current limits fall below $500,000 per occurrence, your policy was designed for yesterday’s claim environment, not today’s. We recommend reviewing whether your limits reflect your actual exposure, particularly if you’ve expanded operations, added subcontractors, or increased customer interaction since your last renewal. Rising medical costs and attorney fees make defense-included policies essential-your insurer covers legal costs even while contesting a claim, preventing litigation from consuming your operating capital. Understanding these three coverage areas positions you to evaluate whether your current protection matches the real risks your business faces.

Why Your Seattle Business Can’t Skip General Liability Coverage

Seattle’s Unique Liability Landscape

Seattle’s business environment creates specific liability exposures that differ sharply from national averages. The region’s dense urban core concentrates customer interaction, which increases slip-and-fall risk in retail and hospitality settings. Construction and trades dominate the local economy-electricians, plumbers, roofers, and contractors face higher injury exposure and property damage claims than office-based businesses. Washington’s pure comparative negligence law means injured parties recover damages even when partially at fault, driving settlement costs higher than states with different negligence frameworks.

How Location and Industry Shape Your Costs

King County premiums run 30 to 50 percent above rural Washington rates due to larger verdict pools and medical cost inflation in the Seattle metro area. A roofer in Seattle pays substantially more than an identical operation in rural Washington, not because the work differs but because the legal and medical environment amplifies claim costs. Software consultants in Seattle typically pay $25 to $40 monthly for general liability, while pressure washing operations exceed $1,000 monthly-industry risk classification creates vastly different cost structures, yet both need protection.

Regulatory Requirements That Affect Your Coverage

If your business serves King County government or other municipal agencies, mandatory procurement rules require $1,000,000 per occurrence and $2,000,000 aggregate limits just to bid on contracts. State licensing thresholds set minimums of $200,000 public liability and $50,000 property damage for most trades, but these floors represent bare minimum compliance, not adequate protection.

The Financial Reality of Uninsured Claims

A single serious bodily injury claim can bankrupt a small business without coverage, and larger claims routinely exceed $250,000. Washington’s litigation environment means defense costs accumulate quickly-attorney fees, expert witnesses, court costs, and settlement negotiations drain cash reserves even before a verdict. Claims history dominates renewal pricing for the next three to five years; a serious claim can raise your renewal premium 20 to 40 percent and make coverage harder to obtain.

Strategies to Strengthen Protection and Control Costs

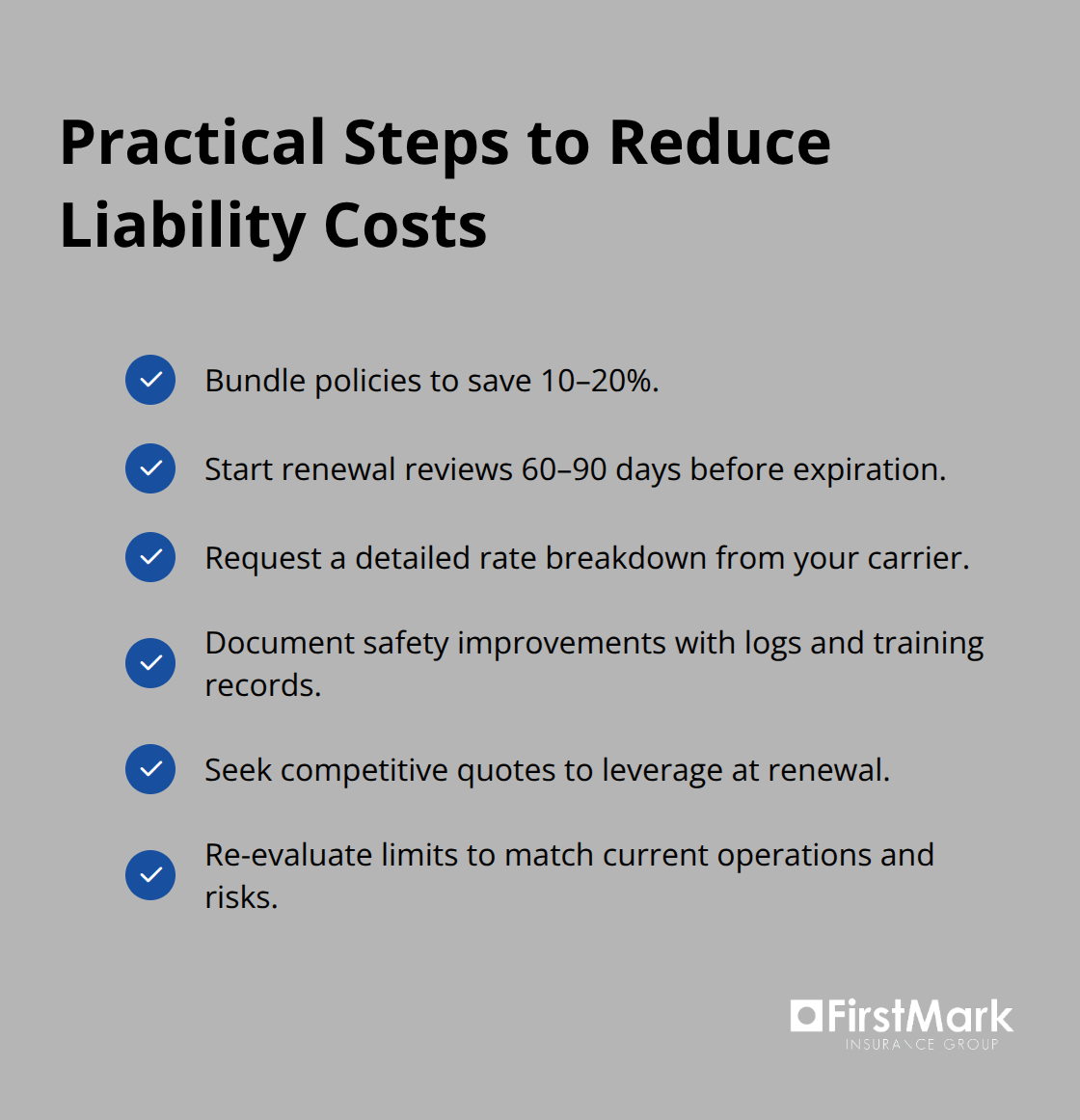

Bundling general liability with commercial property, workers compensation, and commercial umbrella coverage yields 10 to 20 percent savings compared to purchasing policies separately, making comprehensive protection more affordable than most business owners realize. Annual renewal reviews 60 to 90 days before your policy expires allow you to request detailed rate breakdowns, identify premium increases tied to claims surcharges or rate changes, and present documented safety improvements or competitive quotes to your insurer. Rising medical expenses and court awards mean a policy designed five years ago leaves you dangerously exposed today. When you evaluate your current coverage, you’ll likely discover that your limits and policy structure no longer match your actual operations and the claim realities Seattle businesses face.

Common Claims and Real-World Scenarios

Slip-and-Fall Incidents in Retail Environments

Retail environments across Seattle experience slip-and-fall incidents at predictable rates, yet most business owners underestimate both frequency and severity. A customer slips on wet flooring in a grocery store and sustains a fractured hip requiring surgery-medical costs alone exceed $35,000, with additional physical therapy, lost wages, and pain-and-suffering damages pushing total exposure toward $150,000 or higher. Your general liability policy covers the medical expenses, rehabilitation costs, and legal defense if the injured party pursues a lawsuit.

The critical issue most Seattle retailers face is that their $300,000 per-occurrence limit was selected years ago and hasn’t kept pace with inflation in healthcare costs. A single serious slip-and-fall claim can consume your entire policy limit, leaving nothing for the next incident or for defense costs if liability is disputed. Documentation matters enormously-surveillance footage showing that staff ignored a wet floor for hours strengthens the injured party’s case and increases settlement pressure on your insurer. Conversely, timestamped inspection logs and immediate cleanup records reduce claim severity significantly.

Implement documented safety protocols with quarterly jobsite inspections and staff training records. Insurers reward these risk-reduction measures with premium reductions at renewal, making safety documentation a direct path to lower costs while protecting your business.

Product Liability and Customer Injuries

Product liability claims arise when your goods cause customer injury, and Seattle service businesses frequently underestimate this exposure. A cleaning product your company sells causes chemical burns, a piece of equipment malfunctions and injures an operator, or a food product triggers an allergic reaction-these scenarios drain cash reserves quickly without proper coverage. Your policy must specify exactly which products fall under coverage and whether certain product categories carry exclusions that leave you exposed.

Claims in this category often exceed $100,000 because medical costs, legal defense, and settlement demands accumulate rapidly. A single serious product injury claim can exhaust your policy limit entirely, leaving subsequent claims unprotected. Review your current policy language to confirm that product liability coverage extends to all goods your business sells or distributes, and verify that your limits reflect the maximum injury exposure a defective product could create.

Damage to Client Property During Service Delivery

Damage to client property during service delivery represents a major claim category, where your work crew accidentally destroys a client’s flooring, equipment, or inventory while performing contracted services. A plumbing installation that causes water damage to a client’s building interior, an electrical installation that triggers a fire, or a landscaping crew that damages underground utility lines-each of these situations creates liability exposure that extends well beyond the service price.

Claims in this category frequently exceed $100,000 because property damage claims compound over time: initial repair costs, business interruption losses, and consequential damages accumulate faster than most business owners anticipate. Your policy must specify whether it covers only direct property damage or also includes business interruption and additional living expenses for affected clients. Many Seattle contractors operate with policies that exclude certain client-property exposures entirely, creating dangerous coverage gaps.

When you review your current policy language, examine whether damage to client property during service delivery is included without exclusions, and verify that your coverage limits reflect the maximum property value you could damage during a single project. This examination often reveals that your existing protection falls short of the actual risks your operations create.

Final Thoughts

Your current policy likely reflects coverage decisions made years ago, before medical costs climbed 18 percent and before your business expanded its operations or customer base. That gap between yesterday’s protection and today’s claim reality creates exposure that threatens your business stability, and a single serious claim exceeding your policy limits becomes your personal financial responsibility. General liability protection Seattle businesses depend on isn’t a checkbox item-it’s the operational foundation that separates businesses that survive claims from those that collapse under them.

Finding the right coverage requires understanding your specific operations, your industry’s claim patterns, and the regulatory requirements that apply to your business (a software consultant in Seattle faces entirely different exposures than a roofing contractor, yet both need protection tailored to their actual risks). Your coverage limits, policy structure, and endorsements should reflect the maximum loss your business could reasonably face, not the minimum required by regulation. The scenarios we’ve outlined-slip-and-fall incidents, product injuries, and property damage during service delivery-happen regularly across the Seattle region, and they cost far more than most business owners anticipate.

Contact FirstMark Insurance Group to discuss whether your current coverage reflects today’s claim environment and your actual business exposures. A thorough review takes minimal time and often reveals opportunities to strengthen protection while controlling costs through bundling and documented risk reduction. The right time to evaluate your general liability protection is now, before the next claim arrives.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation