Construction projects face constant exposure to damage, theft, and liability risks that standard property insurance simply doesn’t cover. Builders risk insurance fills this critical gap, protecting your materials, equipment, and operations from the moment work begins.

At FirstMark Insurance Group, we’ve seen too many builders learn this lesson the hard way. The right coverage means the difference between a minor setback and a project-threatening loss.

What Builders Risk Actually Covers

Builders risk insurance protects the physical assets of your construction project from the moment materials arrive on site through final completion. This includes the building structure itself, materials and equipment, temporary structures like scaffolding, and supplies in transit or stored off-site. The policy also covers debris removal after a covered loss and, critically, soft costs such as extended loan interest, lost rental income, or additional real estate taxes that accumulate when property damage delays your project. The builders risk market reached $5.36 billion in 2024, reflecting how seriously the industry takes this protection. Most policies start at around $375 in many states, though your actual premium depends on project cost, property type, location relative to fire services and flood zones, construction materials, and the optional coverages you select.

Where Standard Property Insurance Leaves You Exposed

Your homeowner’s or standard commercial property policy explicitly excludes buildings under construction. Insurers writing general property coverage assume a completed, occupied structure with functioning safety systems-not an active work site with exposed materials, temporary power sources, and constant foot traffic. When theft, weather, or vandalism strikes a project in progress, your standard policy denies the claim. Additionally, standard policies do not cover soft costs at all; if a fire destroys framing and delays your project by six months, your regular insurance won’t reimburse the extra financing costs or lost income. Lenders and government contracts increasingly require builders risk coverage as a condition of funding, recognizing that projects without it face catastrophic financial exposure.

All-Risk Versus Named-Peril Coverage

The distinction between builders risk and standard property insurance runs deeper than exclusions. Builders risk operates on an all-risk basis unless specific perils are excluded, meaning you receive coverage for most claims unless your policy explicitly carves them out. Standard property insurance works the opposite way-it covers only named perils and requires you to prove every single loss falls within the listed coverage. This fundamental difference shapes your protection significantly.

The Real Cost of Gaps in Coverage

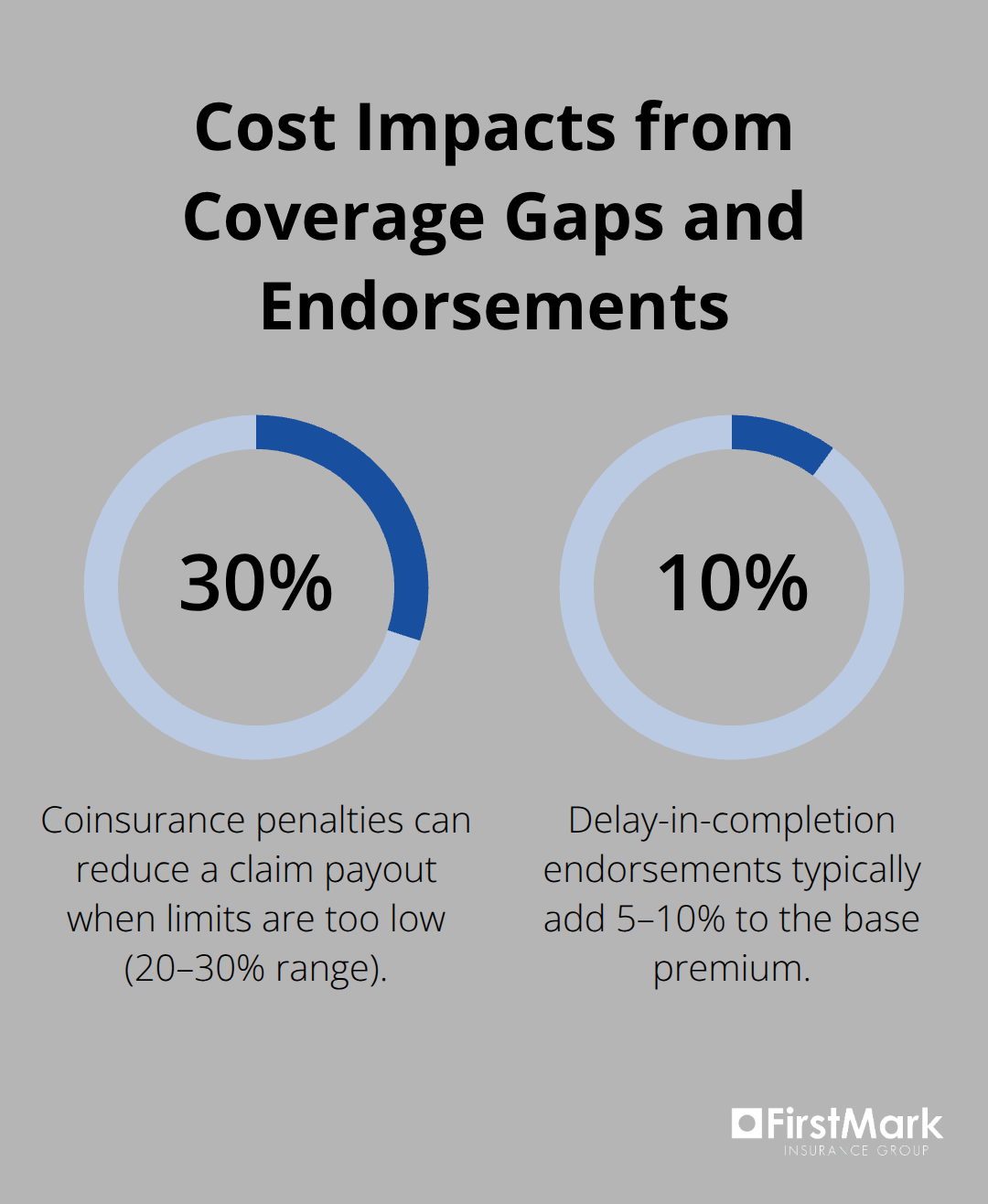

Many contractors and owners assume that because their project is insured somewhere, they’re protected. That assumption costs money. If your policy limits fall short of actual replacement cost (a common mistake when budgets shift mid-project), coinsurance penalties reduce your claim payout by 20 to 30 percent or more. If you fail to add an endorsement for water mitigation technology, modern underwriters will impose higher deductibles or deny coverage entirely for water-related losses.

If debris removal isn’t included and a storm destroys materials, you pay cleanup costs out of pocket.

Building Your Protection Strategy

The solution is straightforward: work with an experienced broker who understands construction risk and can inventory your exposures across every project phase, from site preparation through closeout. This person identifies gaps before they become expensive problems and ensures your coverage matches your actual risk profile. The right partnership protects your timeline and budget while giving you confidence that your project has the protection it needs. Understanding what your policy covers is only half the battle-knowing what it doesn’t cover matters just as much.

What Your Builders Risk Policy Actually Protects

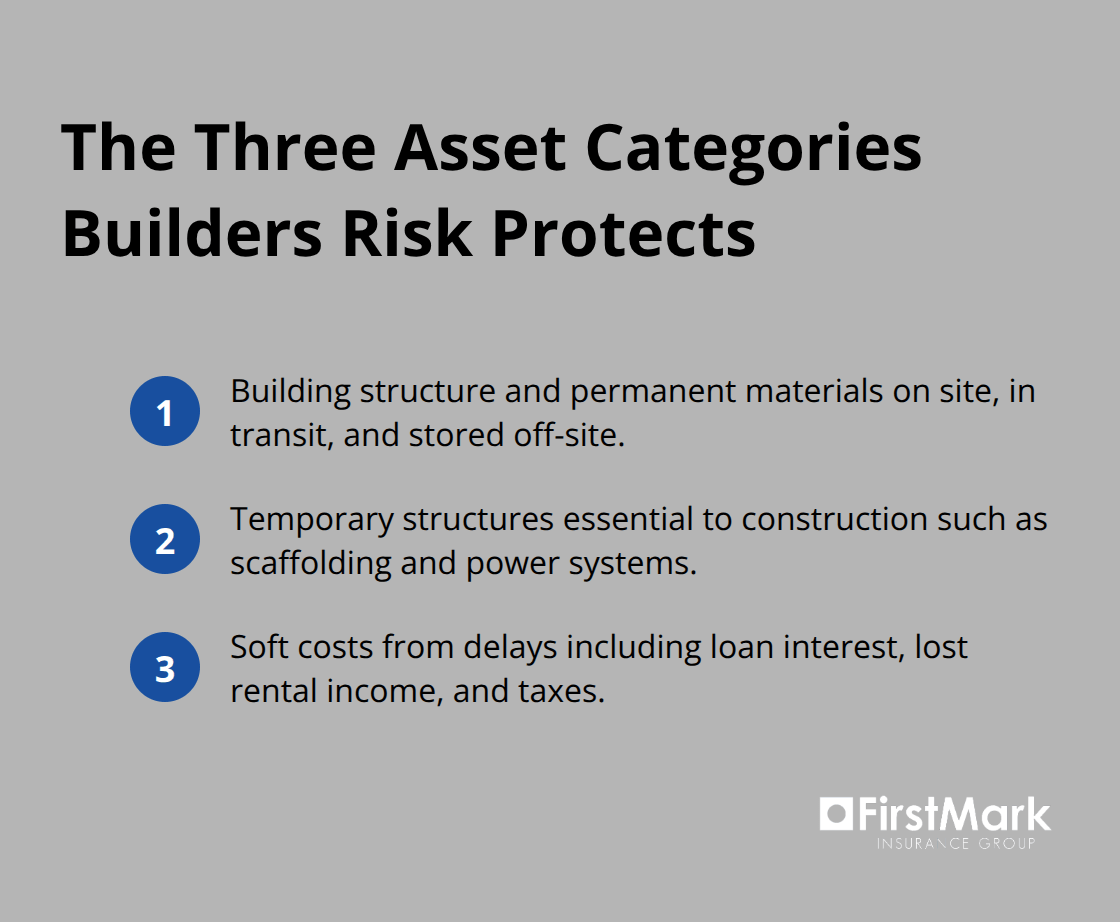

Builders risk insurance protects three distinct categories of project assets, and understanding where each category begins and ends prevents costly coverage gaps.

The Building Structure and Permanent Materials

Your policy covers the building structure itself from the foundation through framing, mechanical systems, and permanent fixtures intended to remain in place after completion. This includes materials and equipment on site that will become part of the finished building, from lumber and drywall to HVAC units and electrical panels. Coverage extends to materials in transit between suppliers and your job site, as well as materials stored off-site before installation. A six-month project can move thousands of dollars in materials through multiple locations, and your policy protects them at each stage.

Temporary Structures That Support Your Work

Your policy covers temporary structures essential to the construction process, including scaffolding, temporary power systems, equipment sheds, and site fencing. Many contractors overlook this category and discover mid-project that damage to scaffolding or temporary facilities falls outside their coverage. These structures represent significant capital investment and, when damaged, can halt work entirely. Experienced builders risk underwriters recognize this exposure and include temporary structure protection as standard in most policies.

Soft Costs That Accumulate During Delays

Soft costs accumulate when property damage delays your project-extended loan interest, lost rental income if the building was meant to generate revenue, additional real estate taxes, and carrying costs on financing. A six-month delay on a $2 million residential project can cost $15,000 to $25,000 in soft costs alone, yet many policies exclude this protection unless you specifically request it as an endorsement. These costs often exceed the physical damage itself, making them the hidden threat to your project budget.

What Your Policy Explicitly Excludes

The critical mistake most contractors make is assuming their policy covers labor costs or worker injuries. Builders risk insurance explicitly excludes workplace accidents and bodily injury claims. If a worker is injured on your site, that claim falls to general liability or workers compensation insurance, not your builders risk policy. This separation means you need multiple policies working together, not one catch-all protection.

Additionally, most standard builders risk policies do not cover consequential losses from delays. If a supply chain disruption halts your project for three weeks, your insurance won’t cover the cost of keeping your crew paid or renting temporary equipment elsewhere. Experienced underwriters now offer delay-in-completion endorsements and soft cost extensions specifically to address these gaps, though they typically add 5 to 10 percent to your base premium.

Inventory Your Exposures Before You Purchase

The key is to inventory every phase of your project before purchasing coverage: what materials arrive first, where they’re stored, which temporary structures support the work, and which soft costs would accumulate if a loss occurred. That inventory becomes your roadmap for endorsements and coverage limits that actually match your exposure. When you work with an experienced broker, we help you map these exposures across every project phase and identify the specific endorsements that close gaps before they become expensive problems. This preparation determines whether your coverage protects your timeline and budget or leaves you exposed when damage strikes.

What Actually Happens When Damage Strikes

Weather damage remains the most frequent builders risk claim, and the data tells a stark story. According to the National Weather Service, severe thunderstorms, hail, and high winds cause an estimated $10 billion in annual property damage across the United States, with construction sites experiencing disproportionate losses because exposed structures lack the protection of finished buildings. A roofless residential frame takes the full force of a summer hailstorm; materials stored under temporary tarps offer minimal protection against driving rain.

The Financial Impact of Weather Events

Projects suffer severe losses when weather strikes. We’ve observed projects where a single weather event destroyed $50,000 to $150,000 in materials and set timelines back months. The combination of material replacement costs and project delays creates a compounding financial burden that standard property insurance won’t address. Extended financing costs, lost rental income, and additional real estate taxes accumulate while contractors wait for materials to arrive and crews to resume work.

Theft and Vandalism: The Hidden Drain on Budgets

Theft and vandalism operate differently than weather damage. The National Insurance Crime Bureau reports that theft losses on active construction sites average $400 to $1,000 per incident, with copper wiring, HVAC equipment, and power tools representing the highest-value targets. A single night of theft can strip thousands in materials from a site, and the financial damage extends beyond replacement cost-your project halts while you reorder and reschedule installation, compressing your timeline and inflating labor costs.

Vandalism often accompanies theft; spray paint on finished walls, broken windows, and damaged temporary structures create secondary costs that many contractors fail to budget for. These secondary expenses mount quickly and can exceed the original theft loss itself.

Worker Injuries and Liability Claims Fall Outside Builders Risk

The critical distinction separates weather and theft losses from accidents involving workers or site visitors, which fall entirely outside builders risk coverage. If a worker is injured on your site, that claim belongs to workers compensation insurance. If a delivery driver or site visitor slips and is injured, general liability insurance handles that exposure. Builders risk protects the physical assets of your project, not the people working on or visiting it.

Many contractors mistakenly believe a single policy covers everything and discover mid-claim that their builders risk policy explicitly excludes bodily injury claims. This gap creates real exposure: a serious injury can generate $100,000 to $500,000 in liability costs, and without proper general liability coverage, those costs come directly from your business.

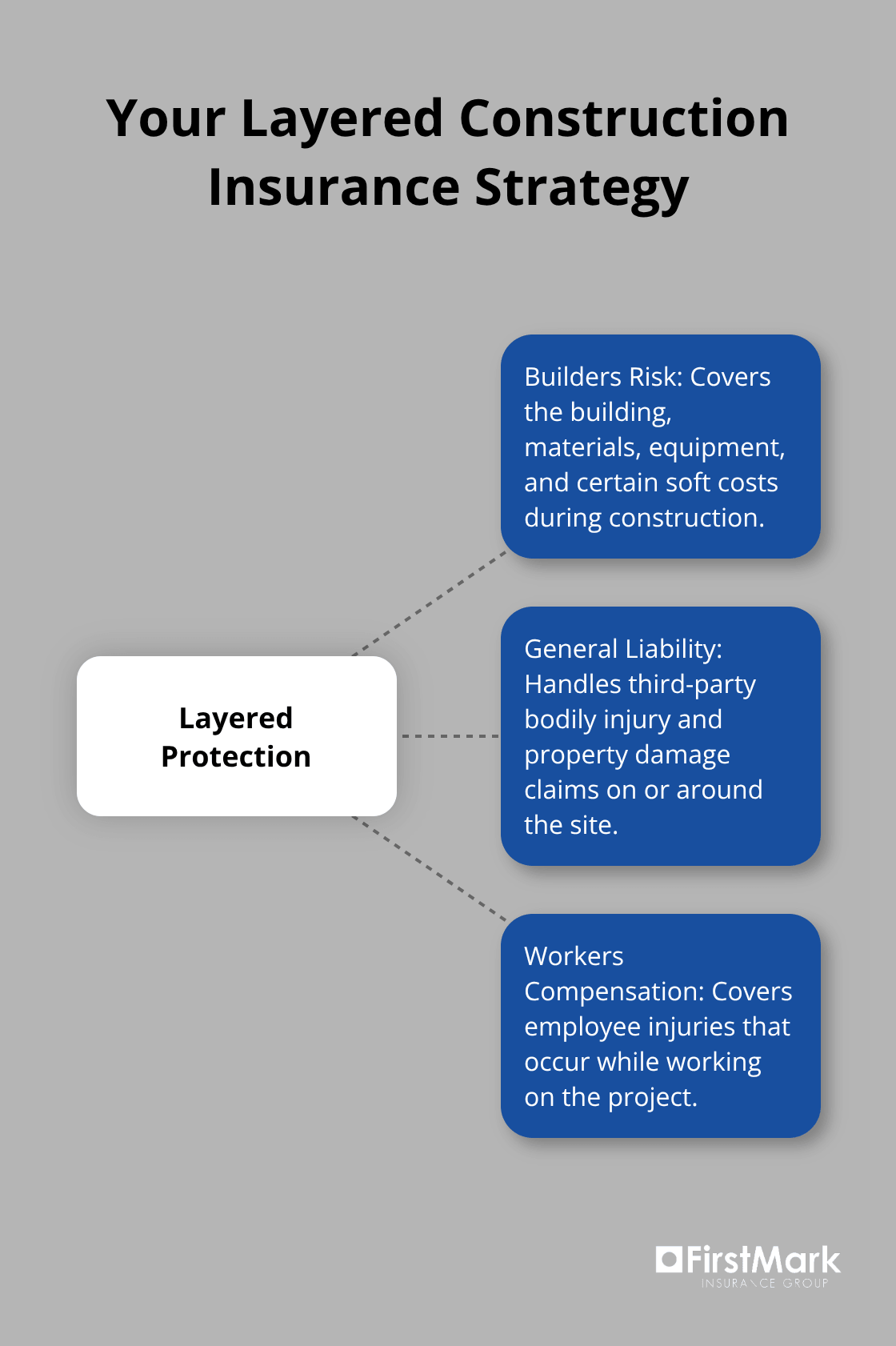

Building a Layered Protection Strategy

The practical reality is that builders risk works as part of a layered protection strategy. Your builders risk policy covers the building, materials, equipment, and soft costs from delays. Your general liability policy covers third-party bodily injury and property damage claims. Your workers compensation policy covers employee injuries.

Each policy serves a distinct purpose, and gaps between them create exposure.

The most effective contractors and builders establish this layered approach before breaking ground, ensuring that every exposure-weather damage, theft, accidents, and liability-falls under some form of coverage. This preparation prevents the costly discovery that a particular loss falls outside your protection when damage strikes.

Final Thoughts

Construction project builders risk insurance protects your timeline and budget when weather, theft, or accidents strike. Evaluate your current coverage honestly: confirm that your policies cover materials in transit, temporary structures, and soft costs from delays, and verify that your coverage limits match your actual replacement costs. Most contractors discover during this review that their coverage falls short in at least one critical area-water mitigation endorsements, debris removal, or soft cost extensions that seem minor until a loss occurs.

Contact an experienced insurance partner who understands construction risk and can review your specific project exposures. At FirstMark Insurance Group, we inventory your exposures upfront and recommend endorsements that close gaps before they become expensive problems. Your project deserves protection that matches its actual risk profile, and that protection starts with a conversation about what your current coverage does and doesn’t include.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation