Running a contracting business in Seattle means managing more than just schedules and crews-it means protecting everything you've built from unexpected losses.

We at FirstMark Insurance Group know that Seattle contractor business insurance isn't one-size-fits-all. The right coverage depends on your specific operations, the risks you face daily, and the local regulations that govern your work.

This guide walks you through what actually matters for your business, where contractors typically fall short, and how to find an insurance partner who understands your industry.

What Seattle Contractors Actually Need

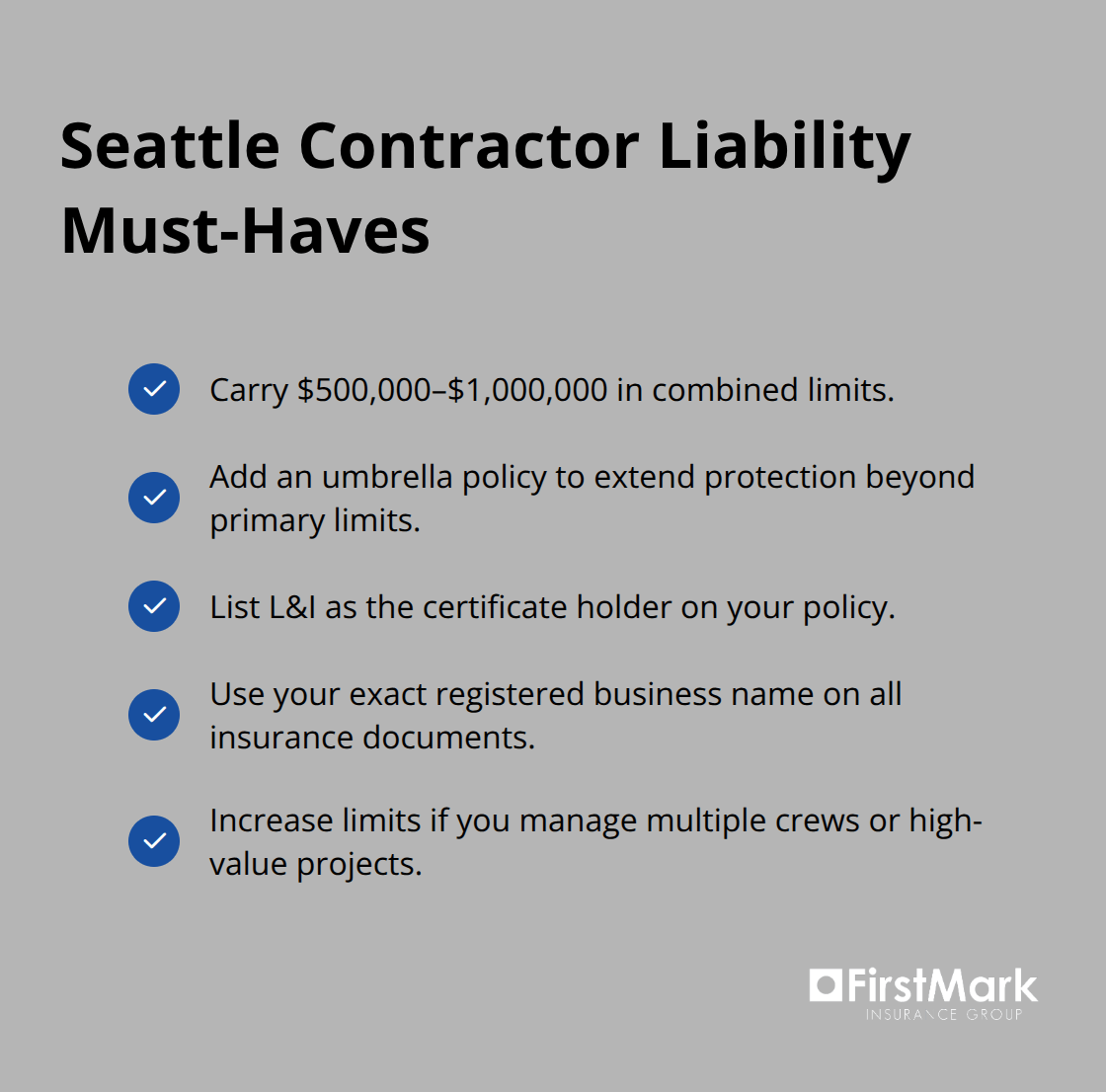

General liability insurance isn't optional for Seattle contractors-it's the foundation that prevents a single accident from destroying your business. Washington State requires minimum coverage of $200,000 in public liability and $50,000 in property damage, or a combined single limit of $250,000, but these numbers barely scratch the surface of real-world exposure. A slip-and-fall on your job site, a dropped tool hitting a neighboring property, or damage to a client's existing structure can easily exceed $250,000 in claims. Most Seattle contractors should carry at least $500,000 to $1,000,000 in combined limits, especially if you manage multiple crews or work on high-value projects. Adding an umbrella policy extends protection beyond your primary limits at a reasonable cost and signals to clients and lenders that you take risk seriously. Your policy must list L&I as the certificate holder and use your exact registered business name-any mismatch delays projects and creates compliance headaches.

Workers' Compensation and Employer Liability

Washington operates a monopolistic state fund for workers' compensation, meaning if you have employees, you must carry coverage through the state fund with no option to use private insurers. The National Safety Council reported that the average workplace injury claim in 2022 cost about $40,000, yet many contractors underestimate their actual exposure when calculating payroll and estimating project costs. One critical gap exists: the state fund does not include employer's liability coverage, which protects you if an employee sues for negligence or unsafe working conditions. Most contractors add employer's liability coverage through private insurers or endorsements to fill this gap and avoid six-figure legal costs. Verify that any subcontractors you hire carry current workers' compensation coverage before they step on your site-you remain responsible for their safety obligations, and a lapse in their coverage exposes you to penalties and uninsured claims.

Seattle's Weather Demands Specialized Coverage

Seattle's annual precipitation averages 35.4 inches and is projected to rise to 38.0 inches, combined with wind events that tear through partially installed materials and topple temporary structures. Builder's risk insurance covers the structure under construction and materials against fire, vandalism, weather, and theft, but standard property policies exclude weather-related damage during construction phases. Water damage endorsements are essential in Seattle-verify coverage specifically protects rain-exposed phases before signing any policy. Tools and equipment under roughly $10,000 and five years old need dedicated coverage that protects against theft, fire, and vandalism on-site and in temporary storage. Builders risk premiums typically range from 1 to 4 percent of project value, with water damage and earthquake endorsements adding 10 to 20 percent to base premiums (so map your project timeline to weather vulnerability and document material arrival dates to get accurate pricing).

These foundational coverages address your core exposures, but significant gaps often emerge when contractors fail to account for the specific ways their operations interact with local conditions and regulatory requirements. The next section examines where most Seattle contractors fall short and what those oversights cost them.

Where Seattle Contractors Lose Coverage Without Realizing It

Subcontractor and Hired Worker Exposure

Most Seattle contractors assume their general liability policy covers everything that happens on a job site, then discover mid-project that subcontractors and hired workers create exposures their policy explicitly excludes. When you hire a subcontractor, your general liability does not automatically extend to them-they need their own coverage, and you must verify it exists before they start work. Washington State requires you to confirm that any subcontractor carries current workers' compensation coverage, and L&I holds you responsible if they do not. A single injury to a subcontractor's employee without proper coverage transforms into a direct liability claim against you, potentially exceeding $500,000 once legal fees and lost-wage claims accumulate. If you use hired or non-owned vehicles for work-whether rented equipment trucks or borrowed company cars-your standard commercial auto policy likely excludes coverage. You need a hired and non-owned auto policy to fill that gap, yet most contractors discover this only after an accident occurs.

Tools, Equipment, and Theft Vulnerabilities

The same blind spot applies to tools and equipment theft, which Seattle contractors face year-round in urban job sites. A standard general liability policy does not cover stolen tools, damaged equipment, or materials lost to vandalism; you need dedicated tools and equipment coverage for items under roughly $10,000 and five years old. Contractors who rely on minimum coverage limits also underestimate how fast a single weather event or on-site injury exhausts their protection. Urban Seattle sites face higher theft and vandalism risk than suburban locations, making tools and equipment coverage a practical necessity rather than an optional add-on.

Weather-Related Coverage Gaps

Seattle's weather creates a second layer of vulnerability that most contractors misjudge. Water intrusion during roofing or insulation phases can cost $100,000 or more in remediation, yet builder's risk policies vary significantly in how they cover rain-exposed work-some exclude gradual water damage entirely. You must request a specific water damage endorsement and confirm it covers the exact construction phases where rain poses the greatest risk; do not assume standard builder's risk includes it. Wind events frequently topple temporary structures and tear through partially installed materials, creating weeks of project delays and thousands in remediation costs that push beyond what standard property coverage allows.

Earthquake and Specialized Endorsements

Earthquake coverage in Washington requires a separate endorsement and does not come automatically with builder's risk; for projects in or near Seattle, this gap matters more than many contractors acknowledge. Soft-cost protection (also called business interruption or income protection) helps cover lost rent, occupancy dates, or sales timelines when delays occur-this coverage becomes critical when weather events or accidents extend project timelines beyond original schedules. A comprehensive approach means documenting your project timeline, material staging plan, and weather-vulnerable phases before requesting quotes-this specificity helps underwriters price accurately and prevents post-loss disputes over what was actually covered when damage occurs.

These gaps in coverage leave contractors exposed to losses that can exceed six figures. The next section examines how to select an insurance provider who understands these local risks and can build a protection strategy tailored to your specific operations.

Finding an Insurer Who Understands Your Real Operations

Selecting an insurance provider for Seattle contracting work means moving past generic quotes and finding someone who grasps the specific exposures you face on urban job sites, in rain-heavy seasons, and under Washington's regulatory framework. Most contractors shop for price alone, then spend months fighting with claims adjusters over coverage gaps they never anticipated. The insurers who handle Seattle construction well know the difference between a $500,000 project in Georgetown and one in Ballard, understand how water damage claims play out during the rainy season, and can price builder's risk coverage for Seattle's rainy season accurately when your timeline exposes materials to weather for eight weeks instead of four.

Ask Insurers About Local Experience

Start by asking potential insurers directly: have they worked with contractors in your specific trade, and can they name three recent projects they've insured in Seattle? If they hesitate or give generic answers, move to the next provider. Carriers like Tokio Marine HCC, Zurich, Travelers, and Hiscox have established Pacific Northwest construction practices, but experience varies widely within each carrier. The individual underwriter matters as much as the company name. Request quotes from at least three providers and ask each one to itemize coverage limits, deductibles, and exclusions side by side-this forces comparison on substance rather than price alone.

When reviewing quotes, look for carriers that specifically address Seattle weather exposure in their builder's risk offerings and include water damage endorsement options without requiring a separate negotiation. Carriers experienced with Pacific Northwest construction tailor coverage to local risk profiles and avoid the generic approach that leaves contractors exposed.

Evaluate Your Agent Relationship

Your agent relationship determines whether you receive reactive claims handling or proactive guidance that prevents problems before they occur. An agent who truly understands contractor operations will ask about your subcontractor vetting process, your equipment staging practices, and whether you use hired vehicles-not because they're checking a box, but because their answers shape your actual coverage. Request that your agent provide a detailed coverage summary that translates policy language into plain English, showing exactly what's covered, what's excluded, and where gaps exist.

Demand that your agent review your coverage annually as your business evolves: new equipment, additional crews, different project types, or geographic expansion all shift your risk profile and may require coverage adjustments. When you request a certificate of insurance for a client or lender, your agent should deliver it the same day or within hours-this responsiveness signals whether they prioritize your projects or treat you as a transaction.

Verify Compliance Knowledge

A strong agent knows L&I requirements cold, can explain why your bond and insurance documents must match your exact registered business name, and catches compliance mistakes before they delay project approvals or create reinstatement fees. This expertise prevents costly delays and protects your registration status. An agent who explores offerings from top insurance providers presents you with choices that fit your requirements at the best available pricing, rather than steering you toward a single option.

Final Thoughts

Seattle contractor business insurance works best when it reflects your actual operations, not just regulatory minimums. Throughout this guide, we've examined why general liability alone falls short, how workers' compensation gaps expose you to employer liability claims, and where weather-specific coverage prevents costly project delays. The contractors who move forward with confidence address these exposures head-on rather than discovering gaps mid-claim.

Building comprehensive coverage means verifying that your general liability, workers' compensation, and builder's risk policies align with your specific trade and local conditions, confirming that subcontractor coverage and equipment insurance close the gaps standard policies leave open, and establishing an annual review process with your agent to adjust limits as your business evolves. The cost of comprehensive Seattle contractor business insurance remains far lower than the cost of a single uninsured loss-a six-figure liability claim or weather damage that halts a project for weeks can damage your reputation and cash flow in ways that price shopping cannot offset. Clients and lenders increasingly expect contractors to carry robust coverage, and demonstrating that protection strengthens your competitive position.

If you're ready to assess whether your current coverage addresses the exposures outlined in this guide, contact FirstMark Insurance Group to schedule a no-obligation coverage review. We explore offerings from top insurance providers to present you with choices that fit your requirements at the best available pricing. Moving forward with the right protection means you can focus on what you do best: building projects that matter in Seattle.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation