Technology professionals face distinct liability exposures that standard business policies simply don't address. A single coding error, data breach, or missed security vulnerability can trigger claims that exceed typical coverage limits and leave your business exposed.

At FirstMark Insurance Group, we've seen how tech industry professional liability gaps create real financial and reputational damage. The right specialized coverage protects what you've built.

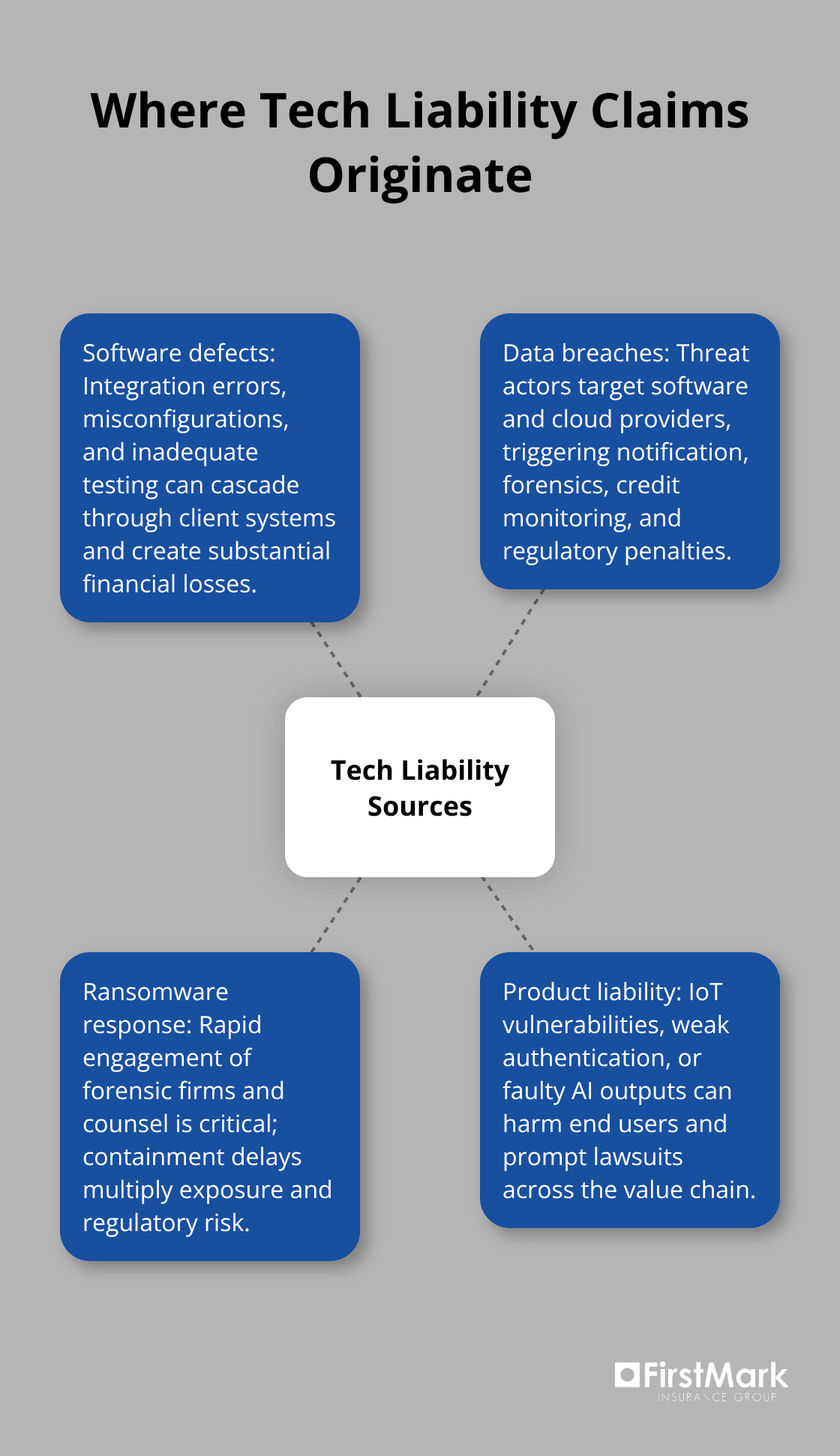

Where Tech Liability Claims Actually Originate

Software Defects and Integration Failures

Software defects rank among the costliest exposures in technology services. A single integration error, API misconfiguration, or inadequate testing can cascade through client systems and trigger substantial financial losses. These scenarios happen regularly across the industry, not in theory alone. When a client's platform experiences downtime due to faulty code deployment, the financial impact extends far beyond your direct costs. Recovery expenses, lost revenue claims, and reputational harm accumulate quickly.

E&O coverage for software development specifically addresses these gaps by covering legal defense, settlements, and damages when your work or advice causes client financial loss. The distinction matters because general liability policies exclude professional services entirely, leaving you fully exposed. Standard business insurance treats your services as incidental, not as the core liability driver they actually represent.

Data Breaches and Incident Response

Data breaches represent the second major liability vector, and the numbers are sobering. Cyber-related claims continue rising as attackers target software companies and cloud service providers with increasing sophistication. A breach affecting customer data triggers notification obligations, forensic investigation costs, credit monitoring services, and potential regulatory penalties that standard policies don't cover.

Ransomware incidents demand rapid incident response-often requiring specialized forensic firms and legal counsel within hours of discovery. Cyber liability insurance covers these immediate response costs, typically engaging preapproved incident response partners within the first hour to contain the damage. This speed matters enormously; delays in containment multiply your exposure and regulatory liability.

Product Liability Across Connected Systems

Product liability claims emerge when flawed code or inadequate security controls cause direct harm to end users. IoT devices with connectivity vulnerabilities, applications with authentication gaps, or AI systems producing incorrect outputs all generate liability exposure that traditional professional liability policies simply don't contemplate. The liability landscape extends across your entire value chain-developers, distributors, and platforms can all face named defendants in product liability lawsuits when technology fails.

A robotic vacuum fire tied to a lithium battery explosion required airlift to a hospital, illustrating severe liability risk from energy storage in home robotics. Interactive toys like Hello Barbie faced privacy claims over recording children's voices without parental consent. Smart home cameras have been hacked in reported incidents, raising privacy and safety concerns and potential liability for manufacturers. These multi-layered exposures demand coverage that specifically addresses technology product risk, not generic business liability frameworks designed for non-technical services.

Why Standard Coverage Misses Technology Risks

Professional Services Exclusions Leave You Exposed

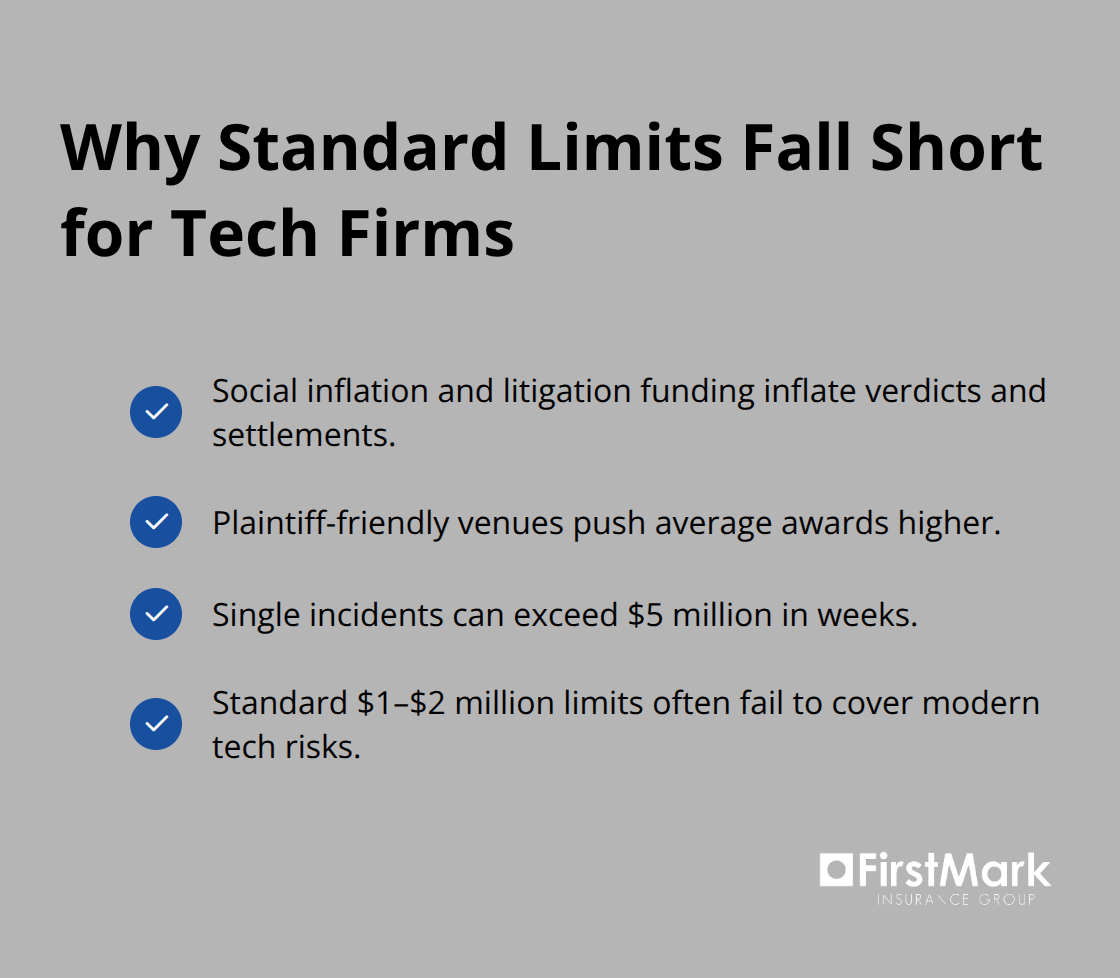

General business liability policies treat professional services as secondary exposures, not primary ones. For technology firms, this fundamental misalignment creates dangerous coverage gaps. Your core business-software development, system integration, cloud services, data management-operates outside the scope of standard commercial policies. Most general liability forms explicitly exclude professional services, meaning claims arising from your actual work receive no coverage whatsoever. You pay premiums for protection that doesn't apply to your largest liability exposures. The distinction between a covered incident and an uncovered claim often hinges on whether your work involved professional judgment or technical expertise, and insurers consistently rule against coverage when technology services are involved. This isn't a minor limitation; it's a structural exclusion that leaves your business entirely exposed to the claims most likely to materialize.

Inadequate Limits Against Rising Claim Severity

Coverage limits present a second critical problem. Standard policies typically cap professional liability at $1 million to $2 million, which sounds substantial until a single data breach or software failure generates claims exceeding $5 million. The professional liability market analysis found that claim severity is rising while frequency remains relatively stable, meaning individual claims are growing larger even as claim counts stay consistent. Social inflation, litigation funding, and plaintiff-friendly jurisdictions drive average awards higher-settlements and verdicts that once seemed exceptional now appear regularly. Technology firms handling sensitive data or operating mission-critical systems face exposure far beyond these inadequate limits.

A mid-market SaaS company experiencing a breach affecting thousands of customers can face notification costs, forensic investigation, credit monitoring services, regulatory penalties, and litigation expenses that dwarf standard policy limits within weeks. Your business needs coverage aligned to your actual financial exposure, not coverage designed for a different industry entirely.

Why Specialized Tech Coverage Addresses These Gaps

Specialized tech professional liability policies address these structural problems directly. They cover claims arising from your professional services, offer limits that scale with your business size and risk profile, and include cyber incident response costs that general policies omit entirely. The right coverage structure includes primary professional liability, layered excess coverage, and integrated cyber protection-a combination that standard policies cannot provide because they were never designed for technology sector risks. This tailored approach protects your business against the specific exposures that actually threaten your operations and financial stability.

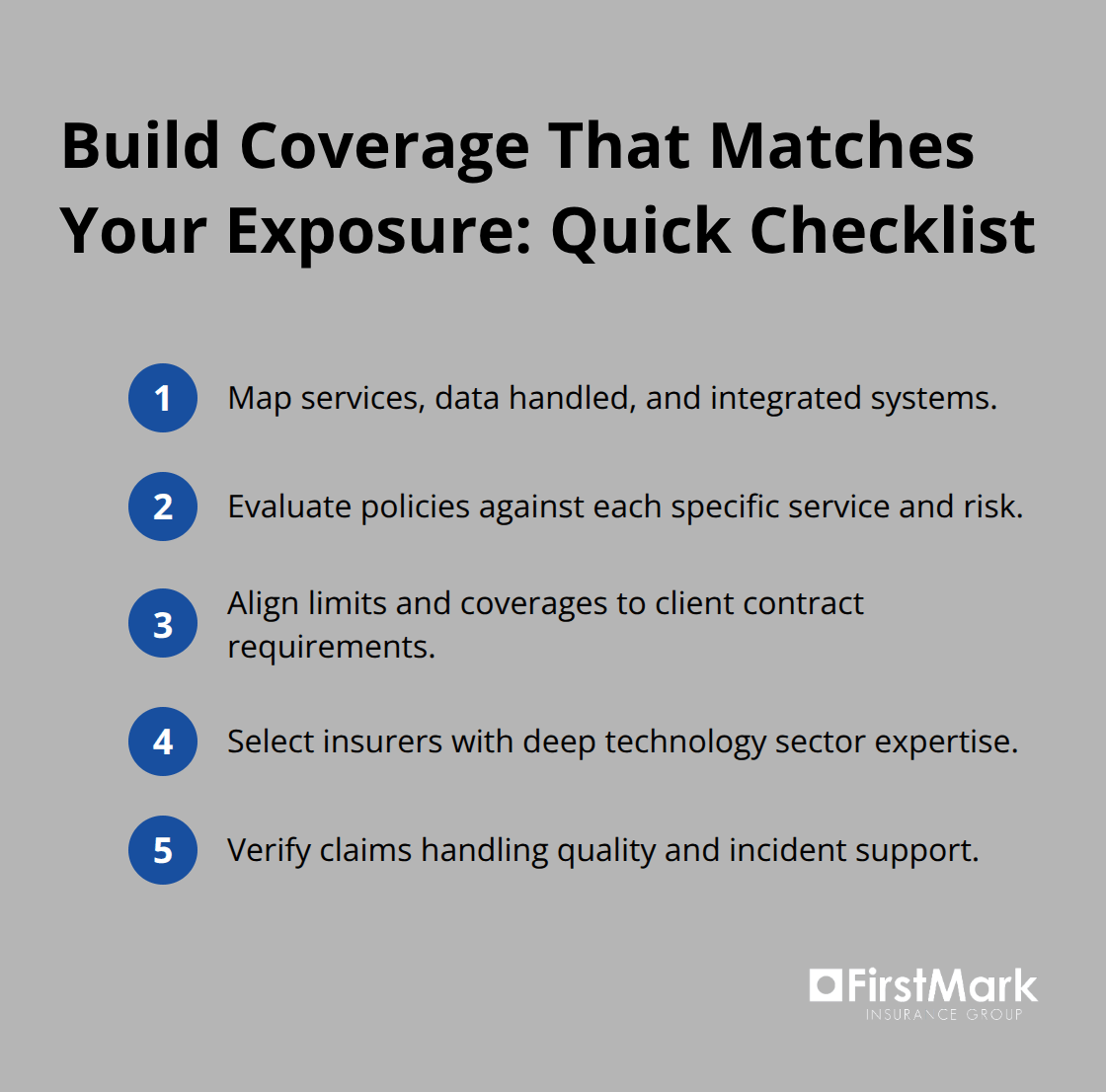

Building Coverage That Matches Your Actual Exposure

Map Your Specific Technology Exposures

Professional liability coverage for technology firms demands precision because generic risk assessments fail to account for the specific technical exposures unique to your business model. A SaaS company handling financial data faces fundamentally different liability vectors than a custom software development shop or a cloud infrastructure provider. The first step involves mapping your actual exposure across three dimensions: the services you deliver, the data you access, and the systems you integrate with.

Document which client operations depend on your work, what happens if your service fails for 24 hours, and which regulatory frameworks govern the data you handle. This exercise transforms abstract risk into concrete exposure figures. A healthcare software vendor must account for HIPAA compliance failures and patient safety implications. A fintech platform must consider transaction integrity and fraud detection responsibilities. A marketing technology firm must evaluate customer data handling and advertising compliance risks. These distinctions determine which coverage provisions matter and what policy limits actually protect your business.

Evaluate Coverage Explicitly Against Your Services

Once you've identified your specific exposures, evaluate whether your current or prospective policy covers them explicitly. Too many technology firms discover coverage gaps only after a claim materializes. Ask insurers directly whether they cover claims arising from AI-assisted work, integration failures with third-party systems, or data breaches affecting client customers. Request sample policy language addressing your specific service offerings.

Claim severity continues rising while frequency remains stable, meaning individual claims grow larger. This trend demands higher coverage limits than technology firms historically purchased. If your business handles customer data or operates mission-critical systems, standard limits of $1 million to $2 million leave you dangerously exposed. Most established technology firms should evaluate primary coverage in the $2 million to $5 million range, with excess layers extending protection to $10 million or higher depending on project values and client requirements.

Align Coverage to Your Client Contracts

Clients increasingly demand proof of adequate coverage as a contract requirement, and many technology vendors face explicit insurance minimums written into service agreements. Review your client contracts now to identify mandated coverage types and minimum limits. This contractual requirement should drive your coverage decisions, not the other way around.

Select Insurers With Technology Sector Expertise

The insurer you select matters as much as the coverage structure itself. Most traditional insurance brokers lack the technical depth to evaluate technology-specific exposures effectively. They apply generic underwriting criteria to specialized risks and often miss critical exposure details. An effective technology insurance partnership requires underwriters who understand software development lifecycles, cloud architecture, data security practices, and the regulatory frameworks governing your industry.

When evaluating potential insurers, assess their technology sector experience directly. How many SaaS companies do they currently insure? What's their claims history in your specific vertical? Do they employ risk engineers with technical backgrounds who can evaluate your development practices and security controls? These specialists understand the difference between a code review process and actual code quality assurance. They recognize that a penetration testing program reduces cyber risk differently than vulnerability scanning. They ask informed questions about your development velocity, your third-party vendor management practices, and your incident response readiness.

This technical sophistication matters enormously when claims materialize. An insurer unfamiliar with technology operations may dispute coverage based on misunderstandings about your technical practices or industry standards. Specialized technology underwriters bring claims experience and technical context that protects you during disputes. They've handled similar claims before and understand the legitimate costs of incident response, forensic investigation, and regulatory compliance.

Verify Claims Handling and Support Quality

Request that potential insurers provide references from comparable technology firms they currently serve. Speak directly with those references about claims handling, responsiveness during incidents, and whether the insurer provided meaningful support beyond just paying bills. This conversation reveals whether you're purchasing coverage from a commodity provider or from a partner genuinely invested in your long-term risk management and business continuity.

Final Thoughts

Technology sector risks demand coverage built specifically for how your business operates, not policies designed for industries with fundamentally different risk profiles. Standard business policies leave you exposed to the claims most likely to materialize-software failures, data breaches, and product liability incidents that generic coverage simply doesn't address. Rising claim severity means individual incidents now generate settlements and defense costs that dwarf traditional policy limits, making tech industry professional liability protection a business necessity rather than an optional expense.

The right coverage structure combines primary professional liability with cyber incident response capabilities and excess layers that scale with your business growth. Selecting an insurer with genuine technology sector expertise matters equally-underwriters who understand your development practices, your data security challenges, and the regulatory frameworks governing your industry provide meaningful support during claims, not just policy documents. Your client contracts likely already mandate specific coverage types and minimum limits; use those requirements as your starting point, then build coverage that exceeds those minimums based on your actual financial exposure.

We at FirstMark Insurance Group guide technology firms through this process with clarity and expertise. Our experience helping businesses navigate insurance complexities means we understand the specific exposures technology companies face and work with top insurance providers to present coverage options that fit your requirements at competitive pricing. Reach out to discuss your tech industry professional liability needs and verify that your coverage actually protects what you've built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation