A single misstep in client advice can expose your consulting practice to significant financial and reputational damage. Professional liability for consultants isn’t optional-it’s a fundamental safeguard that separates thriving practices from those facing devastating claims.

At FirstMark Insurance Group, we’ve seen how the right coverage transforms uncertainty into confidence. This guide walks you through the protection your practice actually needs.

What Professional Liability Actually Covers

How Professional Liability Protects Your Practice

Professional liability insurance for consultants protects your practice when clients claim you made mistakes, gave bad advice, missed deadlines, or failed to deliver on agreed services. The policy covers your legal defense costs, settlements, and judgments arising from these allegations, whether or not you were actually at fault. A client can sue claiming financial harm from your work, and your professional liability policy steps in to handle the defense and associated expenses. The coverage applies across most consulting disciplines-management consultants advising on business strategy, IT consultants recommending technology solutions, marketing consultants designing campaigns, HR consultants handling employee policies, and financial advisors providing investment guidance all face similar exposure.

The Real Cost of Claims Without Coverage

Without this coverage, you personally absorb attorney fees, court costs, and any damages awarded-expenses that can easily exceed $100,000 even for a case that doesn’t go to trial. A management consultant who recommends a failed business strategy that costs a client $500,000 in losses faces a lawsuit for that full amount. A marketing consultant whose campaign recommendations underperform gets sued for wasted advertising spend and lost revenue. An HR consultant who makes administrative errors (filing incorrect tax forms, mishandling employee data, or creating compliance violations) exposes clients to fines and back taxes, and those clients will pursue the consultant for reimbursement. Technology consultants face claims when their recommendations lead to service interruptions or data loss.

Understanding Claims-Made vs. Occurrence Policies

Claims-made policies cover incidents that occur and are reported during the policy period, while occurrence policies cover incidents that happen during the policy period regardless of when they’re reported. Most consultants work with claims-made policies because they’re more affordable, but you’ll need tail coverage if you ever stop practicing to protect yourself against claims filed after you’ve retired or changed careers.

The Scale of Litigation Risk in Consulting

The Duane Morris Class Action Review for 2025 documented over $40 billion in class action settlements in 2024 alone, with many of these cases involving consultant recommendations on product disclosures, environmental claims, privacy practices, and corporate policies. When clients suffer losses tied to your advice, they don’t simply fire you-they sue to recover damages. Your professional liability policy covers defense costs from day one, with the average malpractice lawsuit incurring $30,000 in defense costs, while some cases can reach upwards of $100,000.

Selecting Coverage Limits and Deductibles

Coverage limits matter directly to your protection; a $1 million limit protects you against smaller claims, while a $2 million limit or higher protects your practice if a client’s losses are substantial. The deductible you choose affects your premium-a $5,000 deductible costs less than a $2,500 deductible-so you’ll balance affordability with the amount you can reasonably cover out of pocket if a claim emerges. Understanding these policy mechanics positions you to evaluate which coverage structure aligns with your practice’s size, client base, and risk profile.

Choosing the Right Policy Structure for Your Consulting Practice

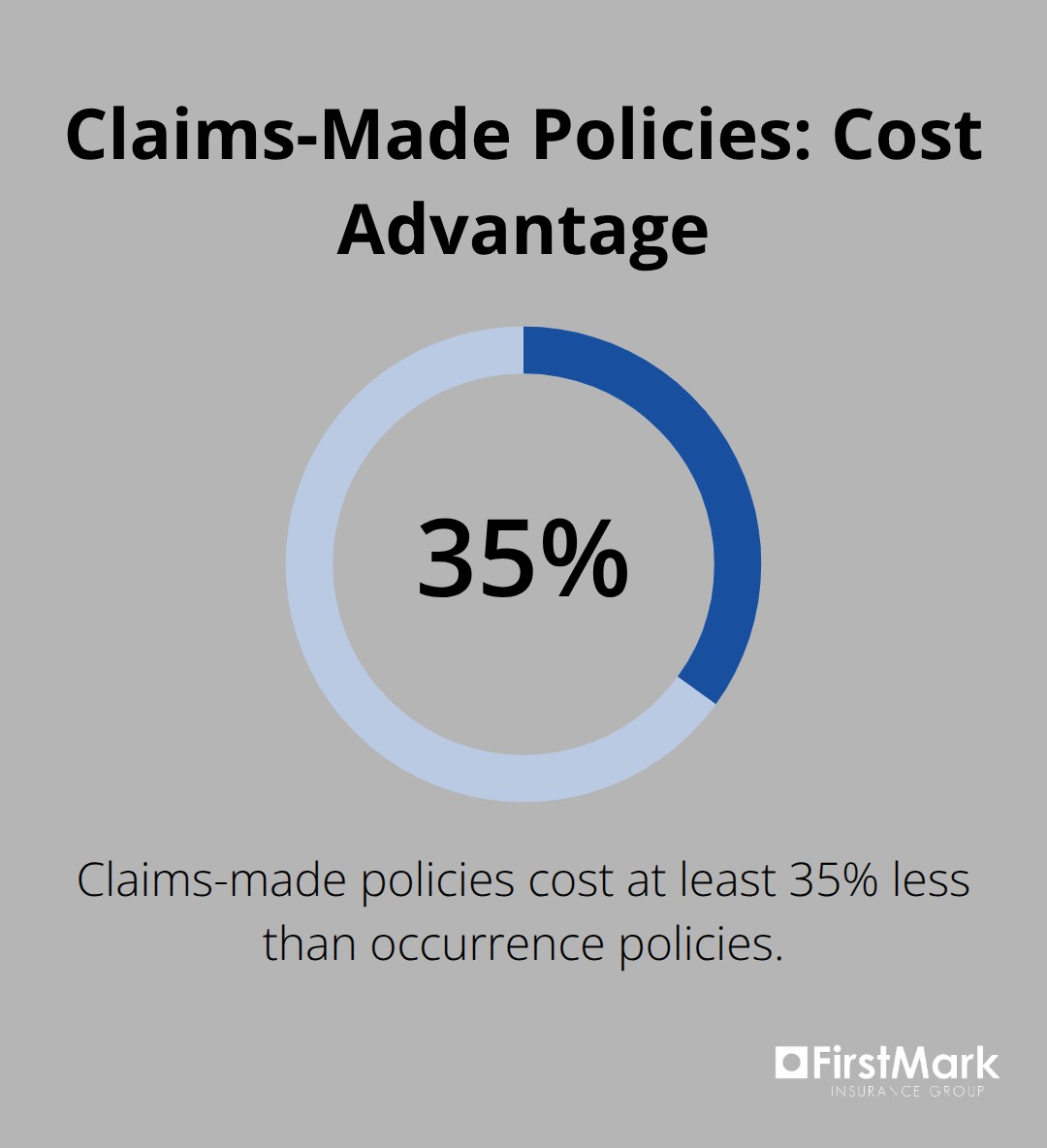

Claims-Made Policies: The Cost-Effective Standard

Claims-made policies dominate the consulting insurance market because they cost at least 35% less than occurrence policies, making them the practical choice for most consultants. A claims-made policy covers incidents that both occur and are reported during your active policy period, which means you need continuous coverage throughout your career. The trade-off is straightforward: you save money upfront, but you must maintain coverage even after you stop taking clients or retire. This is where tail coverage becomes essential.

Tail Coverage: Protecting Your Exit Strategy

Tail coverage, also called run-off coverage, extends your protection for claims filed after your policy ends, typically covering a period of one to three years. Without tail coverage, a client could file a claim years later for work you completed decades ago, and you would have no protection. If you ever plan to exit consulting, factor tail coverage costs into your exit strategy. Occurrence policies eliminate this concern by covering incidents that happen during the policy period regardless of when claims are filed, but the higher premium costs mean you pay significantly more for peace of mind most consultants don’t need.

Matching Coverage Limits to Your Actual Exposure

Your coverage limits should reflect your actual exposure, not industry minimums. A $1 million limit protects against typical claims, but if you advise clients on decisions involving millions in capital, losses, or regulatory exposure, a $2 million or $3 million limit makes more sense. The Duane Morris Class Action Review documented over $40 billion in class action settlements in 2024, with many involving consultant recommendations on product disclosures, privacy practices, and compliance policies. If your advice influences high-stakes decisions, your coverage should match that reality.

Deductibles and Specialized Coverage Options

Deductibles create a direct trade-off with premiums: a $5,000 deductible costs less than a $2,500 deductible, but you absorb the difference from your own resources if a claim emerges. Try a deductible you can actually afford to pay without disrupting operations. Specialized policies exist for specific consulting disciplines because risk profiles vary dramatically. Technology consultants face different exposures than marketing consultants, and HR consultants navigate compliance risks that management consultants don’t encounter. Tailored policies account for these differences, often providing better coverage at more competitive rates than generic professional liability plans.

The structure you select today determines how well your practice weathers tomorrow’s claims. Your next step involves evaluating which insurance providers offer the flexibility and expertise to build a policy that truly fits your consulting model.

How to Choose the Right Professional Liability Coverage

Map Your Actual Client Exposure

Start with your real client exposure, not industry averages. Document the financial stakes of your recommendations: if you advise on decisions affecting $5 million in client capital, your coverage limits should reflect that exposure rather than settle for a generic $1 million policy. Review your client contracts for liability caps or insurance requirements they impose on you-many enterprise clients demand $2 million minimums or proof of specific coverage types. Pull together your last three years of client engagements and note which industries you serve, what decisions your advice influences, and where disputes most likely emerge. A management consultant recommending organizational restructuring faces different risks than a marketing consultant optimizing campaign spend, yet many consultants purchase identical policies. Your risk profile is unique to your practice model, client mix, and the financial consequences of your work. Once you map this exposure, you can articulate exactly what coverage you need rather than guessing at industry standards.

Evaluate Providers on Three Concrete Factors

Evaluating providers requires moving beyond premium quotes to assess three concrete factors: how quickly they bind coverage, whether legal fees are included in defense costs, and their actual claims-handling speed. Some insurers cover legal defense costs from day one, while others exclude certain defense categories or cap them separately from settlement limits-this distinction matters when you face a $50,000 legal bill before any settlement. Request sample policies and read the exclusions carefully, not just the coverage summary, because exclusions determine what you’re actually protected against. Ask prospective insurers directly: how many days until you can download a Certificate of Insurance, whether you can adjust coverage limits mid-year as your practice evolves, and what their average claims resolution time is in your consulting discipline. Providers serving 1,300-plus professions typically offer more tailored coverage options than generalist carriers, allowing you to select protections specific to your consulting type rather than accepting broad, less relevant coverage. Talk to three providers minimum and compare how they respond to your questions-responsiveness during the quote process predicts responsiveness when you file a claim. Your client contracts often specify which insurers are acceptable, so verify that shortlisted providers meet any contractual requirements before investing time in detailed quotes.

Align Your Policy with Client Contract Requirements

Many enterprise clients require professional liability coverage as a condition of engagement, and some specify minimum limits, required endorsements, or proof of continuous coverage. Review each significant client contract for insurance language before binding your policy, then confirm your selected coverage meets those requirements. If a client demands tail coverage for claims filed after your engagement ends, factor that into your policy structure-some claims-made policies include automatic tail provisions, while others require separate purchase. Document your coverage details in writing and share them with clients proactively rather than waiting for requests, which demonstrates professional risk management and builds confidence in your practice. The cost difference between a policy meeting your actual needs and one that falls short of client requirements can be substantial when a claim emerges and you discover gaps-spending an extra $500 annually on adequate coverage costs far less than defending yourself against an uninsured claim.

Final Thoughts

Professional liability for consultants protects what you’ve built, but only if your coverage actually matches your exposure. Review your policy annually when your client base shifts, your engagement scope expands, or your industry faces new regulatory pressures-a policy adequate for a solo practice serving mid-market clients becomes insufficient when you advise enterprise organizations on decisions affecting millions in capital. Document your three largest client engagements and compare the financial consequences your advice influences against your current coverage limits and deductibles.

Contact your insurance provider about adjusting your policy mid-year if gaps exist rather than waiting for renewal. Verify that your coverage meets any contractual requirements your clients impose, and maintain proof of continuous coverage to satisfy enterprise clients who demand it as a condition of engagement. These steps take minimal time but prevent costly gaps when claims actually emerge.

At FirstMark Insurance Group, we’ve guided businesses through insurance complexities for decades, helping them find coverage that protects their operations rather than simply checking a box. We work with top insurance providers to present you with choices that fit your specific needs at competitive pricing. Your consulting expertise creates value for clients-your insurance should create confidence for you.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation