Owning a horse property in Washington means protecting far more than a standard home. Your stables, pastures, and animals face distinct risks that typical homeowners policies simply don’t cover.

At FirstMark Insurance Group, we understand that Washington horse property insurance requires specialized expertise. The right coverage transforms uncertainty into confidence, letting you focus on what matters most.

Why Standard Homeowners Policies Fall Short for Horse Properties

Barn Structures and Outbuilding Limitations

Horse properties in Washington operate under fundamentally different risk profiles than typical residential homes, and standard homeowners insurance simply doesn’t account for these differences. Your barn structures face specific perils that insurers classify separately from main dwellings. A barn constructed with wood framing and metal roofing presents distinct fire risks compared to your home, yet most homeowners policies lump all structures into one inadequate limit.

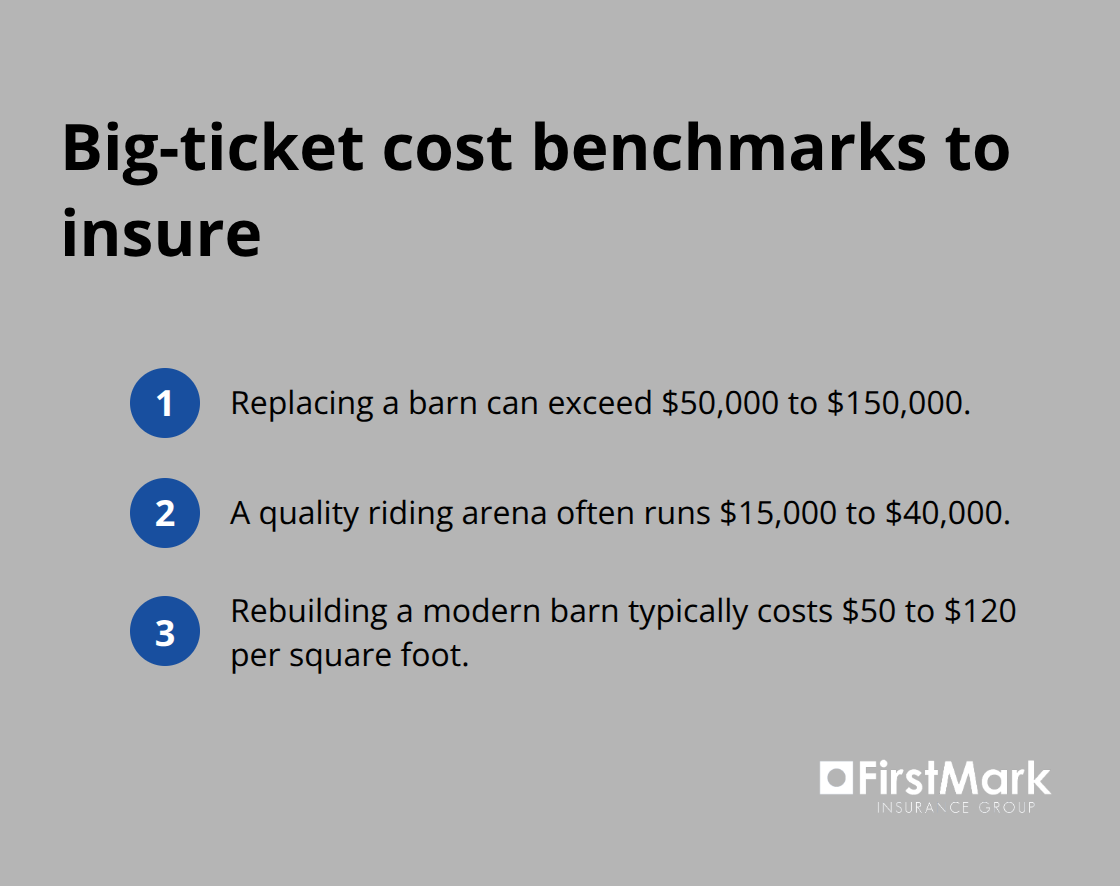

Standard policies typically cap outbuildings at 10 to 15 percent of your dwelling coverage, which proves catastrophically insufficient when a single barn replacement can exceed $50,000 to $150,000 depending on size and materials. Pasture fencing, arena surfaces, and water facilities require their own coverage considerations that homeowners policies simply ignore.

The Liability Gap That Homeowners Policies Create

Horses introduce liability exposure that homeowners policies explicitly exclude. If a horse causes injury to a visitor, damages a neighbor’s property, or injures someone during a riding lesson or boarding situation, your standard homeowners liability protection won’t respond. Washington courts have consistently upheld that equine-related incidents fall outside standard residential liability coverage, leaving owners personally responsible for damages that can easily reach six figures.

A rider thrown from a horse resulting in spinal injury or a boarding horse escaping and causing vehicle damage represents precisely the scenarios your current policy won’t cover. These incidents occur regularly across Washington’s equestrian community, yet most horse owners remain unaware their homeowners policy provides zero protection.

High-Value Animals Left Completely Unprotected

Your horses constitute high-value assets requiring separate protection that homeowners policies don’t provide. Equine mortality insurance and medical coverage for horses operate completely independently from property insurance, yet many owners mistakenly believe their homeowners policy addresses these needs. A competition horse valued at $25,000 to $75,000 receives zero protection under standard homeowners coverage, meaning sudden illness or accident results in total financial loss.

This protection gap affects casual horse owners and serious competitors alike. Whether your horse represents a cherished companion or a significant investment, standard homeowners coverage leaves you financially exposed. Understanding these limitations becomes the first step toward securing the specialized protection your Washington horse property actually requires.

What Coverage Actually Protects Washington Horse Properties

Specialized horse property insurance in Washington addresses the exact risks that standard policies ignore, and the distinction matters enormously when an incident occurs. Barn structures require dedicated coverage limits because replacement costs dwarf what homeowners policies allocate to outbuildings. A modern horse barn in Washington typically costs $50 to $120 per square foot to rebuild, yet standard policies cap outbuilding coverage at 10 to 15 percent of dwelling limits. Horse property insurance removes this artificial restriction and allows you to set barn coverage independently based on actual replacement value. This means a properly valued barn receives full protection rather than the $8,000 to $12,000 a homeowners policy might provide.

Protecting Structures and Land That Standard Policies Exclude

Pasture fencing, arena surfaces, shelters, and water systems represent substantial investments that homeowners policies treat as maintenance rather than insurable property. A quality arena with proper drainage and footing runs $15,000 to $40,000 to construct, yet most homeowners policies provide zero coverage for these improvements. Specialized horse property policies cover these specific assets, recognizing them as essential infrastructure for equestrian operations. Additionally, pasture and land coverage extends beyond fencing to include permanent improvements like drainage systems, gates, and pasture development. This distinction proves critical in Washington’s wet climate where proper drainage infrastructure directly prevents property damage and animal health problems.

Medical and Mortality Protection for High-Value Animals

Equine mortality and medical insurance operates separately from property coverage because horses require their own underwriting and risk assessment. Mortality insurance covers sudden death from accident, illness, or natural causes, protecting against the complete loss of a horse valued anywhere from $5,000 for recreational animals to $50,000 or more for competition or breeding stock. Medical insurance covers veterinary treatment for illness or injury, with policies typically offering coverage limits between $2,500 and $15,000 annually depending on the plan selected. These policies work in tandem with property insurance to create comprehensive protection across all aspects of horse ownership.

Evaluating Coverage Limits for Your Operation

Washington horse owners should evaluate coverage limits based on the number of animals they own, their individual values, and their intended use (whether recreational riding, boarding operations, or competitive activities). The right limits reflect your actual exposure rather than generic industry standards. A boarding operation with ten horses faces different coverage needs than a single-horse owner, and competition animals require different protection than pasture companions. Working with specialists who understand equestrian operations helps you identify the specific coverage gaps that affect your property and animals.

What Actually Drives Horse Property Insurance Costs in Washington

Location and Climate Shape Your Premium Foundation

Washington horse owners face premiums shaped by factors that differ fundamentally from standard homeowners insurance, and understanding these variables gives you real leverage to reduce what you pay. Your property location within Washington creates the first major cost driver, particularly regarding climate exposure and local hazard frequency. Properties in western Washington’s wet zones face higher premiums due to moisture-related barn deterioration and pasture drainage challenges, while eastern Washington properties encounter different risk profiles centered on wildfire exposure and extreme temperature swings.

The National Interagency Fire Center reports that Washington experiences an average of 2,000 wildfires annually, with many occurring in rural areas where horse properties cluster, directly raising insurance costs for properties within high-risk zones. Conversely, properties in lower-risk areas with established fire suppression infrastructure qualify for meaningful premium reductions. Your specific distance from fire stations, water sources, and emergency services determines your actual risk rating, not generic assumptions about your county. Properties within five miles of fire stations typically receive 15 to 25 percent lower premiums than comparable properties in remote locations, according to insurance rating guidelines across the industry.

Facility Maintenance Unlocks Substantial Savings

Facility maintenance and safety infrastructure represent the most controllable cost factors available to horse owners, and insurers reward concrete improvements with substantial premium reductions. A well-maintained property with proper drainage systems, cleared vegetation around structures, and functional fencing costs significantly less to insure than properties with deferred maintenance and visible deterioration.

Specific improvements that reduce premiums include installing fire suppression systems in barns, maintaining pasture perimeter fencing in good condition, implementing proper waste management systems, and keeping pasture vegetation cleared of dead trees and brush that could fuel fire spread. Boarding operations that maintain detailed records of animal care, veterinary protocols, and liability waivers for clients receive preferential rates because documentation demonstrates professional risk management.

Bundling Policies Delivers Measurable Cost Reductions

Combining your horse property insurance with homeowners coverage and other policies through the same agency typically generates 10 to 20 percent savings compared to purchasing policies separately across multiple insurers. This approach strengthens your overall protection while reducing your total insurance expenditure. An experienced insurance agency can evaluate your complete picture to identify these opportunities and present options that work for your specific situation.

Final Thoughts

Washington horse property insurance protects what standard policies leave exposed, addressing the exact gaps that affect horse owners across the state. A single incident involving your barn, pastures, or animals can create financial devastation that homeowners coverage simply won’t address. Working with specialists who understand equestrian operations rather than treating horse properties as residential afterthoughts makes the difference between adequate protection and catastrophic exposure.

At FirstMark Insurance Group, we’ve spent 30 years helping families and businesses navigate insurance complexities with confidence. We recognize that horse ownership represents both passion and significant financial investment, and your coverage should reflect that reality. Contact us to discuss how comprehensive Washington horse property insurance protects your stables, pastures, and the animals you care for.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation