Seasonal home insurance protects vacation properties, cabins, and second homes that sit empty for months at a time. These properties face unique risks that standard homeowners policies don’t adequately cover.

We at FirstMark Insurance Group see many property owners surprised by coverage gaps when filing claims. Understanding these differences can save you thousands in unexpected repair costs.

Understanding Seasonal Home Insurance Coverage

What Counts as a Seasonal Home

Seasonal homes include vacation properties occupied fewer than six months annually, hunting cabins, beach houses, lake cottages, and ski chalets. The Insurance Information Institute defines these as secondary residences where you don’t maintain year-round occupancy. Properties rented occasionally through platforms like Airbnb also fall into this category, though they require additional rental coverage beyond standard seasonal policies.

Why Standard Home Insurance Falls Short

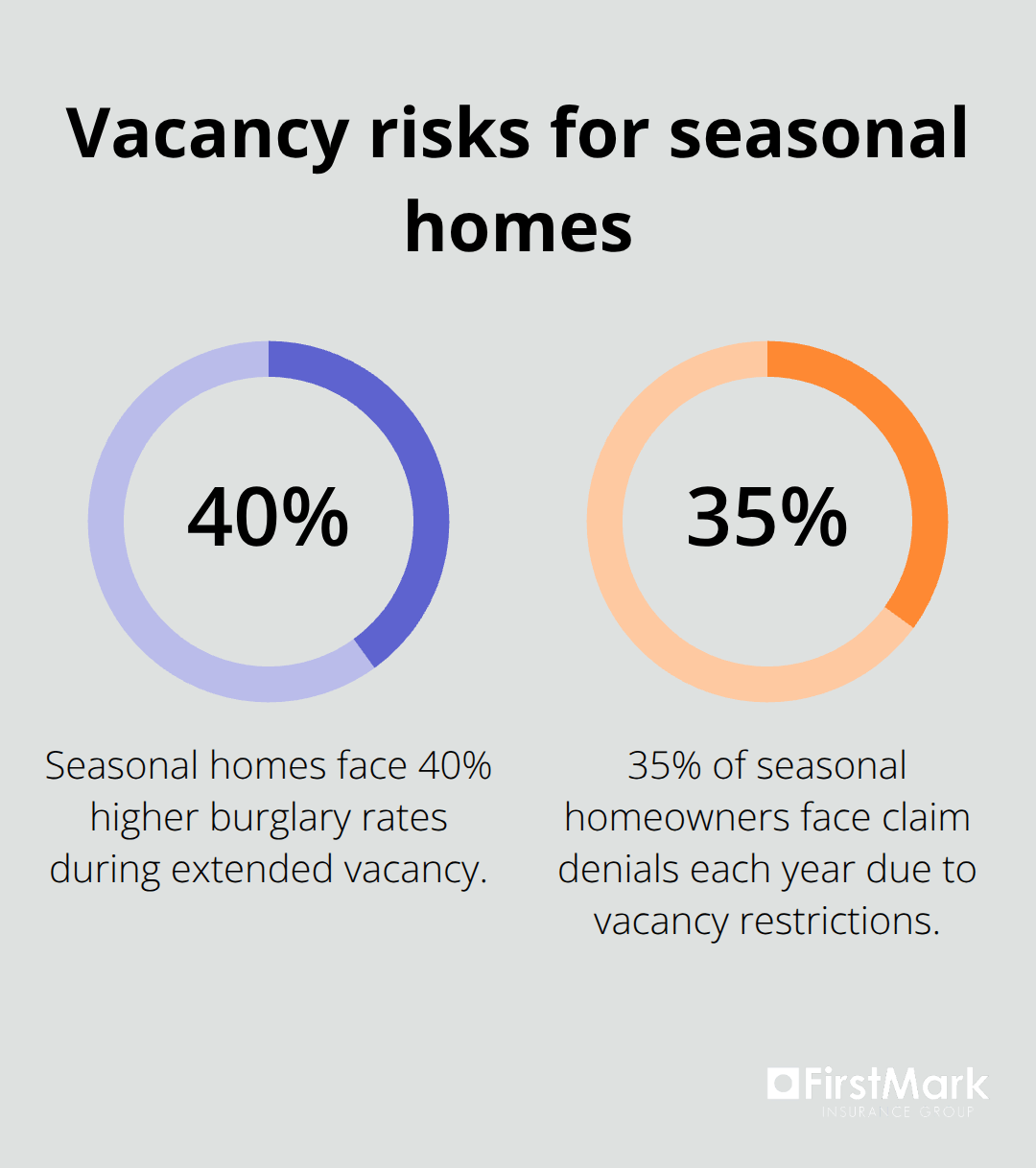

Your primary home insurance excludes coverage for properties left vacant more than 60 consecutive days. Most standard policies contain vacancy clauses that void protection after this period, which leaves you exposed to theft, vandalism, and weather damage. Seasonal homes face 40% higher burglary rates according to FBI crime statistics, yet standard policies won’t cover these losses during extended vacancy periods.

