Contractor insurance quotes in Washington require careful evaluation-the wrong coverage can leave your business exposed to significant financial risk. At FirstMark Insurance Group, we’ve helped countless contractors navigate this process and identify policies that actually protect their operations.

Getting competitive quotes means understanding what you need, not just comparing prices. This guide walks you through the essentials so you can make an informed decision.

What Coverage Do Washington Contractors Actually Need

State-Mandated Coverage Requirements

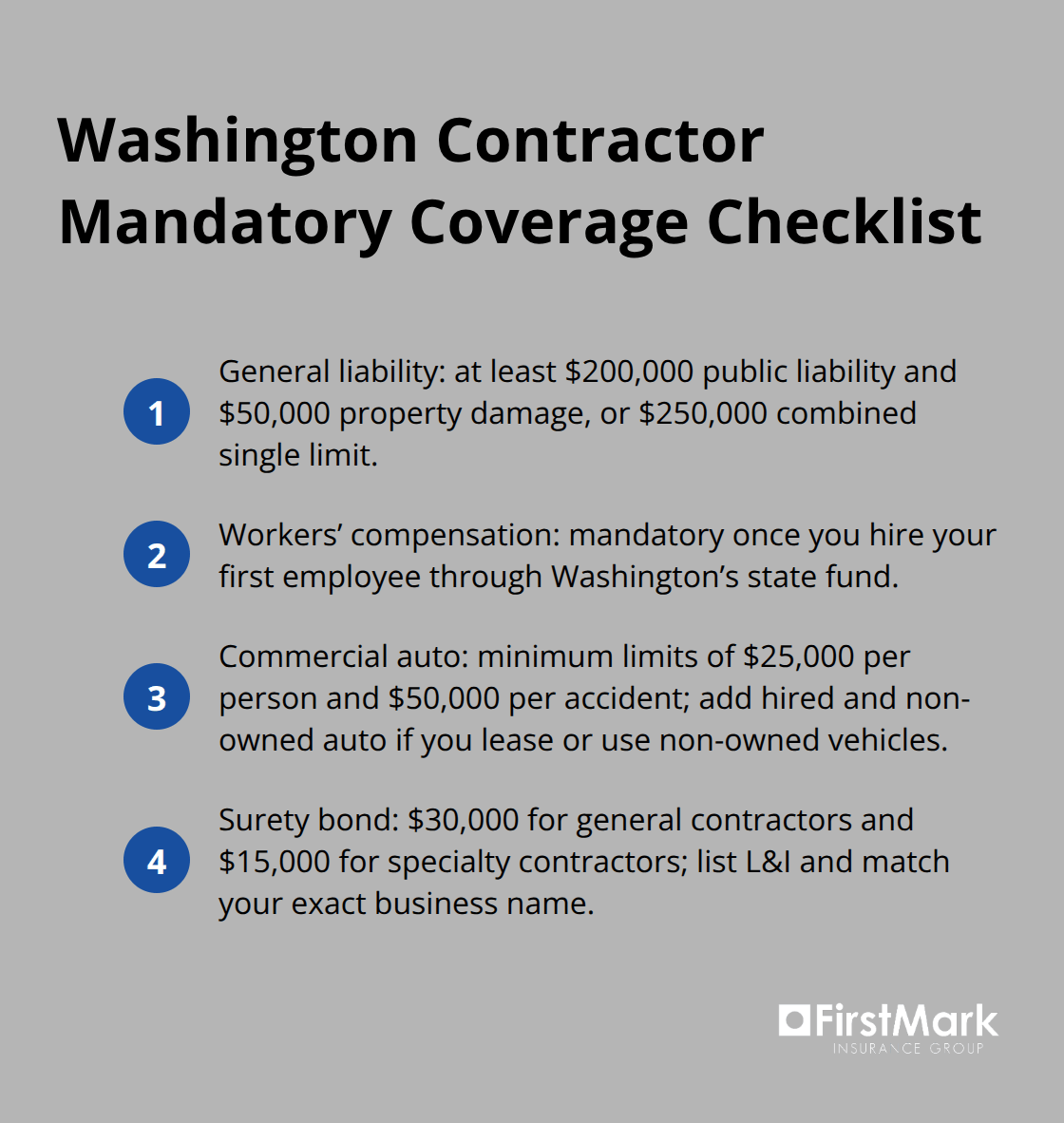

General liability insurance is non-negotiable in Washington. The Department of Labor & Industries sets the minimum at $200,000 in public liability and $50,000 in property damage, or a combined single limit of $250,000.

Your L&I registration won’t move forward without proof of this coverage-it’s a licensing requirement, not optional. Workers’ compensation becomes mandatory the moment you hire your first employee. Washington operates through a state fund monopoly, so you cannot shop between carriers for basic coverage. You can, however, add employer’s liability coverage through a private endorsement if you want additional protection against workplace injury lawsuits.

Commercial auto insurance with minimum limits of $25,000 per person and $50,000 per accident applies to any vehicle you use in your business. If you lease or use vehicles you don’t own, hired and non-owned auto coverage fills that gap. The surety bond requirement-$30,000 for general contractors and $15,000 for specialty contractors-must list L&I as the certificate holder and match your exact business name.

Beyond the Minimum: Additional Protections

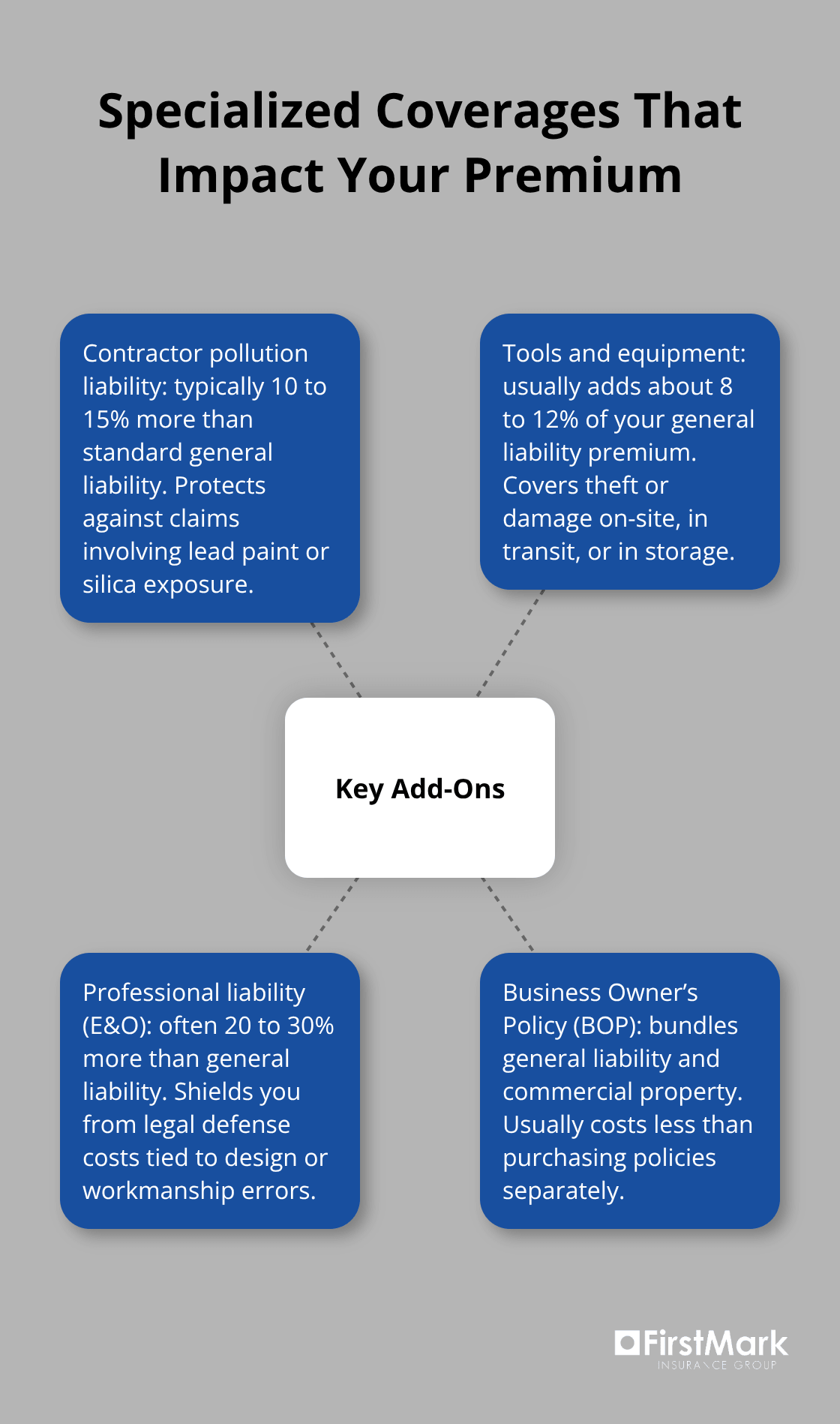

Contractor pollution liability insurance protects you against contamination claims, a real concern if you work with asbestos, lead paint, or silica dust. Tools and equipment insurance reimburses repair or replacement for gear lost or damaged on-site, with coverage most favorable for tools under five years old and equipment valued under roughly $10,000. Professional liability coverage (errors and omissions) shields you from legal fees when clients sue over design mistakes or workmanship failures-something general contractors should treat as mandatory rather than optional.

Builder’s risk insurance covers structures in progress and materials during construction, protecting against fire, vandalism, and weather damage that your general liability won’t touch. A Business Owner’s Policy bundles general liability and commercial property coverage, reducing your overall premium compared to purchasing policies separately.

How Premiums Vary and What You’ll Pay

Premium costs vary significantly based on your building construction type, property value, business revenue, company size, claims history, and coverage limits. Two contractors with identical operations can pay vastly different rates. Average costs run around $115 monthly for general liability and $163 for commercial auto according to data from Insureon, but your actual rate depends on those variables.

When you shop for quotes, bring your payroll information, revenue figures, and lease details ready so providers can quote accurately. Multiple carriers offer different coverage quality and responsiveness, and the cheapest option often means slower claims processing or less thorough coverage review when you actually need help. FirstMark Insurance Group explores offerings from top insurance providers to present you with choices that fit your requirements at the best available pricing.

The decisions you make about coverage limits and policy combinations directly shape how well your business weathers unexpected events. Understanding these options positions you to move forward with confidence when you compare quotes from different providers.

Getting the Right Quotes Without Wasting Time

Prepare Your Business Details Before Requesting Quotes

Shopping for contractor insurance quotes in Washington requires you to know exactly what to request and how to evaluate what you receive. Most contractors request generic quotes without specifying their operation details, which results in inflated estimates or coverage gaps that don’t match their actual needs. When you contact providers, have your business structure, annual revenue, number of employees, types of projects you handle, and equipment value ready to share. Vague applications lead to conservative quotes that overestimate your risk. The Washington Department of Labor & Industries requires L&I to be listed as a certificate holder on your general liability policy, so confirm that requirement is met in every quote you review.

Request Quotes From Multiple Carriers

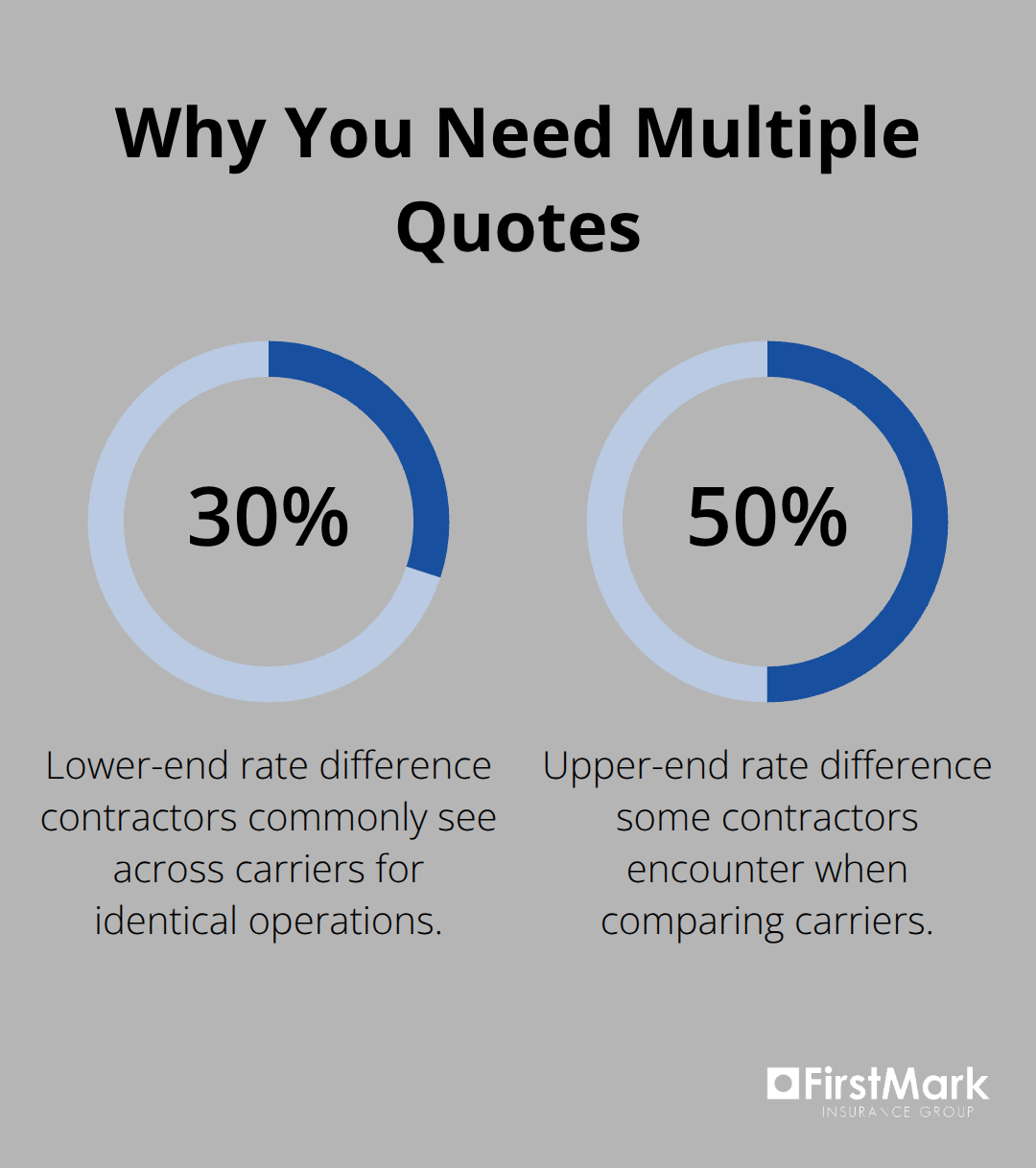

Premium variation between carriers is substantial-two contractors with identical operations routinely see rate differences of 30 to 50 percent depending on how each insurer assesses construction risk and claims history. This means you must request quotes from at least three providers if you want competitive pricing. Online quote tools from established carriers deliver initial estimates within minutes, but they rarely capture the nuances of your specific operation.

A contractor working on residential remodels faces different risks than one handling commercial HVAC installations, and generic online tools often miss these distinctions. Established insurance agencies explore offerings from top insurance providers to present you with choices that fit your requirements at the best available pricing, ensuring you receive quotes tailored to your actual business model rather than industry assumptions.

Evaluate Coverage Quality Beyond Price

When you compare quotes, look beyond the monthly premium to what each policy actually covers and how responsive the carrier is when claims arise. Some providers offer lower rates because they handle claims more slowly or impose stricter limitations on coverage. Ask each provider about their average claims processing time, whether they offer 24/7 support, and what additional endorsements they recommend for your specific trade. A contractor pollution liability policy costs roughly 10 to 15 percent more than standard general liability, but protects you if a client sues over lead paint or silica exposure-skipping this coverage to save money creates exposure that far exceeds the premium savings.

Add Specialized Coverage Where It Matters

Tools and equipment insurance typically costs between 8 and 12 percent of your general liability premium and covers theft or damage on-site, in transit, or in storage, making it worthwhile if you carry equipment valued over $5,000. Ask each provider whether they offer bundled coverage through a Business Owner’s Policy, which combines general liability and commercial property protection and usually costs less than purchasing policies separately. Request quotes that show the same coverage limits across all providers so you can compare apples to apples-requesting $250,000 combined single limit general liability from one carrier and $200,000 public liability from another creates confusion and prevents meaningful comparison.

Document and Rank Your Options

Document each quote with the carrier name, coverage limits, deductibles, annual premium, and any exclusions or limitations specific to construction work. After you gather three or more quotes, rank them not by price alone but by the combination of price, coverage comprehensiveness, and carrier reputation for claims responsiveness. The quotes you collect now form the foundation for the next critical step: understanding which policy features actually matter most for your specific trade and project types.

Common Mistakes Contractors Make When Buying Insurance

Requesting Minimum Coverage Limits Creates Hidden Exposure

Contractors in Washington routinely request the minimum coverage limits required by L&I and assume that satisfies their actual risk. That threshold protects L&I’s public interest, not your business. A single lawsuit from a client injured on your job site can easily exceed $250,000, leaving you personally liable for the difference. Contractors who handle residential remodels or commercial HVAC work face claims routinely exceeding $500,000, which means carrying only the state minimum is financial negligence.

When you shop for quotes, request $1,000,000 in general liability coverage instead. The premium difference between $250,000 and $1,000,000 is typically 15 to 25 percent annually, yet that additional coverage protects your business assets and personal finances against catastrophic loss. Requesting quotes at the legal minimum creates artificially low premium comparisons that obscure your actual protection gap.

Ignoring Trade-Specific Coverage Gaps Leaves You Exposed

A roofing contractor faces fall hazards and weather-related damage claims that differ fundamentally from an electrician’s electrocution risks or a plumbing contractor’s water damage liability. Generic online quote tools assess construction risk broadly and miss these distinctions entirely, producing quotes that either overestimate your risk or leave you exposed. Contractor pollution liability insurance, which covers lead paint and silica dust claims, costs roughly 10 to 15 percent more than standard general liability but becomes non-negotiable if you work with older buildings or perform demolition.

Tools and equipment insurance typically costs 8 to 12 percent of your general liability premium and covers theft or damage on-site. Contractors frequently skip it to save $100 to $150 annually, then face $5,000 to $15,000 losses when equipment is stolen from a job site. Professional liability coverage for design or workmanship errors costs roughly 20 to 30 percent more than general liability but shields you from legal defense costs that often exceed $50,000 even when claims are ultimately dismissed.

When you request quotes, specify your exact trade, the types of projects you handle, and any specialized work like asbestos removal or lead abatement so providers can recommend coverage that actually matches your exposure.

Prioritizing Price Over Claims Service Backfires When You Need Help

Two carriers quoting $200 monthly for identical coverage limits rarely deliver identical service when you file a claim. Some providers process claims within 48 hours while others take two to three weeks, and the difference in cash flow impact during a dispute is substantial. Ask each provider their average claims processing time and whether they offer 24/7 support before you compare premiums.

A carrier charging $20 more monthly but processing claims in two days generates $240 annual premium difference against potential weeks of delayed payment if a claim arises. Additionally, lower-priced quotes sometimes come with stricter claim denials or coverage exclusions buried in the policy language. When you gather quotes, request the same coverage limits and deductibles from each carrier so pricing reflects genuine rate differences rather than coverage variations, then rank your options by the combination of price, carrier reputation for claims responsiveness, and coverage comprehensiveness rather than price alone.

Final Thoughts

Finding the right contractor insurance quotes in Washington requires you to understand your actual coverage needs rather than settle for legal minimums, request quotes that reflect your specific trade and project types, and evaluate carriers based on claims service quality alongside premium cost. Contractors who navigate this process effectively prepare their business details before requesting quotes, gather estimates from at least three providers, and compare coverage comprehensively rather than chase the lowest price. Requesting $1,000,000 in general liability instead of the $250,000 state minimum typically costs 15 to 25 percent more annually but protects your personal assets against catastrophic loss.

Adding trade-specific coverage like contractor pollution liability or professional liability fills gaps that generic policies miss entirely, and verifying that each carrier processes claims within 48 hours matters far more than saving $20 monthly on a premium. You should gather your business structure, annual revenue, employee count, equipment value, and project types, then contact three established insurance providers with identical coverage requests so you can compare apples to apples. Document each quote with the carrier name, coverage limits, deductibles, and annual premium, then rank your options by the combination of price, coverage comprehensiveness, and carrier reputation rather than price alone.

At FirstMark Insurance Group, we help contractors identify coverage gaps specific to your trade, compare quotes that actually match your needs, and secure policies that protect your business and clients. Rather than navigating online quote tools alone, we explore offerings from top insurance providers to present you with choices that fit your requirements at the best available pricing. Contact FirstMark Insurance Group to discuss your contractor insurance quotes Washington needs and receive tailored quotes from carriers committed to responsive claims service.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation