Most people don’t realize they’re leaving hundreds of dollars on the table every year. Insurance bundle discounts can cut your premiums significantly, but only if you know how to use them properly.

At FirstMark Insurance Group, we’ve seen customers save 15–25% by bundling policies strategically. This guide shows you exactly how to maximize those savings and avoid the mistakes that cost money.

What Bundle Discounts Actually Save You

A bundle discount combines two or more insurance policies with a single insurer to qualify for a reduced rate on your premiums. Insurers reward customer loyalty when you consolidate coverage, offering multi-policy discounts across your entire package rather than just one policy. Auto and home insurance represent the most common bundle, but you can also combine auto with renters, condo, motorcycle, boat, or RV policies depending on your insurer. The discount applies to your entire bundled package, which means savings compound across multiple coverage types.

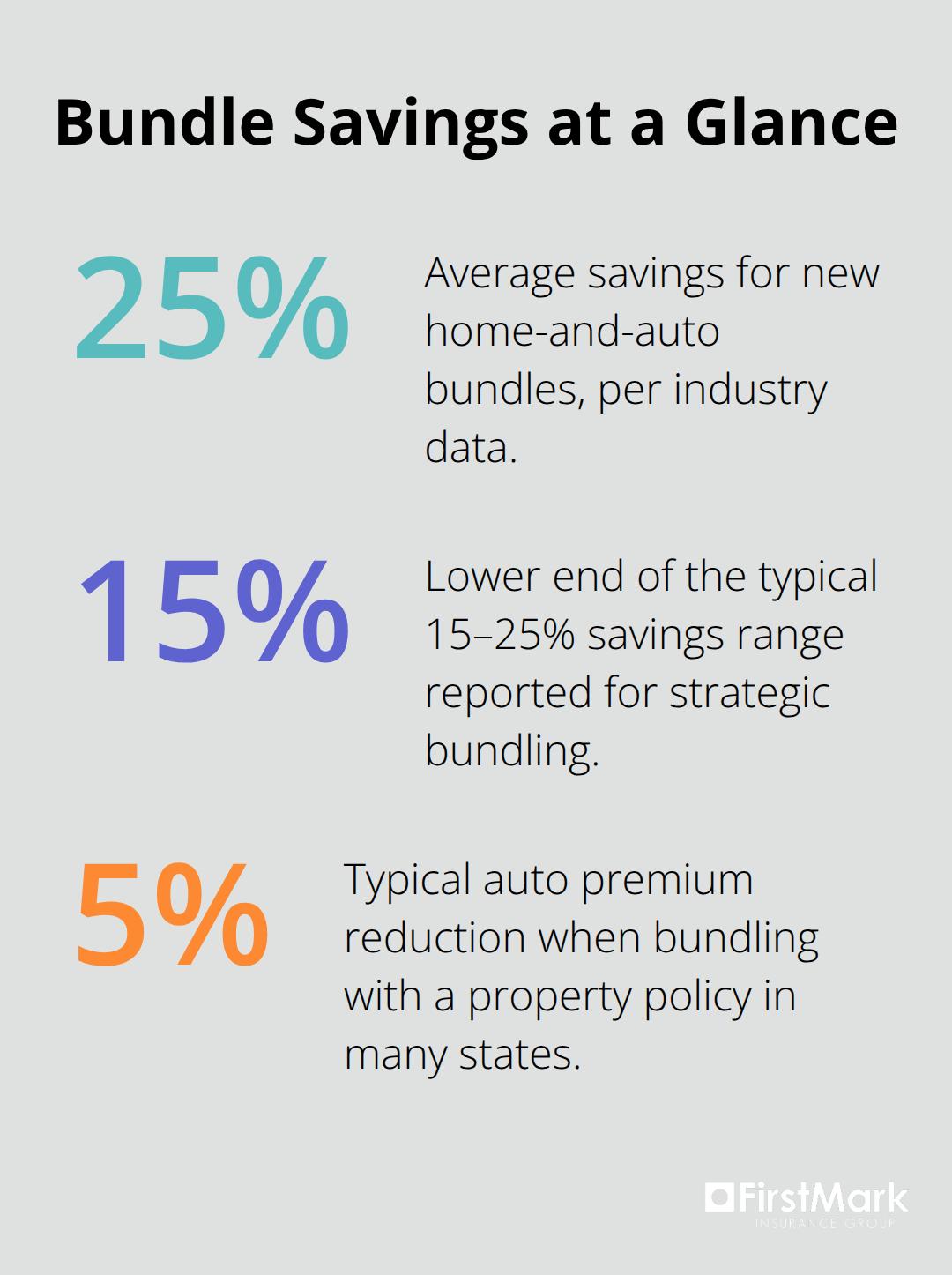

New customers bundling home and auto save nearly 25% on average, according to industry data. Some insurers like Liberty Mutual report customers save around $950 per year when bundling auto and home. Progressive shows new customers can save more than 20% when combining policies. These aren’t theoretical numbers-they reflect what real customers actually pay when they consolidate coverage rather than shopping policies separately.

How much you’ll actually save depends on your situation

The discount percentage varies significantly by insurer and your location. Bundling auto with property policies typically saves about 5% on auto in most states, but total household savings can reach 15–30% when you factor in discounts across all bundled policies. A single deductible for losses affecting both auto and home policies with some carriers like Progressive further reduces your out-of-pocket costs during claims.

What matters most is that you compare bundle quotes across at least three providers before making a decision. One insurer’s bundle might save you $800 annually while another saves only $400-the difference matters. Timing also affects your savings: you can bundle anytime without waiting for policy renewal dates, so the sooner you consolidate coverage, the sooner savings begin.

When to bundle for maximum impact

If you’re purchasing a new car, home, or motorcycle, you should bundle that new policy with existing coverage to make the transition cost-effective from day one. This approach locks in savings immediately rather than waiting months to add coverage later. Life changes create natural opportunities to reassess your insurance needs and consolidate policies with one carrier.

The next section explores specific strategies that help you identify which insurers offer the strongest bundling deals for your situation and location.

How to Lock In Maximum Savings Across All Your Policies

Audit Your Current Coverage and Consolidate

Consolidating multiple policies with one insurer sounds straightforward, but most people miss critical opportunities to amplify their savings. The reality is that bundling delivers its full potential only when you actively manage which policies go where and how you layer additional discounts on top. Start by auditing your current coverage across all carriers. Many customers maintain auto insurance with one company, home insurance with another, and renters or condo coverage elsewhere simply because they never questioned the arrangement. This fragmentation costs real money.

When you move all eligible policies to a single carrier, you qualify for the multi-policy discount immediately. The timing matters less than the action itself-you can bundle auto now and add home coverage later while still qualifying for the discount, as long as you maintain both policies with the same insurer. However, if you cancel one bundled policy, you typically lose the multi-policy discount across your entire account, so plan any coverage changes carefully before pulling the trigger.

Stack Additional Discounts on Top of Your Bundle

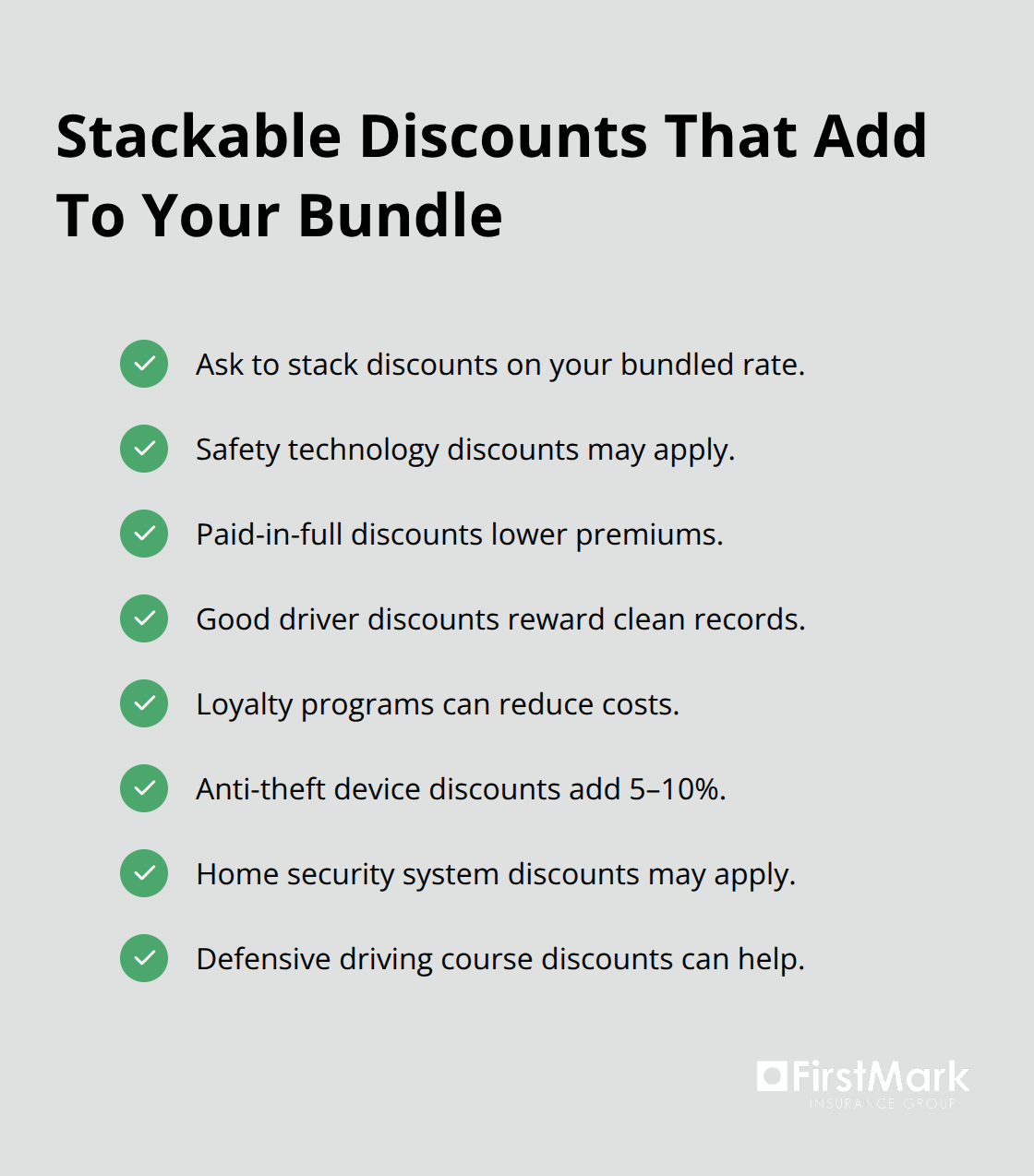

Beyond the base bundle discount, additional savings often exceed the headline number. Ask your insurer about stacking discounts on top of your bundled rate. Safety technology discounts, paid-in-full discounts, good driver discounts, and loyalty programs all compound with your bundle savings.

An insurer might offer a discount for bundling, then another 5–10% for installing anti-theft devices or maintaining a clean driving record. These secondary discounts vary significantly by carrier and location, which is why annual policy reviews matter.

Review Your Renewal Rate Against Competitor Quotes

At renewal time, contact your insurer and explicitly ask what new discounts you’ve become eligible for since your last renewal. Life changes-installing a security system, completing a defensive driving course, or reaching a milestone without claims-create new discount opportunities. Additionally, comparing your renewal rate against quotes from competitors prevents you from paying inflated rates simply because you’ve stayed loyal. Some carriers reward loyalty; others increase rates on long-term customers hoping they won’t shop around.

The only way to know is to get fresh quotes annually and hold your current insurer accountable. If a competitor offers better pricing on your bundled policies, leverage that quote to negotiate with your current carrier or make the switch. Insurance companies understand that bundled customers are more profitable long-term, so they often match competitive offers to keep you. This competitive pressure works in your favor-use it to your advantage.

Understand When Bundling Decisions Impact Your Discount

One critical mistake customers make involves canceling a bundled policy without understanding the consequences. When you remove one policy from your bundle, your multi-policy discount disappears across all remaining policies. This means dropping your motorcycle coverage to save money on that single policy could actually cost you more overall when your auto and home discounts vanish. Before you cancel anything, request a new quote from your insurer showing what your rates would be without that policy. Compare that quote against keeping the policy bundled. The math often reveals that maintaining the bundle saves more money than canceling coverage.

The next section examines the most common mistakes that prevent customers from capturing their full bundle savings potential.

Where Bundling Goes Wrong

Comparing Only One Quote Costs You Hundreds

Most customers who fail to capture maximum bundle savings make one critical mistake: they accept a single quote without comparing that bundle deal against competitors. You might receive a quote showing 20% savings with Carrier A, feel satisfied, and sign up without checking what Carrier B or Carrier C actually offer for your specific situation. The problem is that bundle discounts vary dramatically by insurer and your location. Progressive might save you $400 annually on a home-and-auto bundle in your state while Liberty Mutual saves $950 on identical coverage. That $550 difference vanishes if you skip the comparison step.

The only way to identify which carrier actually delivers the best bundle deal for your situation is to obtain quotes from at least three providers and compare them side by side using identical deductibles and liability limits. This takes 30 minutes and costs nothing, yet most people skip this step entirely.

Ignoring Renewal Opportunities Locks You Into Higher Rates

The second mistake involves treating your bundled policies as a set-it-and-forget-it arrangement after you sign up. When your policy renews, your insurer sends a notice with your new premium, and most people simply pay it without questioning whether rates increased. What you should actually do is request a fresh quote from competitors at your renewal date and specifically ask your current insurer what new discounts you’ve become eligible for since your last renewal.

Life changes create new discount opportunities: you might have installed a security system, completed a defensive driving course, or gone years without claims (all of which trigger additional discounts beyond your base bundle). Some insurers reward loyalty with rate reductions; others increase rates on long-term customers banking on inertia. You won’t know which applies to you without making the call. Additionally, bundling discounts can erode over time as renewal surcharges accumulate, so comparing competitor quotes annually prevents you from overpaying simply because you bundled years ago.

Using Competitive Quotes to Negotiate Better Rates

If a competitor offers better pricing, use that quote to negotiate with your current carrier or switch. Carriers understand bundled customers generate higher lifetime value, so they frequently match competitive offers to retain you rather than lose your entire account. This competitive pressure works in your favor-leverage it to your advantage.

Final Thoughts

Bundle discounts work only when you actively manage them. The customers who capture the full 15–25% savings mentioned earlier share one trait: they compare quotes across multiple carriers, review their policies annually, and stack additional discounts on top of their base bundle. You now understand how insurance bundle discounts function, which mistakes drain your savings, and exactly what actions produce real results.

Gather your current policy documents and contact at least three insurers for bundled quotes using identical coverage limits and deductibles. This comparison takes roughly 30 minutes and reveals whether you’re overpaying on your current arrangement. At your next renewal date, request fresh quotes from competitors and ask your current insurer what new discounts you’ve qualified for since your last policy period.

An independent agent simplifies this process considerably by comparing bundle options across multiple carriers simultaneously, identifying which discounts apply to your specific situation, and handling the administrative work of consolidating your policies. FirstMark Insurance Group has spent 30 years helping families and businesses navigate insurance complexities and find coverage that actually fits their needs at the best available pricing. We review your policies throughout the year to confirm your coverage aligns with your current situation and that you’re capturing every available discount, transforming insurance from a frustrating expense into a straightforward protection strategy that saves you money year after year.