The Coverage Gaps That Cost Thousands

Water damage from frozen pipes represents a significant seasonal home concern, with repair costs ranging from $150 to $5,000 depending on severity. Standard policies often exclude damage from gradual leaks or maintenance issues that develop during vacancy. Mold coverage gets limited or excluded entirely when properties remain unmonitored for months. Liability protection drops significantly for unoccupied properties, which leaves you vulnerable if someone gets injured on your vacant property.

Vacancy Clauses Create Major Risks

Standard homeowners policies typically void coverage after 30-60 days of vacancy. This creates a dangerous gap for seasonal properties that sit empty for months. Insurance companies view vacant homes as high-risk investments due to increased theft potential and delayed damage detection. The National Association of Insurance Commissioners reports that 35% of seasonal homeowners face claim denials each year due to these vacancy restrictions.

These fundamental differences between seasonal and primary home insurance highlight why specialized coverage becomes necessary for your vacation property investment. Consider adjusting coverage based on seasonal usage patterns for recreational vehicles and watercraft to maximize your protection while managing costs effectively.

Essential Protection for Seasonal Properties

Minimum Occupancy Standards Matter Most

Insurance companies require seasonal homes to be occupied at least 30 days annually to maintain standard coverage. Most homeowners insurance policies include a vacancy clause, which limits or excludes coverage if the property is unoccupied for typically 30 to 60 consecutive days. Schedule quarterly visits of at least one week each to meet occupancy requirements and conduct property inspections.

Weather Damage Requires Active Prevention

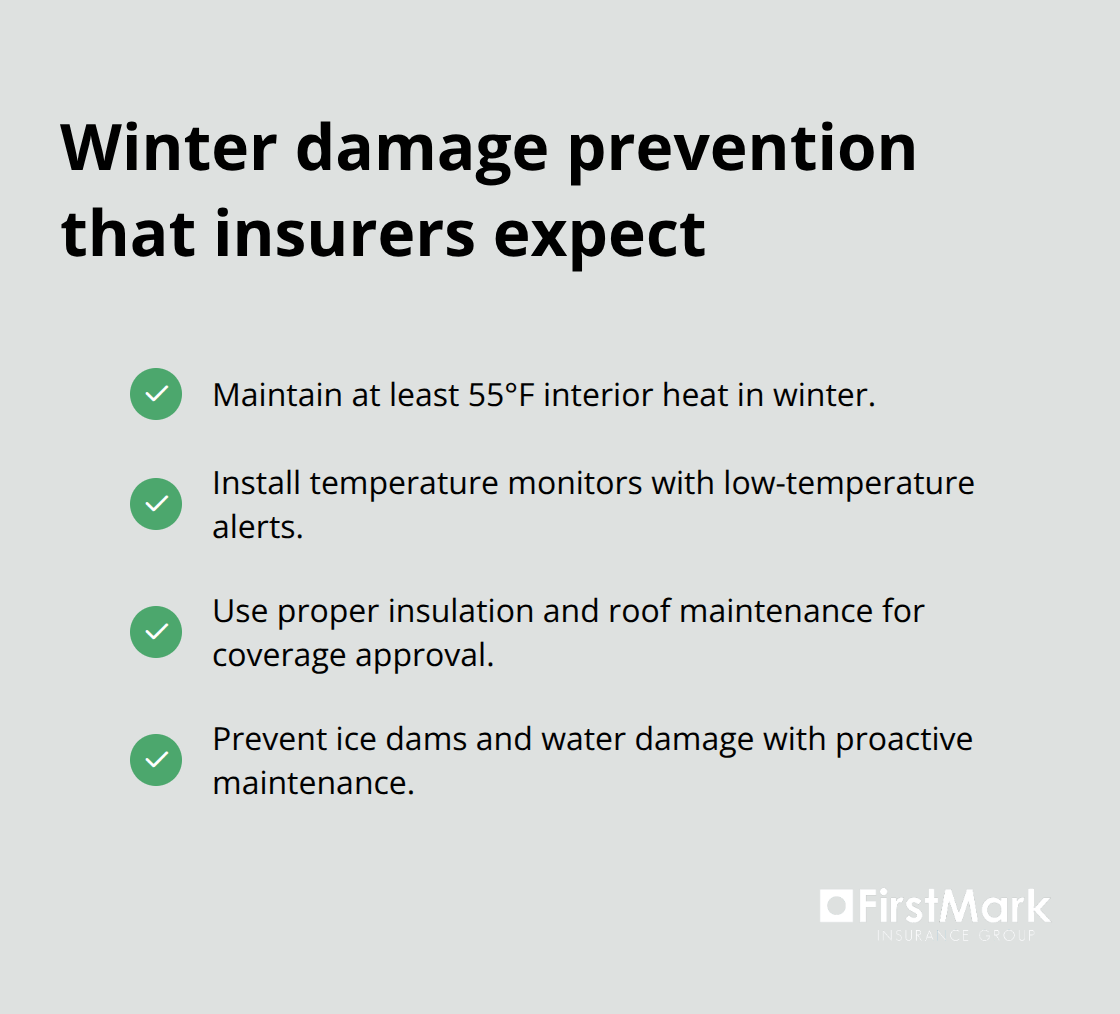

Frozen pipe damage costs seasonal homeowners an average of $18,000 per incident according to the American Insurance Association. Properties must maintain minimum 55-degree heat during winter months to prevent pipe bursts. Temperature monitors that send alerts when interior temperatures drop below safe levels protect your investment. Water damage from ice dams affects 23% of seasonal properties in snow-prone regions (proper insulation and roof maintenance become non-negotiable for coverage approval).

Security Systems Reduce Premiums by 20 Percent

Professionally monitored alarm systems cut seasonal home insurance costs by 15-20% while they provide protection against the 40% higher burglary rates these properties face. Motion-activated cameras with smartphone alerts help detect break-ins within minutes rather than months. The FBI reports that 67% of seasonal home burglaries occur during extended vacancy periods when neighbors aren’t present to watch the property. Smart locks that track entry attempts and provide access logs for property managers or caretakers who check on your home monthly add another layer of protection.

Water Shut-Off Prevents Catastrophic Damage

Turn off the main water supply and drain all pipes before extended absences to prevent freeze damage. Burst pipes in vacant homes often go undetected for weeks, which leads to extensive water damage and mold growth. Professional winterization services cost $200-400 but prevent thousands in repair costs. Hot water heaters should be set to vacation mode or turned off completely during extended absences to reduce energy costs and fire risks.

These protection strategies directly impact your insurance costs and coverage options, which makes understanding the financial implications of seasonal home ownership your next priority. Regular seasonal maintenance helps ensure your property remains protected year-round.

Cost Factors and Money-Saving Strategies

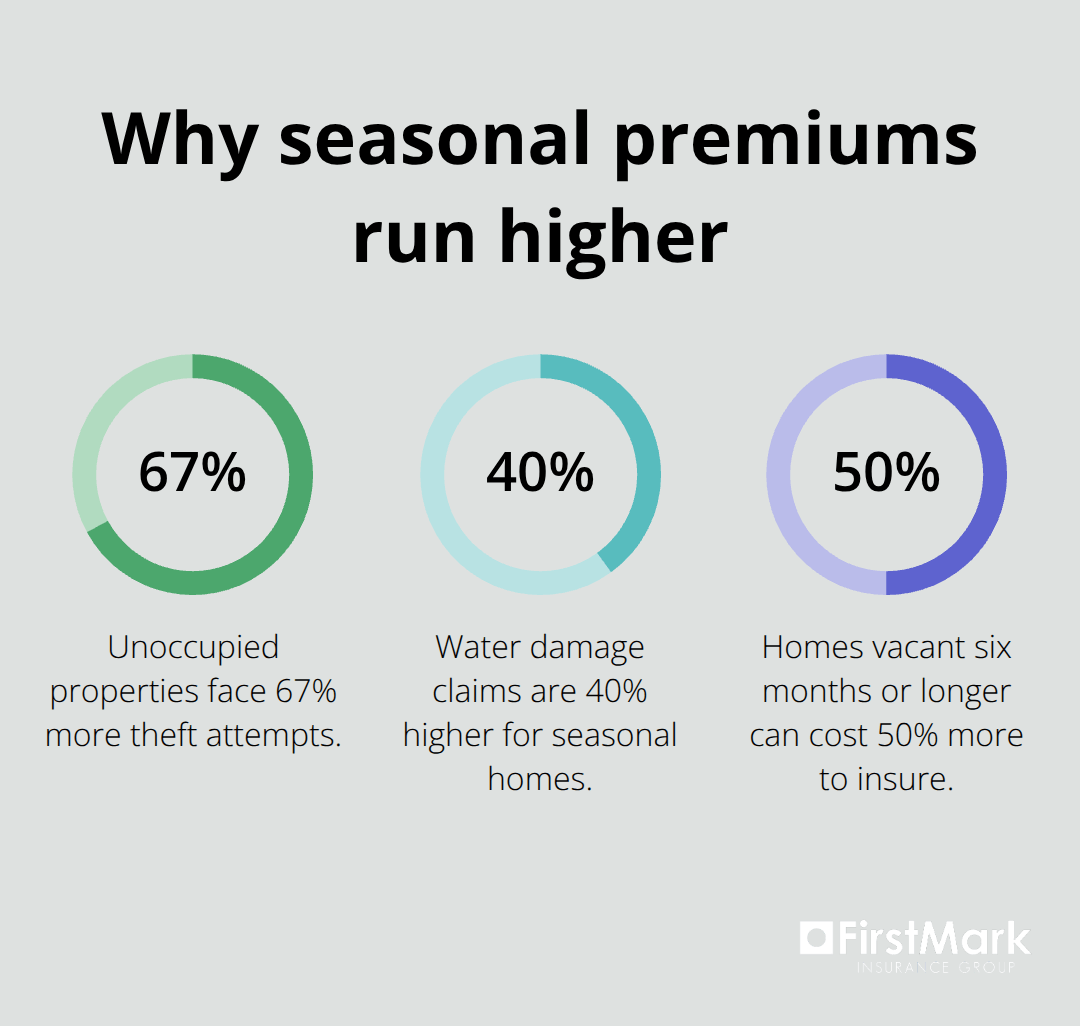

Seasonal home insurance premiums run 15-25% higher than primary residence policies due to increased vacancy risks and delayed damage detection. The Insurance Information Institute reports that unoccupied properties face 67% more theft attempts and 40% higher water damage claims, which drives these premium increases. Properties vacant more than four months annually typically see the highest rate adjustments, with some insurers charging 50% more for homes empty six months or longer.

Security Systems Deliver Immediate Premium Relief

Professional monitoring systems can provide average savings of $59 per year, making them cost-effective investments. Central station alarm systems that notify authorities within minutes of breach detection qualify for the highest discounts. Smart home technology including water leak detectors, temperature monitors, and security cameras can lower rates an additional 5-10% when professionally installed. The National Association of Insurance Commissioners found that homes with comprehensive security systems file 60% fewer theft claims and 35% fewer water damage claims during vacancy periods.

Multi-Policy Discounts Beat Individual Shopping

Combining seasonal home coverage with your primary residence policy saves 10-25% compared to separate insurers. Most major carriers offer multi-property discounts that increase with additional policies, reaching maximum savings at three or more properties (auto insurance bundling adds another 5-15% discount on total premiums). Claims-free discounts accumulate faster across bundled policies, with some insurers offering 25% reductions after five years without claims.

Location and Property Features Drive Base Rates

Coastal properties face hurricane and flood risks that increase premiums by 30-50% over inland locations. Properties in wildfire-prone areas see similar rate increases due to elevated risk assessments. Age of construction affects rates significantly, with homes built before 1980 facing 20-40% higher premiums due to outdated electrical and plumbing systems. Pool and hot tub amenities add liability exposure that increases coverage costs by 10-15% annually. Umbrella insurance provides additional liability protection for properties with elevated risk features.

Final Thoughts

Seasonal home insurance protects your vacation property investment from risks that standard homeowners policies won’t cover. The 15-25% premium increase over primary residence coverage pays for protection against 67% higher theft rates and extended vacancy exposures. Properties left unoccupied face significant risks that require specialized coverage to avoid costly claim denials.

Schedule quarterly property visits to meet occupancy requirements and install professionally monitored security systems for immediate 15-20% premium savings. Bundle your seasonal coverage with existing policies to maximize discounts while you maintain comprehensive protection. Water damage prevention through proper winterization and temperature monitoring prevents the $18,000 average repair costs from frozen pipes (smart security technology and regular maintenance visits reduce claim frequency and keep premiums manageable over time).

We at FirstMark Insurance Group help families navigate insurance complexities with personalized service. Our team explores offerings from top providers to find coverage that fits your specific seasonal property needs at competitive rates. Contact FirstMark Insurance Group today to protect your seasonal home investment with the right coverage before your next vacancy period begins.