General liability insurance in Washington protects your business from costly claims that can threaten your financial stability. Many business owners underestimate their coverage needs or overlook critical gaps that leave them exposed.

At FirstMark Insurance Group, we’ve seen firsthand how the right coverage limits make the difference between a manageable claim and a business-threatening liability. This guide walks you through what you need to know to protect your operation effectively.

What General Liability Insurance Actually Covers

The Three Core Coverage Categories

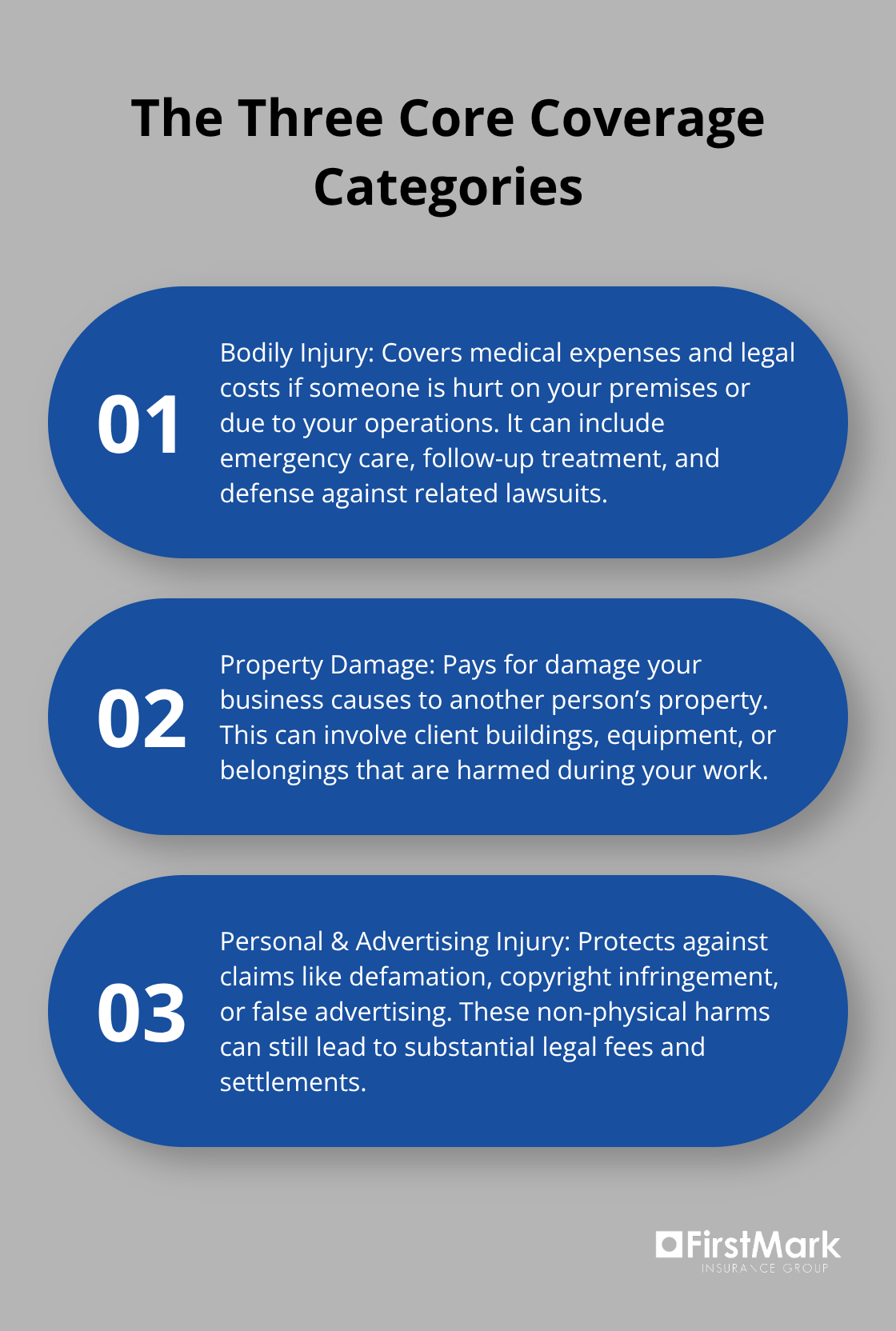

General liability insurance in Washington protects your business against three distinct categories of claims that can drain your operating budget fast. Bodily injury claims cover medical expenses when someone gets hurt on your property or because of your business operations. If a customer slips on a wet floor in your retail space and needs emergency care, your policy pays those medical bills plus any resulting lawsuit costs.

Property damage liability covers harm your business causes to someone else’s property, whether that’s damage to a client’s building during a renovation project or harm to their equipment while you work on-site. Personal and advertising injury claims protect you from accusations like defamation, copyright infringement, or false advertising-claims that don’t involve physical injury but can still generate expensive legal fees.

Why Coverage Limits Matter More Than Coverage Types

The coverage limits you choose matter far more than the coverage types themselves. A $1 million per-occurrence limit sounds adequate until you face a scenario where multiple people suffer injuries in a single incident. If three customers sustain injuries in one event and each claim reaches $400,000, you exhaust most of your coverage with potentially more liability remaining. Washington’s at-fault insurance system means you remain personally responsible for damages that exceed your policy limits, which can trigger lawsuits against your personal assets.

Understanding Per-Occurrence and Aggregate Limits

Your policy includes a separate aggregate limit that caps total payouts during your entire policy year, typically ranging from $2 million to $5 million depending on your business profile. Defense costs-the attorney fees and court expenses your insurer pays to defend you-typically come out of your limits, not in addition to them. A lengthy legal battle can consume your coverage even if the claim ultimately gets dismissed. Industry standards suggest businesses with significant customer interaction or property exposure should carry minimum per-occurrence limits of $1 million to $2 million, though your specific needs depend entirely on your operation’s actual risks.

Your business size, industry classification, and exposure profile determine whether these standard benchmarks apply to you or whether you need substantially higher protection. The next section walks you through how to analyze your particular situation and select limits that actually match your exposure rather than simply following industry averages.

Choosing Limits That Match Your Actual Exposure

Map Your Operational Risks First

Your business size alone tells you almost nothing about the coverage limits you need. A small consulting firm operating from a home office faces fundamentally different liability exposures than a small restaurant serving hundreds of customers daily. The restaurant confronts slip-and-fall risks, food-safety exposure, and constant customer interaction that demand substantially higher limits. Your industry classification drives your baseline exposure profile far more than your employee count or annual revenue. Construction contractors face environmental contamination risks that retail shops don’t encounter. Medical practices confront professional liability exposure that manufacturers don’t. You must map your actual operational risks rather than defaulting to industry averages that may not fit your specific business model.

Identify Your Worst-Case Scenario

Washington state doesn’t mandate minimum general liability coverage limits for most businesses, which means you carry the responsibility to determine adequate protection yourself. This freedom creates a dangerous trap where many owners simply match whatever their competitor carries or whatever their insurance agent suggests without analyzing their genuine exposure. Start by identifying your worst-case scenario. If you operate a fitness facility, what happens if someone suffers a serious spinal injury during a class and requires lifetime care? If you run a construction company, what’s the potential cost of property damage to a client’s structure if your crew causes structural failure? Your per-occurrence limit should cover your realistic worst-case scenario plus the legal defense costs that accompany it.

Set Per-Occurrence and Aggregate Limits Appropriately

Most Washington businesses with customer interaction or significant property exposure should carry minimum per-occurrence limits of $1 million, though many underestimate and select $500,000 limits that prove inadequate when actual claims materialize. Your aggregate limit should typically reach at least double your per-occurrence limit to account for multiple incidents within a single policy year. A business facing high-frequency, lower-severity claims benefits from a higher aggregate relative to per-occurrence limits, while operations with lower-frequency but potentially catastrophic exposure need adequate per-occurrence protection even if the aggregate is proportionally lower.

Balance Premium Costs Against Coverage Gaps

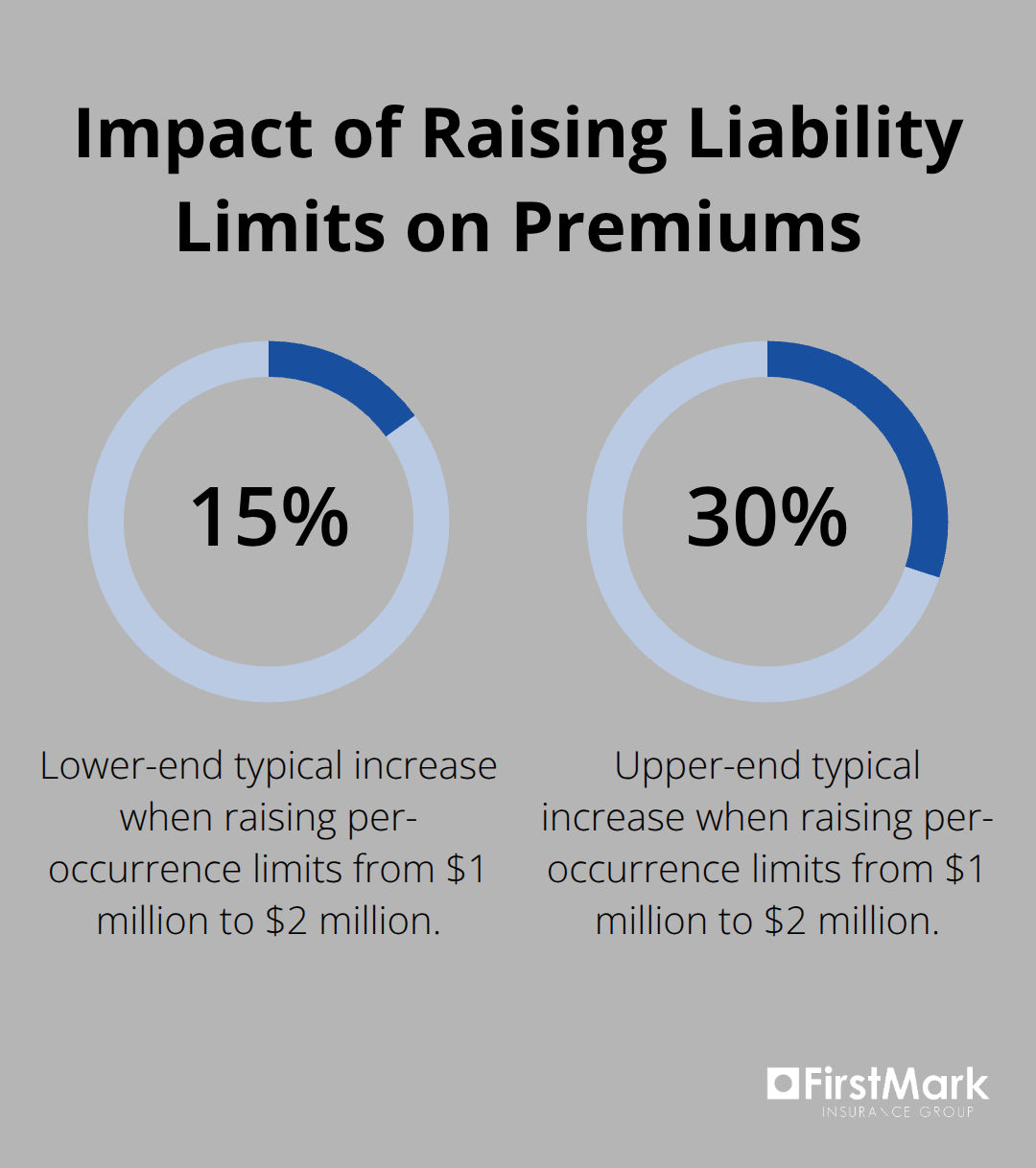

Premium costs matter, but they matter far less than the gap between your coverage and your actual liability. Increasing your per-occurrence limit from $1 million to $2 million typically raises your annual premium by 15 to 30 percent depending on your industry and claims history, yet that additional $1 million in protection could prevent a lawsuit from destroying your business.

Umbrella or excess liability policies extend your coverage beyond your base limits at remarkably low cost, often adding $1 million to $5 million in additional protection for $300 to $800 annually.

Review Coverage as Your Business Evolves

If your business has grown or your operations have expanded, your coverage limits likely haven’t kept pace with your actual exposure. Your policy should reflect your current operations, not the business you ran three years ago. A licensed Washington insurance professional who understands your specific operations can help you evaluate whether your current limits still match your exposure. This assessment becomes especially important when you add new service lines, expand into new locations, or increase your customer base significantly. The next section examines the coverage gaps that standard general liability policies leave unprotected and how to identify which additional policies your business actually needs.

Common Gaps in General Liability Coverage

Standard general liability policies in Washington contain specific exclusions that leave your business exposed to real and expensive risks. Flood damage sits entirely outside coverage, which matters significantly if your business operates in a flood-prone area or near water. Environmental contamination from your operations typically gets excluded unless you purchase specific pollution liability coverage.

Professional services like accounting, legal advice, or consulting fall outside general liability protection and require separate professional liability policies. Contractual liability-situations where you’ve assumed someone else’s liability through a written agreement-often gets excluded or severely limited under standard policies. If you’ve signed a contract requiring you to indemnify a property owner or client for their negligence, your general liability policy may refuse to defend you.

Construction and Contractual Exposure

Construction contractors frequently discover this gap when a client’s contract requires them to cover the client’s liability, creating exposure that standard coverage won’t touch. Product liability for products you manufacture or distribute gets excluded from most general liability policies, requiring separate product liability coverage if you sell physical goods. Abuse or molestation claims face strict exclusions in most policies, creating dangerous gaps for businesses serving vulnerable populations like children or elderly clients. These aren’t minor technical exclusions-they represent the difference between having coverage and facing claims entirely out of pocket. Many Washington business owners operate for years without realizing their primary policy leaves their biggest exposures unprotected.

Professional Liability and Specialized Coverage

Professional liability insurance covers claims of negligence, errors, or omissions in your professional services, protecting you when a client alleges you provided faulty advice or substandard work. This coverage becomes non-negotiable for consultants, accountants, architects, and similar service providers. Pollution liability coverage protects against environmental contamination claims, essential for contractors, manufacturers, and any business handling chemicals or hazardous materials. Commercial auto insurance must supplement general liability if you use vehicles for business purposes, since personal auto policies explicitly exclude business use and standard general liability won’t cover vehicle-related incidents.

Vulnerable Populations and Product Risks

Abuse and molestation coverage specifically addresses claims of abuse or molestation, protecting organizations serving children, elderly individuals, or vulnerable populations. Products liability insurance covers injuries or property damage caused by products you manufacture, distribute, or sell. Contractual liability endorsements or separate coverage address risks you’ve assumed through written agreements, particularly important in construction and service industries where contracts regularly require indemnification.

Cost-Effective Protection Strategies

Rather than purchasing each coverage separately at premium rates, many Washington businesses benefit from a business owners policy that bundles general liability with property coverage, business interruption, and other essentials at better pricing than standalone policies. Umbrella coverage extending $1 million to $5 million beyond your base limits costs remarkably little-typically $300 to $1,000 annually depending on your underlying coverage and industry-making it the most cost-effective way to address the gap between your standard limits and your actual exposure. The specific gaps your business faces depend entirely on your operations, which means a professional assessment of your actual exposures matters far more than generic coverage recommendations.

Final Thoughts

General liability insurance in Washington protects your business from claims that can devastate your finances, but only if your coverage limits actually match your exposure. Map the specific risks your business creates through its daily operations, then review your current policy limits against your realistic worst-case scenario. If you can’t articulate why your per-occurrence limit is adequate for your biggest potential claim, your limit is probably too low.

Consider whether umbrella coverage makes financial sense for your operation, since adding $1 million to $5 million in additional protection often costs less than $1,000 annually. Your coverage needs change as your business evolves-new service lines, expanded locations, or increased customer volume all shift your liability profile. Annual policy reviews ensure your coverage keeps pace with your business growth rather than protecting the operation you ran years ago.

We at FirstMark Insurance Group work with Washington business owners to understand their specific exposures, evaluate their current coverage against their actual risks, and recommend limits that provide genuine protection without unnecessary expense. Contact our team to discuss how your general liability insurance Washington policy aligns with your business’s reality.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation