Construction projects in Washington face real financial exposure. Materials, equipment, and labor represent significant investments that standard homeowners policies simply don't protect.

At FirstMark Insurance Group, we work with builders who understand that residential builders risk in WA requires specialized coverage. The right policy shields your project from costly gaps that could derail timelines and budgets.

What Builders Risk Insurance Actually Covers

The Physical Assets Your Policy Protects

Builders risk insurance protects the physical assets on your residential construction project from the moment materials arrive until the project reaches completion. Unlike standard homeowners policies that activate only after a home is finished and occupied, builders risk coverage applies during the active construction phase when your property faces its highest exposure. The policy covers the structure itself, all materials and equipment on-site, temporary structures like scaffolding and protective fencing, and materials in transit to your project.

Why Fire, Theft, and Weather Matter in Washington

Fire damage to framing and materials represents one of the most significant exposures during construction-a peril that general liability policies explicitly exclude. Theft and vandalism claims occur frequently during residential projects in Washington, particularly for high-value materials like copper wiring and architectural elements left unattended overnight. Western Washington's windstorms create additional risk for partially enclosed structures where temporary roofing and unsecured materials face significant damage exposure, with structural damage from falling trees representing the costliest consequence.

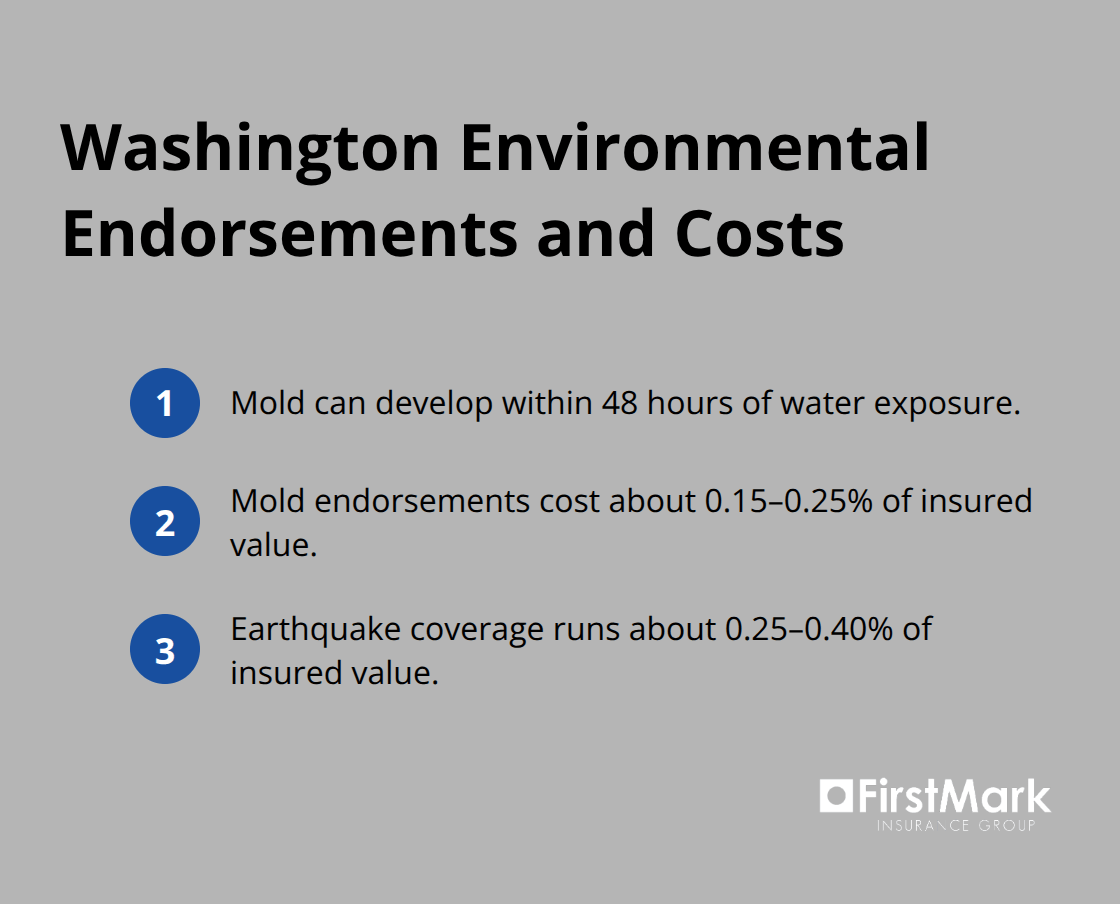

Heavy rainfall in the region heightens water damage and mold risk within 48 hours of exposure, making mold endorsements worth approximately 0.15 to 0.25 percent of your insured value. Earthquake coverage proves particularly relevant in Washington's seismic zones, typically running 0.25 to 0.40 percent of insured value and should be included if your project sits in a high-risk area.

Why Standard Homeowners Policies Leave You Exposed

Standard homeowners policies fundamentally fail residential construction projects because they're designed for occupied homes with permanent occupants, not active construction sites with exposed materials and ongoing work. These policies exclude loss or damage occurring during construction, renovation, or remodeling phases entirely. A homeowners policy will not cover theft of materials stacked on your property, fire damage to framing before the roof is installed, or labor costs associated with rebuilding after a loss.

The policy also won't cover debris removal after a loss, which can run into tens of thousands of dollars on residential projects. If your project experiences a significant delay due to weather or supply chain disruptions, your homeowners policy provides no protection for extended carrying costs or permit fees-expenses that accumulate quickly in markets like Seattle where permit processing costs reached approximately 46,000 dollars in 2023.

Construction-Specific Coverage Fills the Critical Gaps

Construction-specific coverage fills these gaps with broad protection that covers most perils unless explicitly excluded, and the policy period aligns precisely with your project timeline rather than your home's occupancy status. This alignment means your coverage activates when you need it most and terminates when the risk actually ends, not when you move into the finished home. Understanding which optional coverages make financial sense based on location, construction type, and project timeline requires careful analysis of your specific situation-something that varies significantly from one Washington project to another.

What Your Residential Project Actually Needs to Protect

The Three Protection Categories Your Project Requires

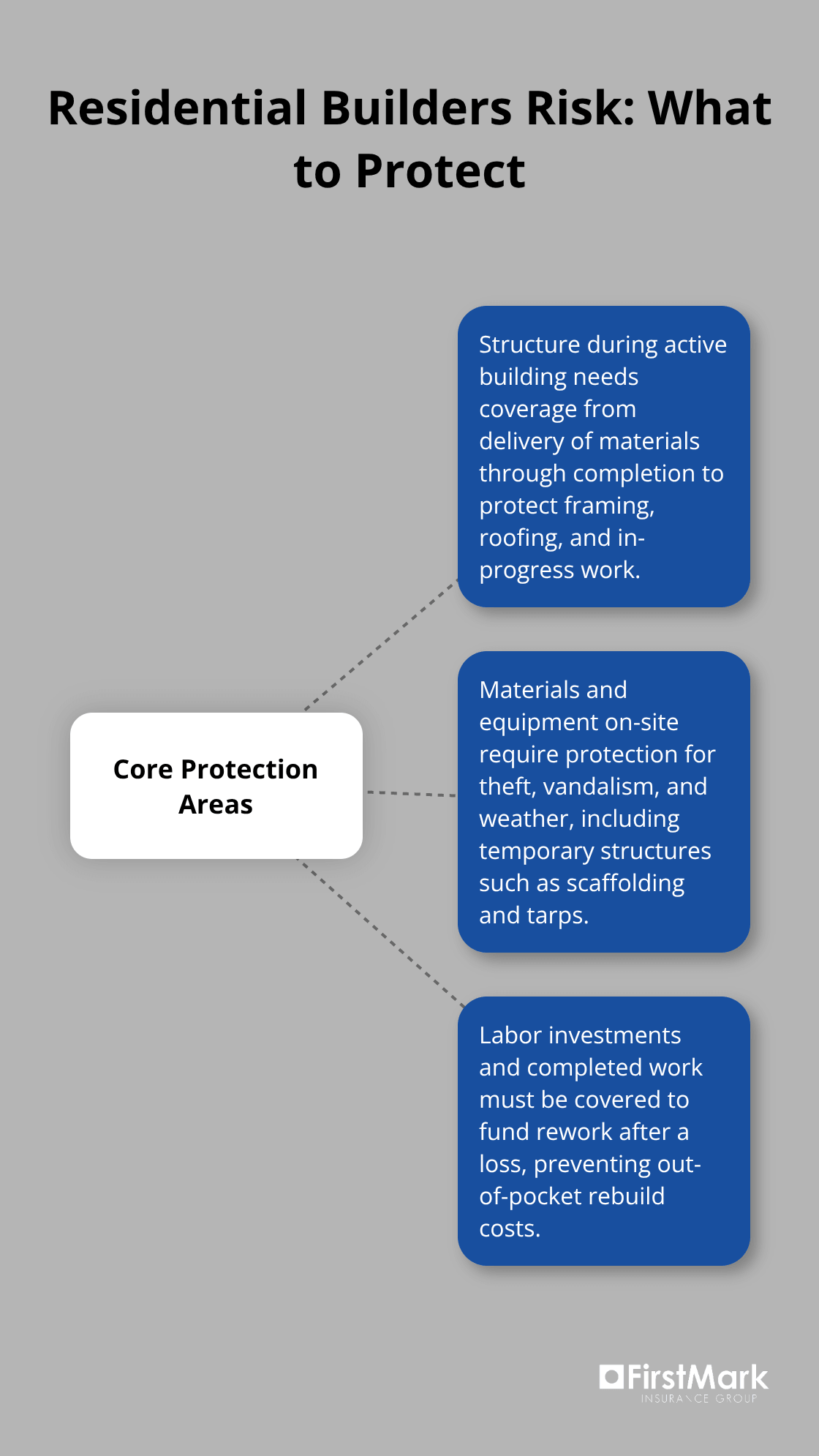

Residential construction in Washington demands coverage that addresses three distinct protection categories: the structure itself during active building, all materials and equipment present on-site, and the labor investments tied to completing the work. Each category carries separate financial exposure that standard policies fail to address. Your builders risk policy must protect against losses that occur across all three areas simultaneously, since a single fire or weather event can damage materials, equipment, and completed work at once.

Materials and Equipment Face Multiple Threats

On-site materials represent the most visible exposure, but the real financial risk extends far beyond what sits in plain view. Materials in transit to your project face theft and weather damage during delivery, particularly when suppliers store them temporarily before arrival at your property. High-value items like copper wiring, architectural metals, and specialty finishes attract theft during overnight hours when job sites sit unattended.

Installing robust security measures such as night cameras, secure fencing, and daily tool-check procedures can yield premium credits between 5 and 15 percent, making the investment in security directly reduce your insurance costs. Equipment on-site includes not just the materials becoming part of the finished home, but also temporary structures like scaffolding, protective fencing, and tarping systems that shield the active work area from weather exposure. These temporary installations cost money to install and remove, yet they face significant damage risk from Western Washington's 60 mph windstorms and heavy rainfall events.

Labor Costs and Soft Costs Demand Separate Protection

Labor and completed work protection operates differently than material coverage because it addresses the financial impact when construction work requires completion following a loss. If fire damages framing before the roof installation, your builders risk policy covers the replacement materials, but it also protects the labor cost to rebuild that framing, which often exceeds material expense alone.

Soft costs represent another critical protection gap that many residential builders overlook entirely. These costs include permit fees, inspection charges, extended loan interest if project delays occur, and architect or engineer fees required to obtain revised approvals after a loss. Seattle's permit processing costs reached approximately $46,000 in 2023, demonstrating why soft-cost coverage matters on residential projects in Washington's major markets.

Liability Coverage Protects Against Third-Party Claims

Liability coverage during construction addresses third-party injury claims that fall outside your homeowners policy's active construction exclusion. A worker or visitor injured on your construction site could file a claim against your general liability coverage, but builders risk policies often include additional liability protections tailored to construction activities. These protections extend beyond what standard homeowners policies provide during the active construction phase.

Understanding which coverages your specific project requires means analyzing your location's environmental risks, construction timeline, and material values with precision. Standard coverage limits often underprotect your actual exposure, leaving gaps that surface only when you file a claim. The next section examines the common gaps that residential builders encounter and shows you how to identify them before construction begins.

Common Gaps That Derail Residential Projects in Washington

Underinsurance Penalties That Cost Thousands

The most destructive gap in residential builders risk coverage stems not from missing perils but from insuring at the wrong value. Most residential builders in Washington underestimate their project's replacement cost, then discover mid-claim that their policy includes a 100 percent coinsurance requirement. This requirement means any underinsurance triggers a proportional penalty on the entire claim. If you insure a $500,000 project at $450,000 and suffer a $100,000 loss, the insurer calculates your recovery as $100,000 multiplied by the ratio of insurance carried to insurance required, reducing your payment to $90,000. That $10,000 penalty disappears from your pocket.

The correct approach requires establishing your project's insured value by starting with the total replacement cost of materials, labor, and temporary structures, then subtracting only the land value. Many builders mistakenly use the sales price minus land as their baseline, which works only if labor and material costs align perfectly with market pricing. On renovation projects, this calculation becomes even more critical because you must insure the replacement cost of both the new work and any existing structure damage that a loss might expose.

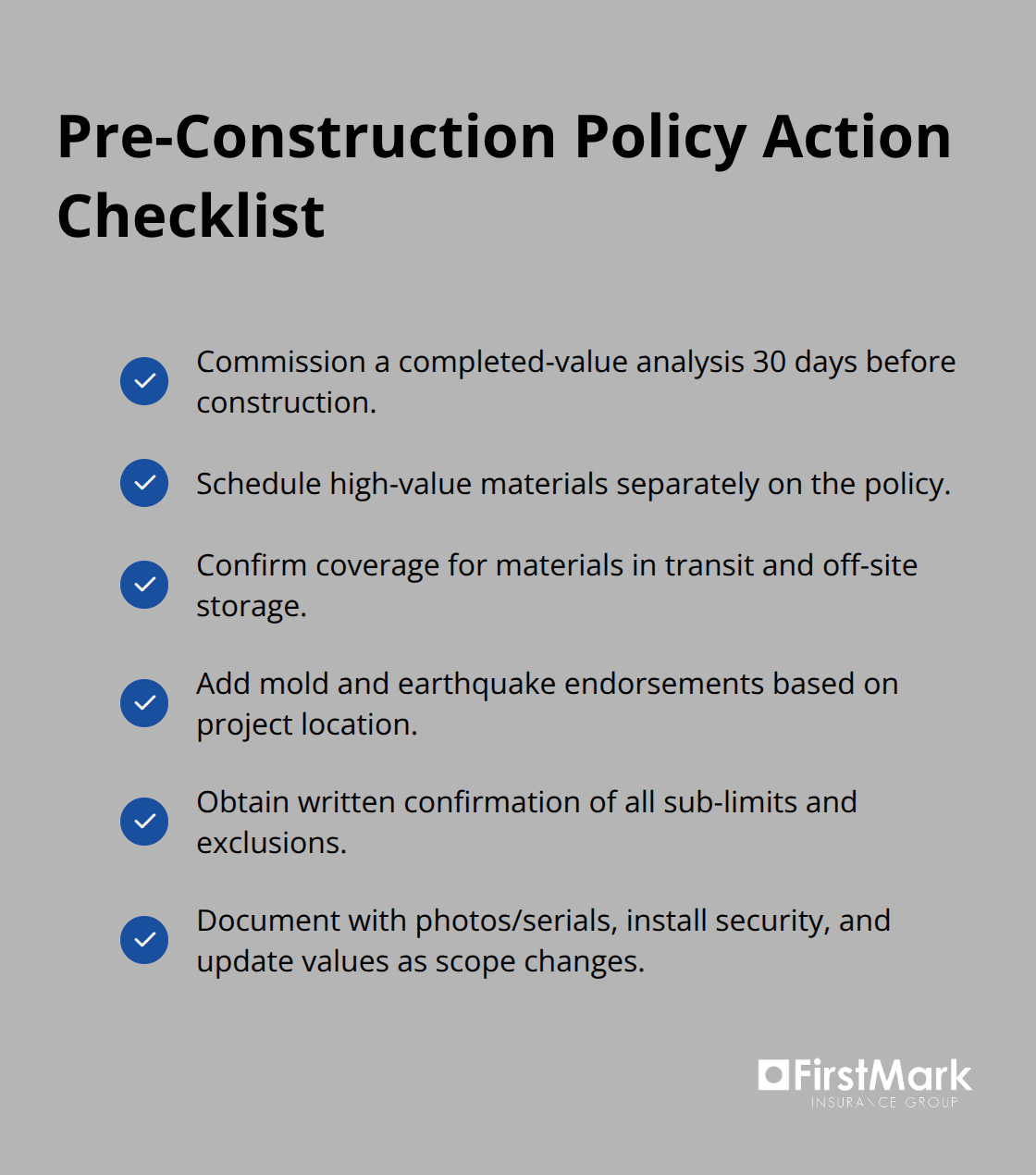

Before groundbreaking, commission a detailed completed-value analysis from your agent, particularly for projects exceeding $5 million where underinsurance penalties compound into six-figure losses. Update your insured value whenever project scope changes materially, and request written confirmation from your carrier showing the exact replacement cost basis they've accepted.

High-Value Materials and Theft Exposure

Copper wiring, architectural metals, and specialty finishes attract organized theft during overnight hours, yet many policies carry sub-limits of $5,000 or $10,000 on theft claims when these materials alone might exceed $50,000 in value. Schedule high-value components separately on your policy to avoid coinsurance penalties and obtain full replacement cost protection.

Installing robust security measures such as night cameras, secure fencing, and daily tool-check procedures can yield premium credits between 5 and 15 percent, making the investment in security directly reduce your insurance costs. Thorough on-site documentation (photos, serial numbers, security measures) and a daily storage log speed claims and reduce disputes about what was on-site.

Materials in Transit and Off-Site Storage

Materials in transit and off-site storage locations represent another persistent blind spot, particularly when suppliers hold materials at their facilities before delivery or when your project requires temporary material staging at a secondary location. Your builders risk policy must explicitly cover materials heading toward your project and materials stored away from the job site, with written confirmation of coverage limits at each location.

Temporary structures including scaffolding, protective fencing, tarping systems, and weather protection equipment face substantial damage risk from Western Washington's 60 mph windstorms and heavy rainfall, yet these installations often receive minimal or no coverage under standard policies. Request specific coverage limits for temporary structures and confirm whether wind and weather damage to scaffolding and tarping receives full replacement cost protection.

Environmental Risks Specific to Washington

Mold endorsements prove essential in Western Washington's wet climate, where water exposure within 48 hours can trigger mold growth that standard policies exclude entirely. These endorsements cost approximately 0.15 to 0.25 percent of your insured value but prevent claims that could reach $50,000 or higher. Earthquake coverage proves particularly relevant in Washington's seismic zones, typically running 0.25 to 0.40 percent of insured value and should be included if your project sits in a high-risk area.

Documentation and Policy Review Before Groundbreaking

Schedule a comprehensive policy review with your agent at least 30 days before groundbreaking, requesting a written summary that lists every endorsement, specifies sub-limits for high-value categories, identifies any excluded equipment or materials, and clarifies whether inland marine coverage applies to tools or specialized equipment. This documentation creates a reference point for claims and prevents disputes about what your policy actually protects.

Final Thoughts

Residential builders risk in WA protects your project's most valuable assets during the phase when exposure runs highest. The coverage addresses gaps that standard homeowners policies leave wide open, from fire damage to framing and theft of materials to labor costs following a loss. Your project's success depends on understanding what your policy actually covers and identifying gaps before groundbreaking.

Underinsurance costs more than adequate coverage, so commission a completed-value analysis 30 days before construction begins to prevent penalties that surface only when you file a claim. Schedule high-value materials separately, confirm coverage for materials in transit and off-site storage, add environmental endorsements like mold and earthquake protection based on your Washington location's specific risks, and request written confirmation of every sub-limit and exclusion from your carrier. Document everything on-site with photos and serial numbers, install security measures that yield premium credits, and update your insured value whenever project scope changes materially.

Contact FirstMark Insurance Group to schedule a policy review with an agent who understands residential construction in Washington. Bring your project timeline, location, and preliminary budget, and we'll help you build protection that matches your actual exposure rather than leaving gaps that could derail your investment.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation