Horse farms in Washington face real liability exposure that most property insurance policies simply don’t address. A single incident-a guest thrown from a horse, property damage during a riding event, or an employee injury-can create financial devastation without proper protection.

At FirstMark Insurance Group, we’ve seen how equine liability insurance WA fills the gaps that standard coverage leaves wide open. This guide walks you through the specific risks on your operation and the protection strategies that actually work.

What Makes Equine Operations Different From Other Farm Businesses

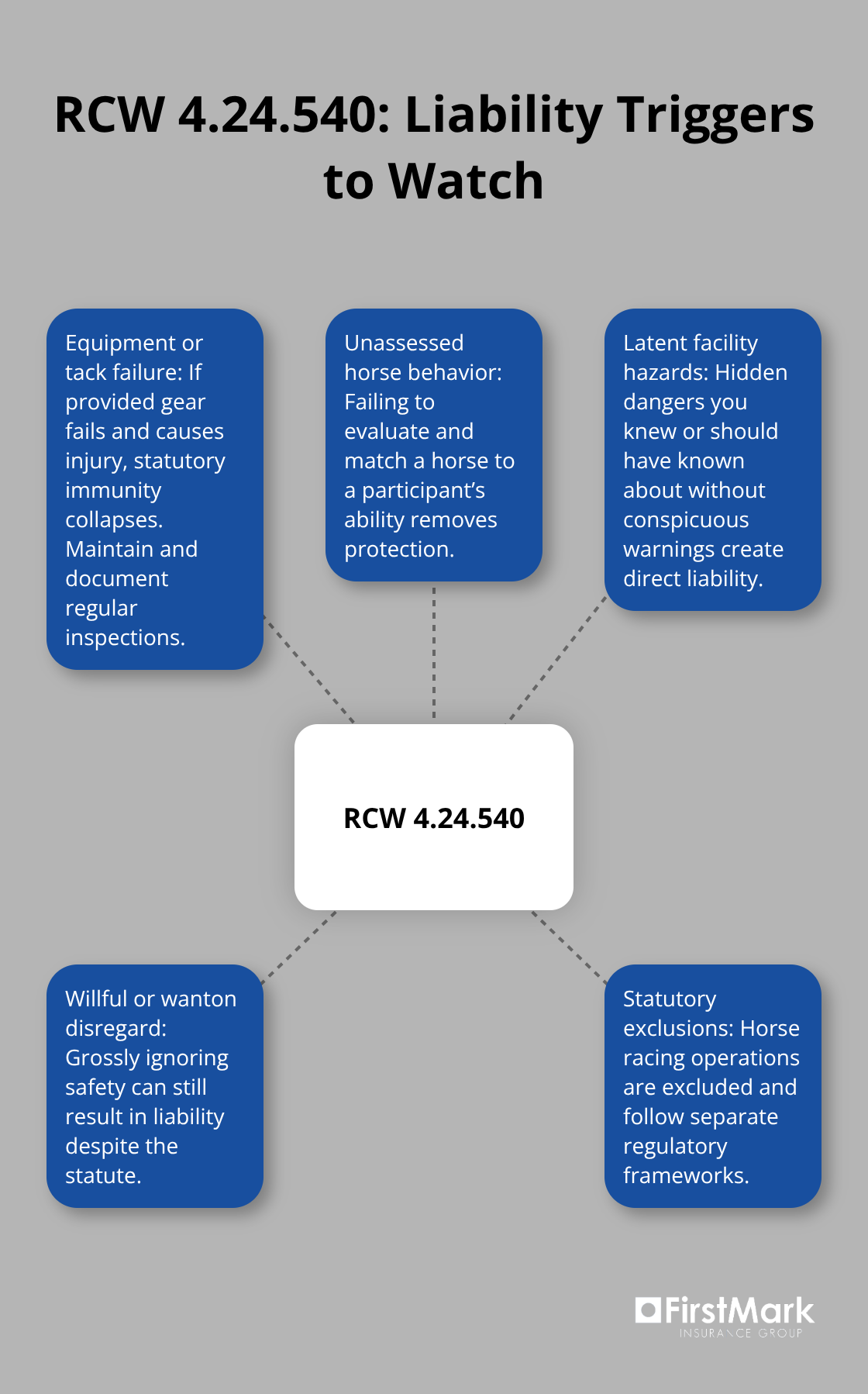

Equine liability differs fundamentally from standard farm exposures because horses create unpredictable hazards that property policies simply don’t contemplate. A guest stepping onto your property for a trail ride faces injury from a spooked animal, a fall from height, or a sudden behavioral shift-risks that fall outside homeowners and standard commercial policies. Washington RCW 4.24.540 provides immunity from liability for equine activity sponsors under specific conditions, but that protection evaporates the moment equipment fails, a horse’s behavior wasn’t properly assessed before the activity, or facilities harbor known hazards without warning signs. This means your farm’s legal shield depends entirely on documented safety practices, not just having horses on the property. The statute also excludes horse racing operations, which fall under separate regulatory frameworks, and liability can still attach if willful or wanton disregard for safety caused the injury.

Many farm owners mistakenly believe their general liability or homeowners policy covers equine activities; it doesn’t. Standard policies explicitly exclude animals kept for business purposes, and they certainly don’t account for the specialized risks of boarding operations, riding instruction, or breeding facilities. The gap between what you think you’re covered for and what actually protects you grows wider when you consider that a single serious injury can exceed $500,000 in medical costs and legal fees. Washington’s file-and-use insurance system means policies can be deployed immediately, but that speed also means policy language matters tremendously-you need wording that explicitly addresses equine liability, care and custody exposures, and products liability for equipment.

How Standard Policies Leave You Exposed

Your property value, the number of horses, and the types of activities you conduct all influence both your actual risk and your insurance costs, making a blanket approach to coverage ineffective for equine operations. Standard homeowners and commercial property policies were never designed to handle the liability that arises when someone interacts with a horse on your land. These gaps exist because equine activities introduce variables-animal behavior, rider experience, facility conditions-that traditional underwriting simply doesn’t address. Without equine-specific coverage, you operate with a false sense of security that evaporates the moment a claim lands on your desk.

Equipment and Facility Conditions as Liability Triggers

Under RCW 4.24.540, immunity collapses if the equipment or tack you provide causes injury or if your facility contains a dangerous latent condition you knew about or should have known about without conspicuous warning signs. This isn’t theoretical-your barn’s rotted fencing, a saddle with frayed straps, or a muddy paddock with hidden holes becomes your direct liability if someone is hurt. Poor facility management signals negligence to any injured party’s attorney and undermines your statutory protections.

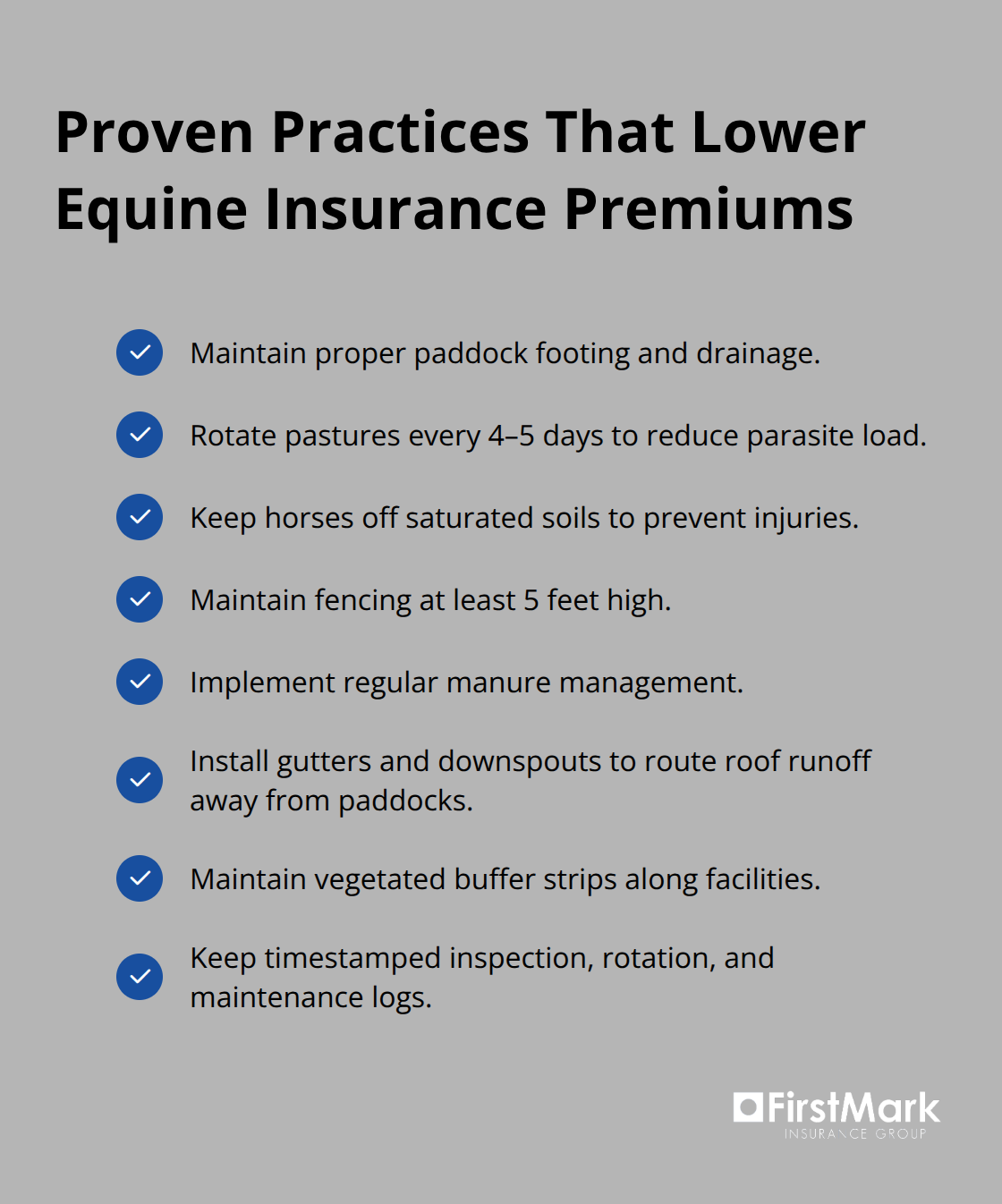

Proper paddock footing with adequate drainage reduces both animal health problems and liability exposure. Fence height should reach at least 5 feet, electric fencing provides a visible psychological barrier, and barbed wire should be eliminated entirely. When you maintain consistent pasture management and keep horses off saturated soils, you create a written record of reasonable care that strengthens your position if a claim arises.

Documentation as Your Defense

Documentation of these practices supports your equine liability insurance application and may qualify you for better rates. Regular manure management and vegetated buffer strips along paddocks demonstrate active risk management. Installing rain gutters and downspouts to direct roof runoff away from barns and paddocks further reduces mud accumulation and the liability exposure it creates. These aren’t optional improvements-they’re the foundation of a defensible safety record that insurance underwriters and courts recognize.

Your facility’s condition and your documented maintenance practices directly determine whether statutory immunity protects you or whether you face full liability exposure. This reality makes the next step-understanding what equine liability coverage actually includes-essential to closing the gaps that standard policies leave wide open.

What Equine Liability Coverage Actually Protects

Bodily Injury and Property Damage Coverage

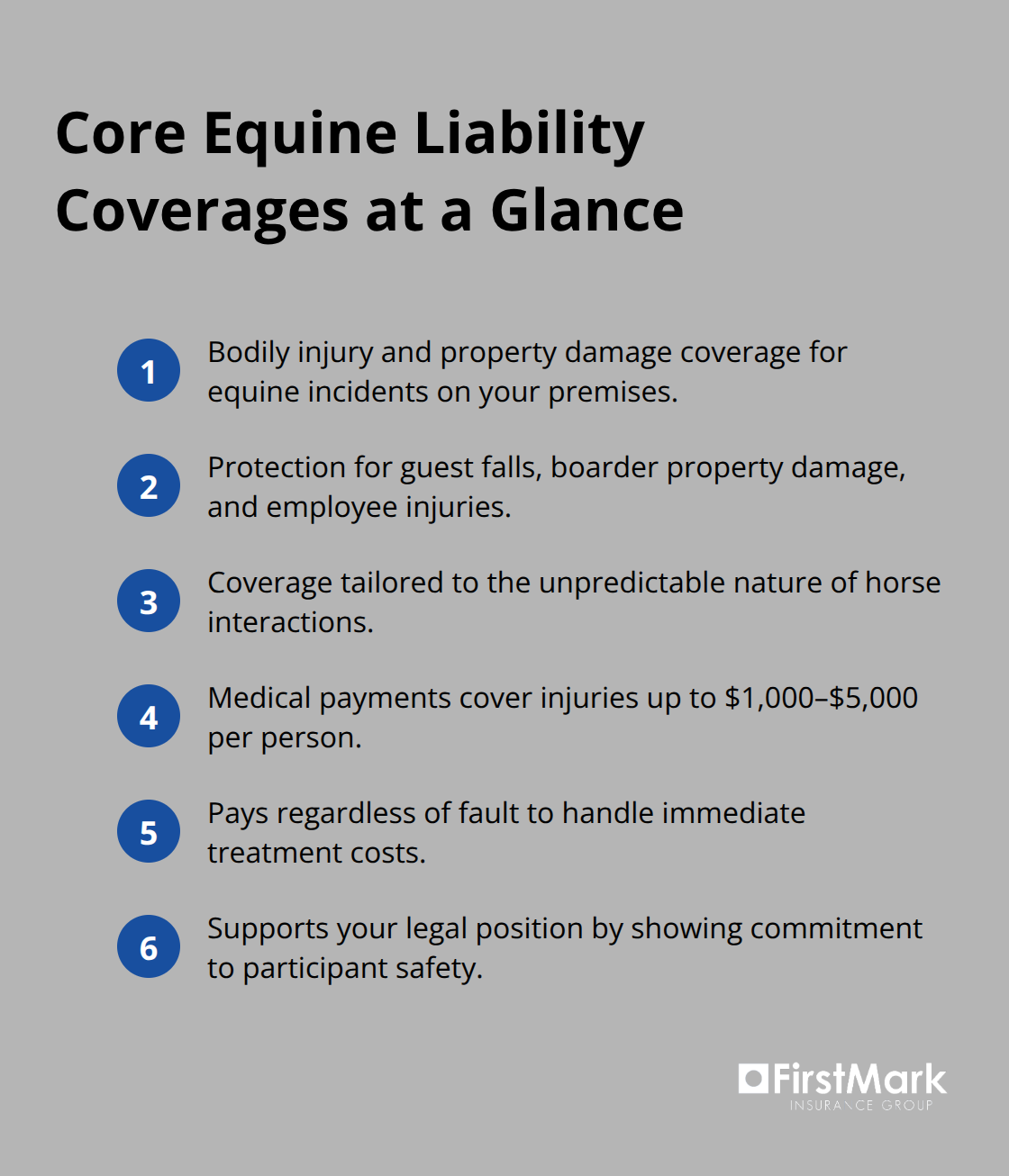

Equine liability insurance fills the exact gaps that standard policies leave open by addressing bodily injury, property damage, and the specialized exposures unique to horse operations. This coverage applies when a guest falls from a horse during a trail ride, when a boarder’s horse damages property in your facility, or when an employee sustains an injury while handling animals on your premises. The protection extends beyond simple slip-and-fall incidents to cover the unpredictable nature of equine interactions. Medical payments coverage operates separately and pays directly for guest and employee injuries up to your chosen limits, typically ranging from $1,000 to $5,000 per person, without requiring proof of fault. This matters because it covers immediate treatment costs and demonstrates your commitment to participant safety, which strengthens your legal position if a more serious claim emerges later.

Care and Custody Liability for Boarding Operations

Care, Custody or Control insurance is an essential coverage for all horse operations which involve non-owned horses, including boarding, breeding and training. A boarding facility housing 15 to 20 horses faces continuous exposure from multiple owners’ animals, boarder activities, and staff interactions that a private farm operation never encounters. This coverage layer ensures you’re protected when someone else’s horse causes damage or injury while in your care.

Specialized Endorsements for Different Operations

Riding schools require specialized endorsements because their liability exposure differs fundamentally from private farm operations. Instruction liability means you’re responsible for assessing each rider’s ability before they mount, documenting that assessment, and maintaining equipment in safe condition. Equipment coverage within your policy protects saddles, bridles, tack, and facility improvements like arena footing and jump standards, which can easily represent $25,000 to $75,000 in property value.

Products Liability and Event Coverage

Products liability endorsements become essential if you sell feed, supplements, or boarding services, covering claims that arise from those products. Competitive event coverage extends protection when horses travel to shows or events off your property, addressing the additional liability that accompanies transportation and unfamiliar environments. These specialized protections address the specific revenue streams and activities that distinguish your operation from others.

Matching Coverage to Your Operation

The right combination of endorsements depends entirely on what your farm actually does. A private breeding operation needs different protection than a boarding facility that also offers riding instruction and sells supplements. Your property value, the number of horses you maintain, and the types of activities you conduct all influence which endorsements make sense for your situation. Understanding these distinctions allows you to close coverage gaps without overpaying for protection you don’t need-and that precision matters when you’re evaluating your actual risk exposure against the costs of your insurance program.

What Drives Your Equine Insurance Premiums

Property Value and Herd Size Set Your Baseline

Property value and the number of horses you keep form the foundation of your premium calculation, but they represent only the starting point. A farm with 5 horses and $200,000 in facility improvements faces fundamentally different exposure than a 25-horse boarding operation with $800,000 in barns, arenas, and equipment. Underwriters examine your total insurable value across structures, pastures, equipment, and livestock to establish appropriate liability limits. If you operate a breeding facility with high-value bloodlines, your premium reflects that concentration of asset risk.

Activity Type Matters More Than Horse Count

The type of equine activities you conduct matters far more than the raw number of horses. A private farm where family members ride recreationally carries minimal liability exposure compared to a boarding facility accepting 15 boarders, each bringing their own animals and liability expectations onto your property. Riding instruction introduces additional exposure because you must assess each participant’s ability before they mount and maintain your equipment to safe standards. Competitive events, breeding operations, and travel to shows all expand your risk profile and adjust your costs accordingly.

Safety Practices and Documentation Lower Your Costs

Your documented safety practices and risk management measures directly influence what you pay. A farm that maintains proper paddock footing, rotates pastures to reduce parasite load, keeps horses off saturated soils, and maintains fencing at 5 feet high demonstrates active hazard reduction. These practices aren’t cosmetic-underwriters recognize them as measurable controls that reduce claim frequency. Farms that implement regular manure management, install gutters to direct roof runoff away from paddocks, and maintain vegetated buffer strips along facilities signal competence to insurers and often qualify for meaningful premium credits.

Documentation matters tremendously here. When you can show timestamped records of facility inspections, pasture rotation schedules, and maintenance logs, you prove that your operation operates preventatively rather than reactively. A facility with poor drainage, visible mud accumulation, and deteriorating fencing will pay substantially higher premiums because those conditions increase injury risk and suggest inadequate management.

Location, History, and Access Shape Your Rate

Location within Washington influences cost significantly. Western counties with heavy rainfall and flood exposure face different hazards than eastern regions contending with drought and wildfire smoke. Your proximity to adequate veterinary care and your history of claims factor into the equation as well. A farm with no prior incidents and strong relationships with local emergency services presents lower risk than one with a pattern of incidents or remote access challenges.

Equipment Value and Specialized Endorsements

Equipment value deserves specific attention because saddles, bridles, specialized tack, and arena footing can easily exceed $50,000 in total value. Endorsements covering equipment breakdowns, products liability for feed or supplements you sell, and care and custody coverage for non-owned horses all add to your premium but address specific exposures your operation creates. The key is matching coverage precision to your actual operations rather than accepting generic protection that either leaves gaps or pays for unnecessary coverage. A boarding facility with 20 horses, a riding school component, and $75,000 in equipment needs a fundamentally different policy structure than a private breeding operation with 8 horses and minimal public interaction.

Final Thoughts

Equine liability insurance WA protects your operation when statutory immunity fails and standard policies leave you exposed. RCW 4.24.540 provides protection only if you maintain equipment properly, assess participant ability before activities begin, and post warnings about known facility dangers-but that statute offers no shield when you fail these obligations. Your equine liability coverage fills the gaps that standard homeowners and commercial policies ignore entirely, addressing guest injuries, equipment failures, and the unpredictable nature of animal behavior that property policies explicitly exclude.

Evaluate your current protection by honestly assessing what your operation actually does. A private farm with family members riding recreationally requires fundamentally different coverage than a boarding facility accepting multiple boarders or a riding school conducting instruction, and your property value, horse count, and revenue streams all shape what you truly need. Check whether your existing policy explicitly addresses equine liability, care and custody coverage for non-owned horses, and equipment protection-most standard policies exclude these exposures entirely, leaving you with false confidence that collapses when a claim arrives.

Combine insurance with documented safety practices to build genuine risk management. Maintain proper paddock footing and drainage, rotate pastures every 4 to 5 days, install gutters to direct roof runoff away from facilities, and implement regular manure management-these practices reduce actual injury risk and demonstrate competence to underwriters, often qualifying you for meaningful premium credits. We at FirstMark Insurance Group work with top carriers to present equine liability coverage options that match your specific operation and budget, helping you identify the exact endorsements and limits your farm needs rather than accepting generic protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation